AUSSIE 10-YEAR TECHS: (Z5) Reversal Lower Extends

- RES 3: 95.960 - High Apr 7 (cont.)

- RES 2: 95.875 - High Jul 2 (cont.)

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.645 @ 16:24 BST Sep 30

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading closer to their recent lows. It is still possible that the recent move down is a correction. Near-term resistance to watch is 95.780, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.875, the Jul 2 high on the continuation chart. On the downside, key short-term support to watch has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

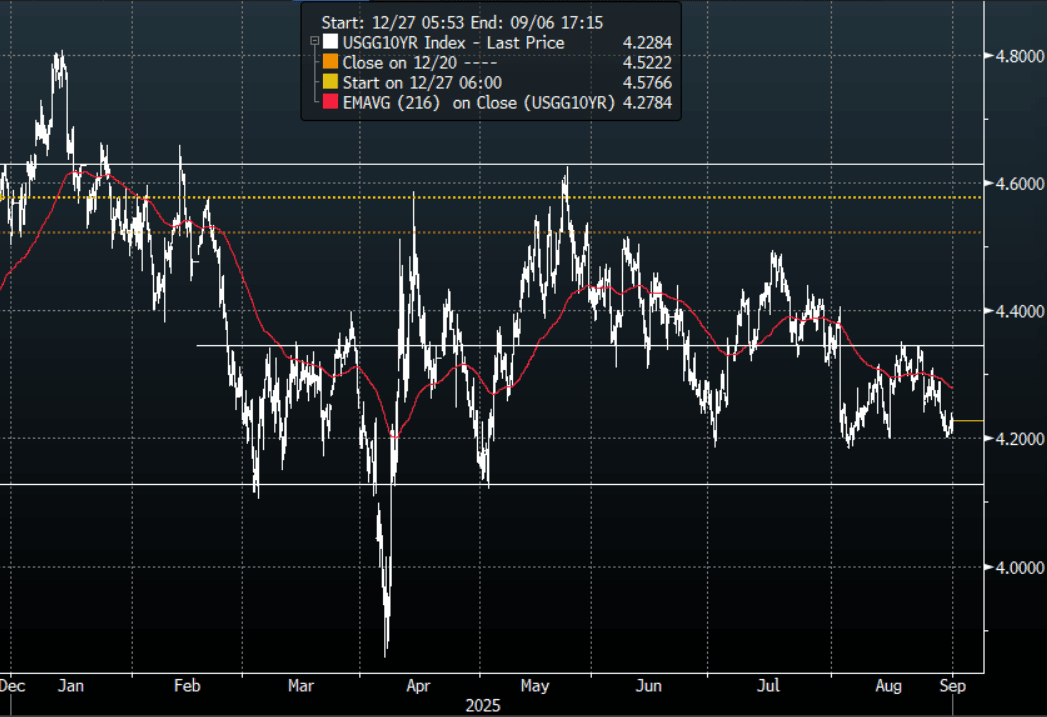

US TSYS: Long-End Yields Bounce Friday, US Holiday Today

TYU5 reopens at 112-14+, down 0-01+ from closing levels in today’s Asia-Pac session.

- Friday night the US 10-year yield had a range of 4.2052% - 4.2401%, closing around 4.23%.

- Treasury yields ended mixed Friday night; the long-end moved higher and this saw the yield curve steepen (2s10s +3.94 at 60.965, 5s30s +4.67 at 122.993).

- MNI BRIEF: Fed's Daly Says Soon Time To Recalibrate Policy. San Francisco Fed President Mary Daly said Friday the time is coming for the Federal Reserve to reduce interest rates in order to prevent further damage to a weakening job market. "It will soon be time to recalibrate policy to better match our economy," she wrote in a LinkedIn post. "Congress has given the Fed two goals: full employment and price stability. Both are in tension at the moment, with tariffs pushing inflation higher and the labor market showing signs of slowing."

- Bloomberg: Trump’s Global Tariffs Found Illegal by US Appeals Court - Most of President Donald Trump’s global tariffs were ruled illegal by a US appeals court that found he exceeded his authority in imposing them. A panel of judges in Washington on Friday upheld an earlier ruling by the Court of International Trade that Trump wrongfully invoked an emergency law to issue the tariffs.

- 10-Year Yields continue to find supply toward the 4.20% area. While the 4.35% area holds, bounces should still see demand. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Yields Steady To Start The Week, Building Permits Due

NZGB yields are little changed in the first part of Monday dealings. Aggregate moves are close to unchanged at this stage. The 2yr was last close to 2.95%, while the 10yr was near 4.34%. Both benchmarks finished lower for last week, with 2yr yields off by slightly more than the 10yr. NZ 2yr swap rates are a touch above recent lows, last around 2.73%.

- In the US on Friday, there was a Late bounce in Tsy futures on SF Fed Daly comment on LinkedIn: that "it will soon be time to recalibrate policy". Still, the 10yr yield remained above 4.20%, while front end yields finished down a touch (2yr to 3.62%).

- Late on Friday, NZ time, RBNZ Chair Quiqley announced his resignation. Finance Minister Willis stated: "Speaking to RNZ shortly after, Willis said Quigley tendered his resignation following a discussion with her earlier on Friday about the "ongoing criticism" of the board's handling of information surrounding Orr's departure on 5 March." (via BBG). PM Luxon also backed the move.

- "New Zealand Buyers Less Confident Of House Prices Rising: ABS" (via BBG, see this link).

- On the data front today, we have July building permits out in a little while. This week sees terms of trade for Q2 out tomorrow, then ANZ commodity prices for August on Wednesday. Q2 volume of building work done is out on Thursday. Note though Q2 GDP is not due until Sep 18.

USD: Goldmans Sachs On USD Outlook - Ingredients For More Depreciation

The global bank on USD outlook, it sees ingredients for a more sustained depreciation, see below for details.

Goldman Sachs: "USD: A licking that keeps on ticking. The broad Dollar was relatively range-bound over July and August—a summer of carry, after all—but we think the forces that weighed on the Dollar in H1 are still active, and we increasingly see the required ingredients for a more sustained depreciation. We see the softening labor market as confirmation of the main thrust behind our view that the Dollar should fall further; the US is not outperforming the way it has for much of the last decade, and that warrants a weaker currency. More salient tariff effects will likely continue to weigh on US activity, and our economists expect more subpar growth ahead. Next week’s payrolls report will be an important marker to gauge the extent of the slowdown so far and the likely policy response ahead. Fed speakers have taken some understandable solace from the steady unemployment rate, and this will be the most important factor for the initial market reaction next week (we think a rise above 4.40 is likely required to meaningfully jostle rates- and recession-sensitive crosses like EUR/USD and USD/JPY). But, with the market already having moved some way to reflect this shifting outlook, we see two FX-specific developments that in our view help reinforce the Dollar downtrend. First, global asset allocators dealing with the Dollar dominance in their portfolios are likely to continue to seek ways to hedge the FX risk that has contributed a large portion of the variance in international portfolios this year. This is especially true under swirling institutional governance concerns that often have negative FX implications in part because they reduce global investor appetite. Second, we think recent CNY management changes reveal an important policy preference that has broad FX implications given the Renminbi’s important role as both a regional anchor and global benchmark. We have argued that, for Dollar depreciation to continue, it is likely that other regions will need to take the baton from the Euro, and that process now looks to be under way."