CREDIT RESEARCH: Weekly Fund Flows

Inflows continued for € & $ credit for the week ending Wednesday – in line with what we saw through the week in $ ETF’s there has been a slowdown in the pace for $ IG & HY while € saw a pickup in the pace of its inflows. Credit’s demand again seems duration/yield driven – US equities continued to face outflows through the first week of earnings. The divergence seems to be echoed in secondary markets - our credit weighted equity indices have fallen ~2% this year reversing just over 1/5th of its rally since late October – meanwhile credit-spreads have resumed their rally breaking earlier set tights. The missing piece driving inflows may be index yields that are +20-30bps this year as rates re-price expected CB tightening across both. The impact of this on ICR’s seems to (for now) be in the backseat for investors but is likely to get some focus as we roll through Q4 & get updated interest costs – focus may be on €IG’s where we see ICR’s currently testing pre-covid/post-GFC lows. Looking ahead earnings growth forecasted for this year should provide a buffer to ICR’s – though that relationship may be tested if forecasted better activity/earnings is met with less easing/ higher rates. Back to flows there was also reported outflows in £IG – the reporting period doesn’t capture much of post-CPI tightening in BOE curve – its pared half of that tightening since so limited impact overall & Gilt/Bund 10’s are still trading in tandem. Still the weakness in flows are echoed in secondary spreads - £IG is +3bps wider this week vs. € & $ that are 1-2bps tighter continuing its YTD underperformance.

More timely ETF flow data is pointing to outflows gathering pace in $ credit – seems focused in long-end $IG & in $HY. Fairly consensus steepening view has had a temporary pause over the last week – worries that might continue (YTD long end $IG yields have underperformed short-end by 17bps) alongside aggressive re-pricing in front end rates this week may be driving the flow skews in recent sessions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

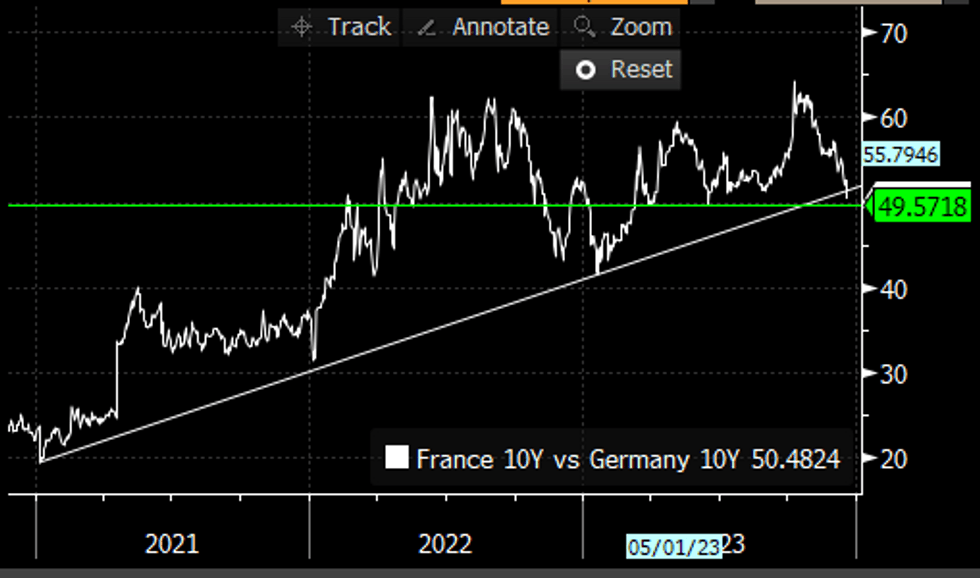

BONDS: OAT/Bund spread near 50bps

- French OAT is still leading futures higher in Europe, although still trading close to inline with Bund, which translate into a flat OAT/Bund spread so far.

- Regardless, the spread continues to make an attempt at the 50bps handle, now at 50.5bps.

- A Clear break through the latter, sees 49.57bps next.

Chart source: MNI/Bloomberg.

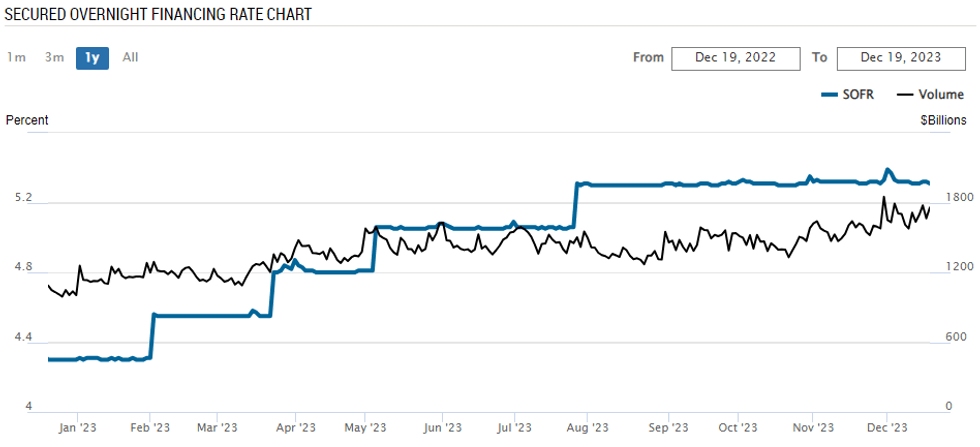

STIR: Repo Reference Rates

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 5.31%, -0.01%, $1757B

* Broad General Collateral Rate (BGCR): 5.30%, no change, $632B

* Tri-Party General Collateral Rate (TGCR): 5.30%, no change, $622B

SOFR dipped 1bp back to 5.31% yesterday after two sessions at 5.32%. It's held at 5.31/5.32% since Dec 7 after it's early Dec spike to 5.39%. Volumes of $1757bn remain at the high end of historical ranges, off the Nov 30 high of $1850bn.

Source: NY Fed

Source: NY Fed

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Dec21 $1.0850(E1.8bln), $1.0900-20(E2.5bln), $1.0950-70(E2.7bln), $1.1000(E1bln); Dec22 $1.0945-60(E1.7bln)

- USD/JPY: Dec21 Y144.75-80($1.0bln), Y145.00($1.2bln); Dec22 Y143.00($1.1bln), Y144.00($1.1bln), Y145.00($2.7bln)

- GBP/USD: Dec21 $1.2600-20(Gbp1.3bln), $1.2745-50(Gbp1.0bln)

- AUD/USD: Dec21 $0.6800-15(A$1.3bln); Dec22 $0.6650(A$1.6bln), $0.6775(A$1.1bln)

- USD/CAD: Dec22 C$1.3500($1.3bln)