EM ASIA CREDIT: MNI EM Credit Overnight – CEEMEA & LATAM

Emerging Markets spreads had a weaker bias overnight, with CEEMEA benchmark bonds weaker and a range bound tone overall in LATAM.

In CEEMEA, benchmark sovereign spreads were up to 10bp wider, while corporate bonds were up to 5bp wider. We saw a busy primary market session, with seven new deals and mandates. In newsflow, Qatar National Bank reported Q3 earnings, which were a neutral read; we also received updates on Ivanhoe Mines' production and dewatering process. Additionally, the US Supreme Court rejected Halkbank’s argument of sovereign immunity.

In LATAM, benchmark spreads traded in a narrow range (+/– 1bp), although USD bonds of troubled Telefónica Móviles Chile moved a point higher as América Móvil and Entel issued a statement confirming reports from last week that they had signed a non-binding agreement to consider acquiring part or all of the Chilean telecom firm. Finally, the Codelco-SQM lithium deal received approval from China.

Ivanhoe Mines: Prod'n and Dewatering process update see link https://mni.marketnews.com/46FTSFS

Halkbank: Supreme court rejected sovereign immunity see link https://mni.marketnews.com/4h2zBxG

Codelco: China Approval for Lithium Mining JV – Neutral: https://mni.marketnews.com/4q1c83Q

CEEMEA: https://mni.marketnews.com/48q1NZf

LATAM: https://mni.marketnews.com/46QI57P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Week Ahead: The Macro, Valuation, Sentiment & Technical Lens

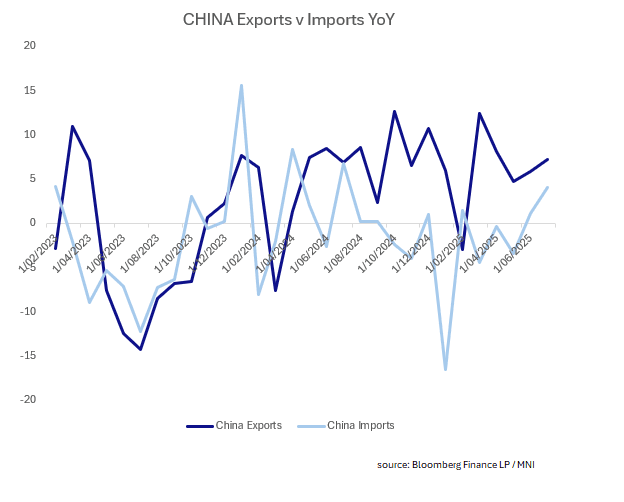

Macro: Last week's August PMIs surprised to the upside with manufacturing expanding at +50.5 (forecast 49.8) and services very strong at 53.0. This week's key releases will be the August trade data. Exports for July rose +7.2% and the forecasts for August is currently +5.5% and Imprts +3.4%.

Fig 1: China Trade Data Year on Year

Valuations: The performance of equity markets in recent weeks have seen P/Es at the top end of their full year forecasts and above the average of for the full year over the last 5-years, though lower than the post-COVID highs. Bonds remain well contained with the 10-Yr government bond trading in a 2-3bp range over the last few weeks.

Sentiment: The strength of the equity market has seen people rushing to open equity accounts. Signs of life in the Shanghai real estate market are encouraging, but will need to see a more sustained recovery in multiple key cities. Margin trade account openings have grown, though in context the size of China’s stock market also has nearly doubled in the past decade. The amount of leveraged purchases as a proportion of total market capitalization was 2.2% as of Monday last week, slightly above the 10-year average but far below 2015’s peak of 4.6% (as reported by BBG).

