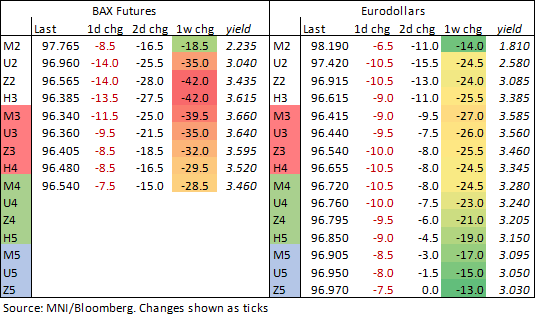

CANADA: Second Day Of Double Digit Increases In BAX Yields

Apr-21 15:05

- BAX futures yields continue to move higher, up ~14bps through most of the white pack before easing to high single digit increases by the end of the reds.

- Yesterday’s CPI continues to give it legs to rise faster than moves seen in Eurodollars, for a very large 28bp increase in BAZ2 in two days.

- It could be hard to top this increase with Powell (currently on ongoing remarks at separate event before 1300ET IMF panel) and Macklem (1900ET) speaking later, leaving potential for some pullback if they fail to match market hawkishness.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGB/Gilt - New multi year high yields

Mar-22 15:03

- EGBs and Bund continued to collapse today, with yield reaching new multi years highs.

- Volumes were also a little better, compared to the last 7 sessions, but are still overall below what you would expect for Bund.

- The main driver, besides the Hawkish Fed Powell last night which set the early downside tone, was the constant rally in Equities, which started during the European morning hours, and contracts saw some follow through as the US came in.

- The move in risk (Europe) is a little perplexing, as tension in Russia remains, also higher rates would imply the end of cheaper money.

- Seems the reflation trade has taken a back seat of late, and potentially more rebalancing out of Govies and into Equities could have been at plau.

- US Equities saw short covers, as they caught up with the European move.

- Peripheral spreads are mixed, Greece is 0.9bp wider and Spain 2.1bps tighter.

- Gilt outperform Bund, but ie 90 ticks down vs 101 ticks for the Bund at the time of typing.

- Gilt/Bund spread is in turn 1.1bp wider.

- Looking ahead, BoE Cunliffe, ECB Lane, SNB Jordan, and Fed Daly, Mester, are yet to speak.

US EURODLR OPTIONS: BLOCKS, Recent Quarterly Put Spds

Mar-22 15:02

- +15,000 Dec 97.00/97.25 put spds 7.0 over 98.50/98.75 call spds at 1040:25ET

- +2,200 Sep 98.25/98.50 6x5 put spd, 39.5 net at 1030:09

US TSYS: Market Roundup: Tsy Yields March Higher

Mar-22 14:54

Tsy futures trading weaker across the board, near recent lows after 30Y Bond yields climb to highest lvl since June '19 at 2.6026%, 2.5790% last as rates bounce slightly.

Carry-over weakness in rates after hawkish Fed chair Powell comments from Monday's NABE conf: in short willingness to make "more than 25bp" hikes at each meeting in order to keep inflation in check if needed.

- Tsy sell-off accelerated this morning after StL Fed Pres Bullard comments on Bbg TV urged Fed to "move aggressively to curb inflation .. faster is better" to get "policy back to neutral", adding 50bp hike "would definitely be in the mix."

- Slight delayed reaction to hawkish StL Fed Bullard comments, lead quarterly Eurodollar futures reversed after going bid on lower 3M LIBOR settle (-0.00386 to 0.95371%, +0.01971/wk).

- Markets less whippy than Monday opener, better volumes (TYM2>870k already), market depth w/Japan back from extended holiday weekend. Pick-up in Asia real$ selling in long end partially mitigated by leveraged$ acct buying. Tight stops triggered again in early trade, deal-tied rate-lock selling in short end, tactical curve flattener unwinds.

- Tsy yld curves steepening as bonds gradually move off lows over last hour, 5s10s still inverted at -1.659, 5s30s off 17.309 low at 19.879.

- Cross asset: Equities climbing: SPX emini +47.75 (1.07%) at 4500.5. West Texas Crude (WTI) -$2.22 (-1.98%) at $109.90; Gold -$21.59 (-1.12%) at $1914.30.

- Technicals for TYM2: Monday’s strong sell-off that confirmed a resumption of the primary downtrend. Move lower maintains bearish price sequence of lower lows and low highs, reinforcing the current bear cycle. Focus on 122-20, the 176.4% retracement of the Feb 10 - Mar 7 climb and 122-00 further out.

- Upside: firm resistance is seen at 125-23+, the 20-day EMA.