US NATGAS: Western Canada Natgas Fundamentals

Heating demand continues to be weaker on the heals of warmer than normal weather in Western Canada. With warmer weather, reduced Northern Border exports, irregular demand from LNG Canada, and maintenance on the NGTL system, AECO is likely to remain weak until the region sees a steady uptick in demand.

- Calgary week ahead weather forecasts are calling for warmer than normal weather. Calgary cumulative HDDs decreased by 3.9 compared with the prior forecast.

- Calgary cumulative HDDs count for the next 5 days is 78.64, down 16.07 days from the 10-year normal, while the count for the next 14 days is 259.05, down 53.73 days from the 10-year normal.

- Vancouver cumulative HDDs count for the next 5 days is 37.42, down 16.64 days from the 10-year normal, while the count for the next 14 days is 4.82, down 62.46 days from the 10-year normal.

- AB outflows to SK are 5.9 Bcf/d today, down 0.06 Bcf/d from yesterday and up 0.22 Bcf/d from last week.

- Alliance US Exports reached 1.7 Bcf/d today, flat to yesterday and down 0.05 Bcf/d from last week.

- Northern Border US Exports are 0.1 Bcf/d today, down 0.01 Bcf/d from yesterday and down 0.15 Bcf/d from last week.

- Canadian exports to the Midwest are 2 Bcf/d today, down 0.01 Bcf/d from yesterday and up 0.46 Bcf/d from last week.

- Canadian net exports to the Northeast are 2.2 Bcf/d today, down 0.04 Bcf/d from yesterday and down 0.04 Bcf/d from last week.

- BC exports to the US PNW are 2.5 Bcf/d today, flat to yesterday and down 1.49 Bcf/d from last week.

- All fundamentals data is BNEF. Current figures as of publishing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Lithuania Long 10 / 20-year LITHUN: Final terms

Long 10-year:

- Spread set at MS + 95bp (Guidance was MS+105bp area and revised to MS + 95-100bp (WPIR))

- Size: E1.0bln (in line with MNI estimate)

- Books closed in excess of E1.9bln (ex JLM interest)

- Maturity: 10 March 2036

- Coupon: Short first

- ISIN: XS3175946071

20-year:

- Spread set earlier at MS +140bp (guidance was MS+145bp area)

- Size: E750mln (MNI pencilled in E1bln)

- Books closed in excess of E1.6bln (ex JLM interest)

- Maturity: 10 September 2045

- ISIN: XS3175947046

For both:

- Bookrunners: Erste Group (B&D), HSBC and Societe Generale

- Settlement Date: 10 September 2025 (T+5)

