AUDNZD: Westpac Maintain Long Bias

Westpac remain “biased towards buying AUD/NZD on dips.”

- They’d look to enter longs around 1.0860, targeting 1.1050, with a trailing stop at 1.0810.

- Westpac note that “Australian Q2 CPI was softer than expected, locking in an RBA rate cut for 12 August. Further afield, developments in China have been encouraging. Iron ore has risen 10% during the past month, amid infrastructure announcements such the large hydro dam in Tibet. And the Shanghai Composite is up 9%. Regarding U.S.-China negotiations for an extended tariff truce, the mood is reportedly constructive, awaiting President Trump’s decision”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

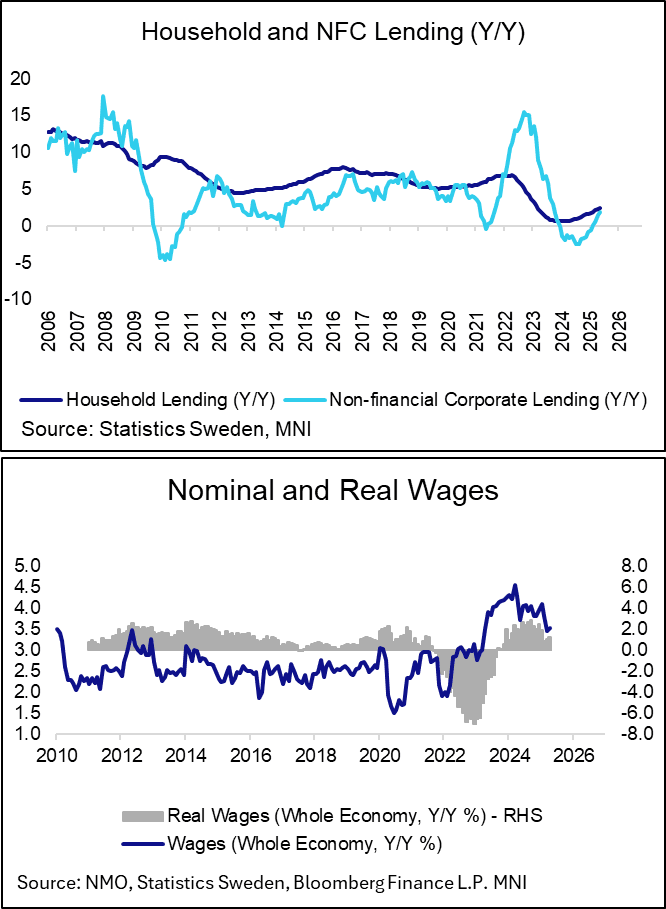

SWEDEN: Lending and Wage Data Less Dovish Than Retail Sales Report

The other Swedish data released this morning was less dovish than the very weak retail sales report. However, there’s not yet enough strength to call into question the recent dovish Riksbank guidance tilt:

Household and corporate lending growth continued to accelerate in May, with the former rising to 2.4% Y/Y (vs 2.3% prior) and the latter climbing to 1.9% Y/Y (vs 1.5% prior), the highest since September 2023. Although near term growth prospects appear soft due to heightened uncertainty, an improving credit impulse should support activity in the coming years. The Riksbank projects calendar adjusted GDP growth at 1.4% in 2025, 2.2% in 2026 and 2.1% in 2027.

April Wages: Non-manual workers wages reported by BBG fell notably to 2.5% Y/Y (vs 3.3% prior), but the more closely followed series from the National Mediation Office saw whole economy wages tick up to 3.5% Y/Y (vs 3.4% prior). Private sector pay rose two tenths to 3.5% Y/Y. The Riksbank has noted that the recent union wage agreement should support real incomes, but not threaten the inflation target.

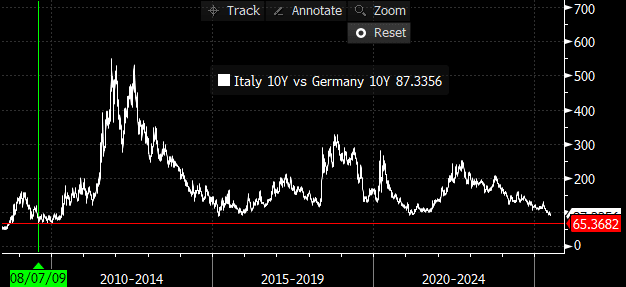

BONDS: BTP/Bund spread tests the 2015 low

- Risk On seems to favour continued BTP/Bund spread tightening, looking at the chart it is testing through the 87.5bps, which is the 2015 low.

- Next would see the 2009 low at 65.37bps.

(Chart source: Bloomberg Finance LP/MNI).

EURJPY TECHS: Support Remains Intact

- RES 4: 171.09 High Jul 23 ‘24

- RES 3: 170.47 76.4% Fibonacci retracement for Jul - Aug ‘24 downleg

- RES 2: 169.91 1.236 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 169.81 High Jun 27

- PRICE: 168.98 @ 07:59 BST Jun 30

- SUP 1: 167.92 Low Jun 24

- SUP 2: 166.94 20-day EMA

- SUP 3: 165.91 Low Jun 16

- SUP 4: 164.95 50-day EMA

The trend set-up in EURJPY is unchanged, it remains bullish. Recent gains have resulted in a break of 166.69, the Oct 31 ‘24 high. Scope is seen for a climb towards 170.47, a key Fibonacci retracement point. Note that the uptrend is in overbought territory, a pullback would unwind this condition. Support to watch lies at 166.94, the 20-day EMA. Clearance of this EMA would suggest potential for a deeper retracement.