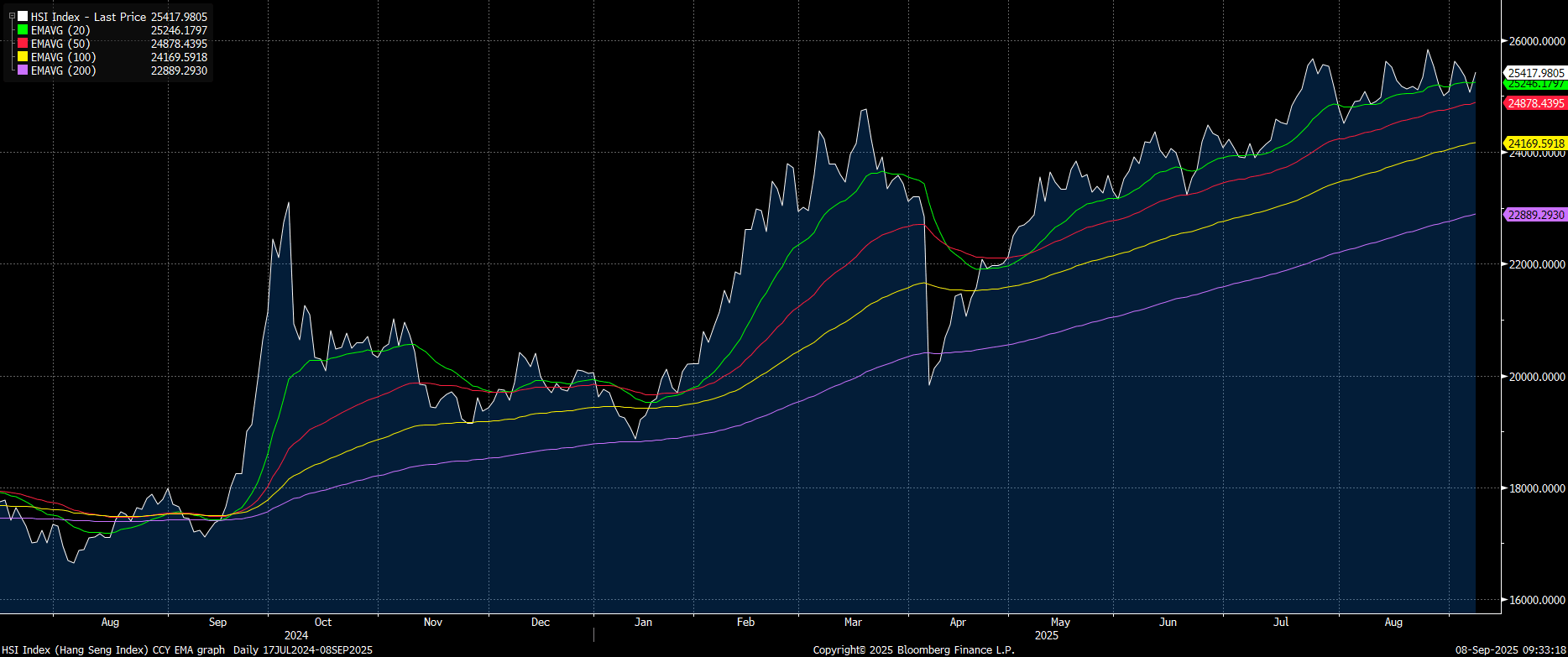

Technicals: Whilst the CSI 300 sits comfortably above the 20-day EMA, the Hang Seng has bounced above and below it in the last fortnight, closing above it last week, and is up +2.2% over the last month, compared to +8.6% for the CSI 300. Government bond issuance for the week ahead sees a barbell approach to maturities.

09/10 : China to Sell 149 Billion Yuan 2030 Bonds

09/10 : China to Sell 35 Billion Yuan 2075 Bonds

Fig 2: Hang Seng vs 20, 50, 100 and 200-day EMA

source: Bloomberg Finance LP / MNI

JAPAN DATA: Q2 GDP Growth Revised Higher, Consumption Up, Capex Down

Japan Q2 GDP revisions were stronger than expected. Headline Q2 GDP rose 0.5%q/q, against a 0.3% expectation (which was the initial print). Nominal GDP rose 1.6%q/q, against a 1.3% forecast. The y/y deflator was unchanged though at 3.0%.

- In terms of the detail, private consumption growth was revised up to 0.4%q/q from 0.2%, but capex was revised to 0.6%q/q growth (from 1.3%). The inventory contribution was flat, versus an initial -0.3pt drag. Exports contribution was unchanged at 0.3%pt.

- It's also likely that public investment improved versus initial estimates. Our policy team noted last week: "Public investment is expected to be revised to flat on quarter from the initial -0.5%."

- The revisions are welcome from a broader growth standpoint. We have now had 5 consecutive quarters of growth (albeit with Q1 only marginally positive at 0.1%q/q).

- The authorities will be hoping that this trend is sustained, with near term focus on the tariff fallout. Its impact on profitability/capex is a BOJ watchpoint, with the next Tankan survey, out at the start of Oct, to help gauge impact.

US TSYS: Cash Open

TYZ5 is trading 113-09, down 0-03+ from its close.

- The US 2-year yield opens around 3.522%, up 0.01 from its close.

- The US 10-year yield opens around 4.09%, up 0.02 from its close.

- MNI INTERVIEW: Fed To Cut Faster After Weaker Jobs - William English. "There's no doubt the labor market report was soft, and that causes them to lean in the direction of easier policy," he said in an interview Friday. "It leans in the direction of easing policy further, faster than maybe the Fed had been inclined to."

- Holger Zschaepitz on X: "The real surprise came in the revisions: BLS revealed that the US economy lost 13k jobs in June, marking the first monthly decline in employment since Dec2020. That also means the 53mth streak of continuous job growth ended in May; a major turning point for the US labor market.”

- Bob Elliott on X: “Labor market weakening needed to get the cuts so many want also means that growth is far weaker than what's currently priced in.”

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone between 4.15%-4.20%. First target the 4.00% zone then the 3.80% area.

- Data/Events: NY Fed 1-Yr Inflation Expectations, Consumer Credit