- Timing: Allocations and pricing to follow

From market source / MNI colour

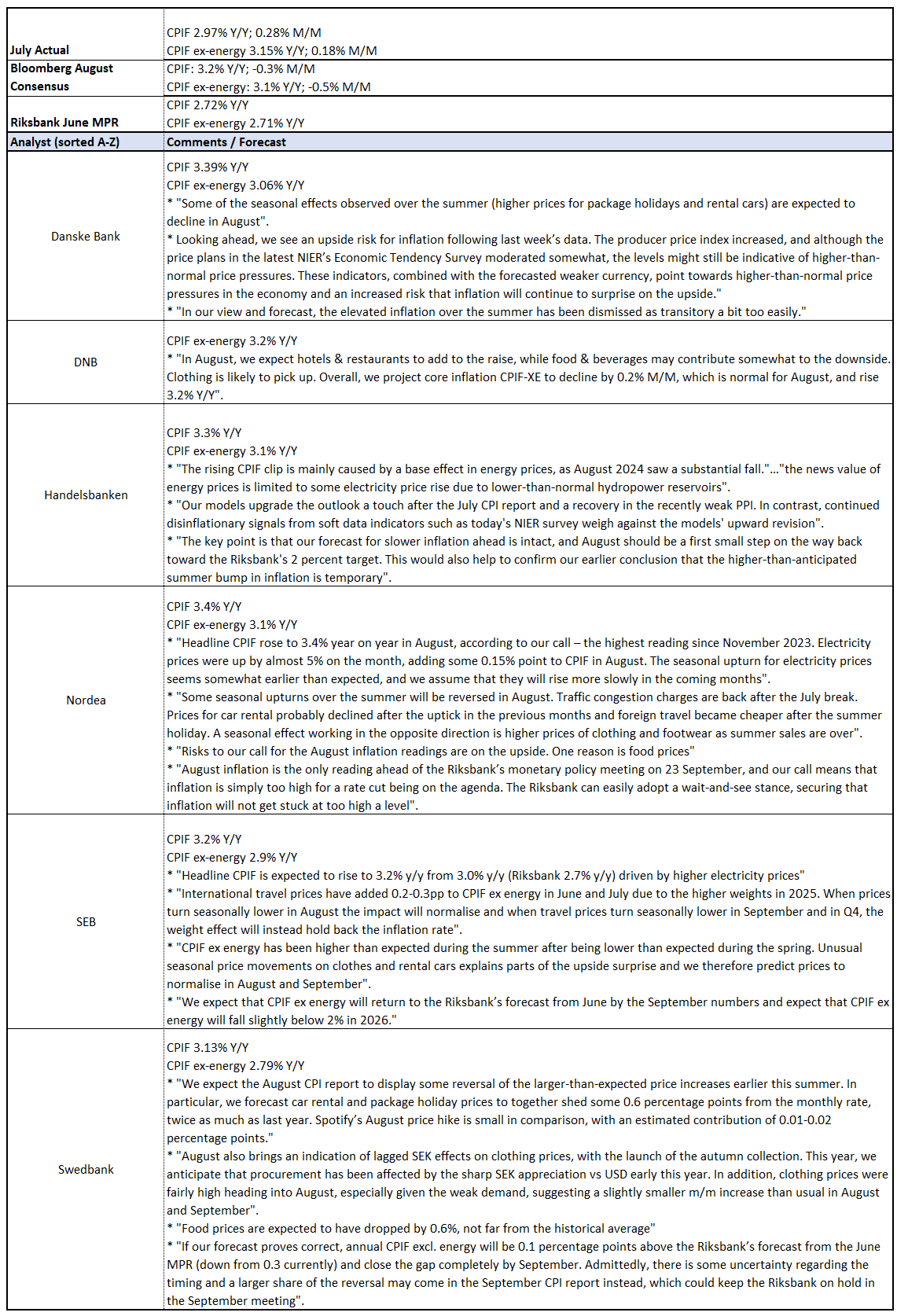

SWEDEN: August Flash Inflation Due Tomorrow; Key For Riksbank Sep Decision (2/2)

See below for a selection of analyst comments on the August inflation round:

SWEDEN: August Flash Inflation Due Tomorrow; Key For Riksbank Sep Decision (1/2)

Swedish August flash inflation is due tomorrow at 0700BST/0800CET and will be key in determining whether the Riksbank can cut rates as early as the September 23 decision. Markets currently price the September decision as a coin toss between a 25bp cut and hold.

- The median analyst surveyed by Bloomberg expects CPIF ex-energy inflation at 3.1% Y/Y (vs 3.2% prior), but five of the eleven forecasters expect a sub-3% reading. The Riksbank projected 2.71% Y/Y in the June MPR, but this projection is stale given the large upside surprise seen in June.

- The range of analyst expectations is likely due to differing assumptions on the extent to which summer inflationary impulses (e.g. for package holidays and car rentals) are unwound.

- Although full details of the report will not be available until the final release on September 11, we think that annual CPIF ex-energy disinflation of 0.3pp (i.e. a 2.9% Y/Y or below rounded reading) would be sufficient to give at least three Executive Board members confidence that the summer inflation uptick is likely to be temporary.

- This may pave the way for a (potentially not unanimously supported) cut in September, and drive a material intraday market reaction in SEK FX and rates.

- A 3.0% Y/Y rounded reading would probably also be sufficient to driven some intraday reaction, but would place more importance on the final inflation report to assess underlying inflation details. On balance, it could push the likelihood of another cut into Q4 (i.e. the November or December decisions).

- Headline inflation is expected to accelerate to 3.2% Y/Y (BBG analyst range 3.0-3.5%), from 3.0% in July. This is expected to be driven by a base effect on electricity inflation.