EM ASIA CREDIT: Xiaomi: New phone a hit

(XIAOMI, Baa1/BBB/BBBpos)

"Xiaomi 17 Phone Series’ Sales Exceed 1m, President Lu Says" - BBG

The new Xiaomi 17 phone launch going well, with production ramp up needed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

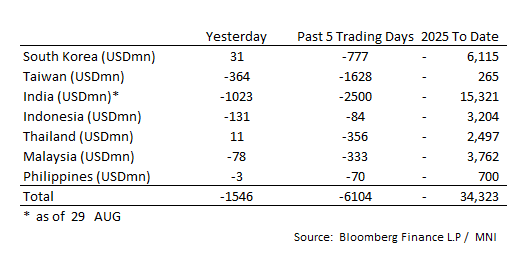

ASIA STOCKS: Very Large Outflows Dominate

One of the largest one day outflow of late across the major markets covered as India suffered a $1bn exit.

- South Korea: Recorded inflows of +$31m yesterday, bringing the 5-day total to -$777m. 2025 to date flows are -$6,115. The 5-day average is -$155m, the 20-day average is -$37m and the 100-day average of +$40m.

- Taiwan: Had outflows of -$364m yesterday, with total outflows of -$1,628m over the past 5 days. YTD flows are negative at -$265. The 5-day average is -$326m, the 20-day average of -$164m and the 100-day average of +$185m.

- India: Had outflows of -$1,023m as of the 29th, with total outflows of -$2,500m over the past 5 days. YTD flows are negative -$15,321m. The 5-day average is -$500m, the 20-day average of -$251m and the 100-day average of -$17m.

- Indonesia: Had outflows of -$131m yesterday, with total outflows of -$84m over the prior five days. YTD flows are negative -$3,204m. The 5-day average is -$17m, the 20-day average +$27m and the 100-day average -$13m.

- Thailand: Recorded inflows of +$11m yesterday, with outflows totaling -$356m over the past 5 days. YTD flows are negative at -$2,497m. The 5-day average is -$71m, the 20-day average of -$33m and the 100-day average of -$14m.

- Malaysia: Recorded outflows as of -$78m yesterday, totaling -$333m over the past 5 days. YTD flows are negative at -$3,762m. The 5-day average is -$67m, the 20-day average of -$40m and the 100-day average of -$12m.

- Philippines: Recorded outflows of -$3m yesterday, with net outflows of -$70m over the past 5 days. YTD flows are negative at -$700m. The 5-day average is -$14m, the 20-day average of -$4m the 100-day average of -$5m.

INDONESIA: VIEW: JP Morgan Expects September Cut Assuming Political Stability

August headline inflation moderated to 2.3% y/y% from 2.4% and core to 2.2% y/y% from 2.3%. JP Morgan notes that the seasonally-adjusted monthly fall in core was the weakest in almost 14 years suggesting soft consumption. Therefore it continues to expect the third consecutive rate cut on 17 September assuming that recent political turmoil stabilises. Protests continued on Monday and BI intervened to support the rupiah.

- JP Morgan notes that “while below-target inflation and BI’s pivot to a more pro-growth stance support our call for another 25bp rate cut this month, the recent flare-up in political tensions has put this call in jeopardy. For now, we stick with our easing call, but elevated tensions risk pushing out the next cut to October.”

- “Food prices notwithstanding, broad-based softness in core points to a weak consumption profile; retain September cut, contingent on political tensions stabilizing: Despite food prices putting upward pressure on inflation, this is being more than offset by broad-based softness in the core CPI basket. The latter is also consistent with continued weakness in several high-frequency indicators of consumer health.”

- “Details show that price pressures remain soft across the core basket, but a relatively large 0.9%m/m, sa drop in education services prices put additional downward pressure on core CPI in August (-0.05%-pt contribution -0.03%m/m, sa), pulling down the 3m/3m momentum on the latter from a 2%ar to 1.2%ar. The 3m/3m momentum on headline CPI also eased from 4.2%ar to 1.7%ar.”

- “A further firming of rice prices—alongside shallots, fish, and bird’s eye chillies—led food CPI to post another 0.6%m/m, sa gain in August, though its underlying momentum still remains soft due to weak earlier prints. This has led the government to release 43.7 thousand tons of rice.”

AUSTRALIA DATA: Net Exports As Forecast, No Contribution From Government

Q2 net exports contributed 0.1pp to GDP, as expected, while public demand was neutral. Q2 GDP prints on Wednesday and was forecast to rise 0.5% q/q & 1.6% y/y before this data was released. See ABS balance of payments press release here.