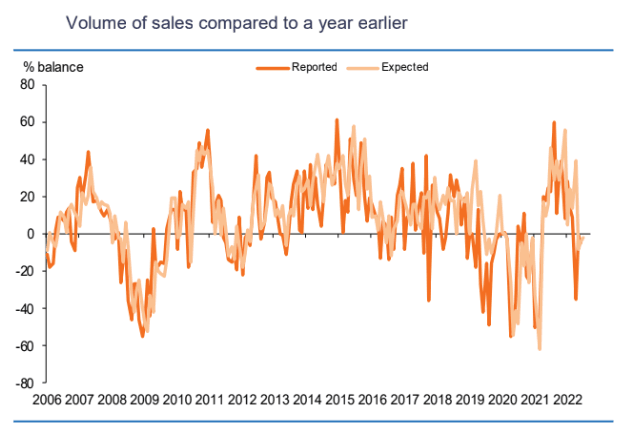

UK DATA: CBI Retail Outlooks Weak as Demand Wanes

UK CBI JUNE REPORTED SALES BALANCE -5.0% VS MAY -1.0%

UK CBI JULY EXPECTED SALES BALANCE -2.0%

- The CBI distributive trades report saw a small dip in sales reported in June, implying no growth in sales volumes in Q2. Retail was again below levels seen in June 2021.

- Inventory levels remained high, as firms struggled to push through stock. As consumer demand wanes on the back of soaring inflation, expected sales are anticipated to remain flat. The downturn in consumer spending generated upstream effects, with wholesale sales stagnating as retailers factor weak growth outlooks into sale volumes in upcoming months.

- The motor industry saw "good" sales volumes in June, however, this is expected to soften again next month.

- The latest CBI report precedes the official May retail sales data, due June 24 , which is anticipated to see a further 4.5% y/y contraction.

Source: CBI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

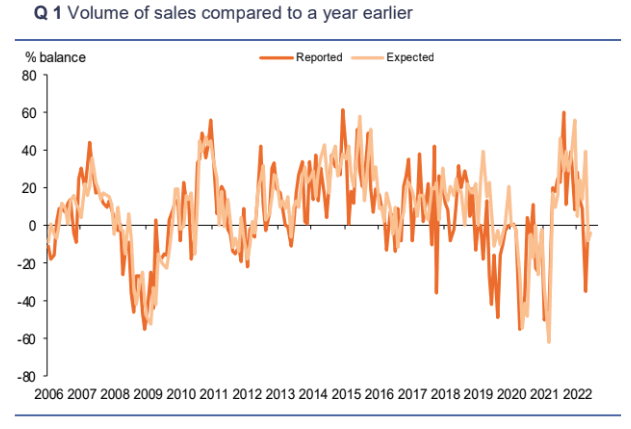

UK DATA: CBI Sees May Retail Sales Recover from April Lows

UK MAY REPORTED SALES VOLUME BAL -1 (FCST -30) VS -35 APR: CBI

JUN EXPECTED SALES VOLUME BALANCE -4 VS -8 MAY: CBI

MAY REPORTED ORDERS VOLUME BALANCE +2 VS -7 APR: CBI

JUN EXPECTED ORDERS VOLUME BALANCE -3 VS -9 MAY: CBI

- May reported retail sales came in substantially stronger than the forecast, recovering the bulk of April losses. We note that this data is relatively volatile and draws most of its value from being a directional indicator.

- Sales were average for May, following the April falls. Outlooks for the upcoming months remain subdued.

- Inventories continue to remain high and rising as demand slows, whilst internet sales fell at the fastest rate on record (since 2009).

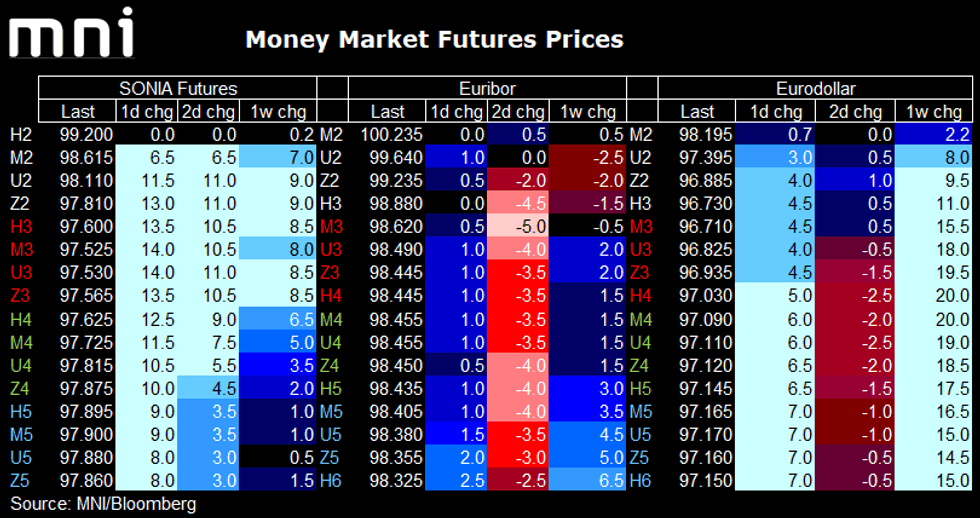

STIR FUTURES: Different drivers across major STIR markets this morning

SONIA futures continue to lead the way higher for STIR futures after the disappointing UK PMI prints; the Eurodollar strip was dragged higher earlier following risk-off initially triggered by Snapchat earnings and concern about the Chinese growth outlook. Villeroy's comments about the ECB moving back to a neutral rate of 1-2% next year have contained moves higher for the Euribor strip.

- SONIA Whites/Reds/Greens are up 10-14 ticks (with the biggest moves in the June-23 and Sep-23 area). The market-implied probability of a 50bp hike by August reduced from around 65% at yesterday's close to 30% earlier and is now back to around 40%. June is now priced for 29bp (from 31bp yesterday close), August 60bp (from 66bp), September: 83bp (from 91bp) with 118bp by year-end (from 129bp).

- The majority of the Euribor strip is up 0.5-1.0 ticks. Markets now price 32bp by July (cumulatively), 65bp by September, 83bp by October and 104bp by year-end.

- The Eurodollar strip has flattened with Whites up 3.0-4.5 ticks and Blues up 7.0 ticks (with Reds/Greens between these). Markets now price 52bp for June, 101bp for July, 138bp by September and 191bp by year-end.

EURIBOR OPTIONS: Euribor call fly

0RZ2 98/75/99.00/99.25c fly, bought for 2.35 synthetic in 5k