US STOCKS: Weaker As Tech/Semiconductor Losses Weigh

Front S&P E-mini futures briefly touched the best intraday level of the month (7,632.00) in Asia-Pac...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Bullish Outlook

- RES 4: 187.95 High Apr 17 and the bull trigger

- RES 3: 187.56 High Apr 30

- RES 2: 186.56 76.4% retracement of the Apr 17 - May 6 bear leg

- RES 1: 186.22 High Jun 16

- PRICE: 185.56 @ 16:34 BST Jun 16

- SUP 1: 184.01 Low Jun 8

- SUP 2: 183.50 Low May 07

- SUP 3: 182.05 Low May 06 and a bear trigger

- SUP 4: 181.87 Low Mar 16

EURJPY has opened an increasingly sizeable gap with support into the Jun 8 low. The trend condition is bullish and recent weakness appears to have been corrective. Note too that MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 186.56, the 76.4% retracement for the Apr 17 - May 6 bear leg. Clearance of this level would confirm a resumption of the short-term bull cycle. Key short-term support 184.01, the Jun 8 low.

FED: Macro Since Last FOMC - Labor: Improvement Confirmed [2/2]

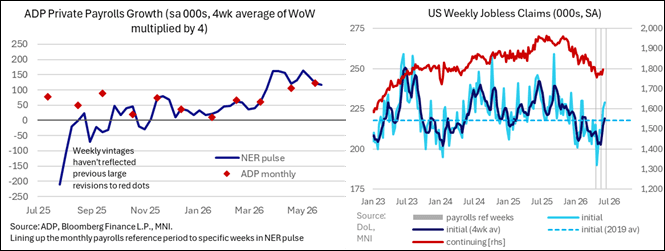

For a sense check, alternate sources such as ADP employment haven’t quite kept pace with this improvement in the BLS payrolls figures although they still point to a clear uptrend in private sector jobs hiring.

- ADP employment increased 122k in May for a three-month average of 96k whilst subsequent weekly tracking points to this early May pace having been sustained later in the month [before slightly softer read around the ~100k level into late May].

- Weekly jobless claims meanwhile offer somewhat of a warning sign on the sustainability of this broader labor market improvement, with initial claims ticking up to a seasonally adjusted 229k last week.

- Alternatively, the four-week average stands at 219k, still low by historical standards – for instance near identical to the 2019 average through 2019 at a previous period of labor market tightness – although it’s lifted from the 203k in the first half of May.

For more detail, see our latest Employment Insight - “Payrolls Surge, Hike Seen This Year” (link).

FED: Macro Since Last FOMC - Labor: Improvement Confirmed [1/2]

The below is taken from the MNI Fed Preview, found in full here.

A combination of an increasingly resilient labor market and the, for now, ongoing US-Iran conflict has driven a significant hawkish re-pricing in Fed rate expectations since the last meeting. CPI inflation readings have been impressively close to unrounded analyst estimates in the two monthly updates although underlying input cost inflation has been far stronger than expected and points to a strong pipeline of price pressures. Core PCE tracking suggests it could hit 3.4% Y/Y in May for a notable further acceleration away from the 2% inflation target.

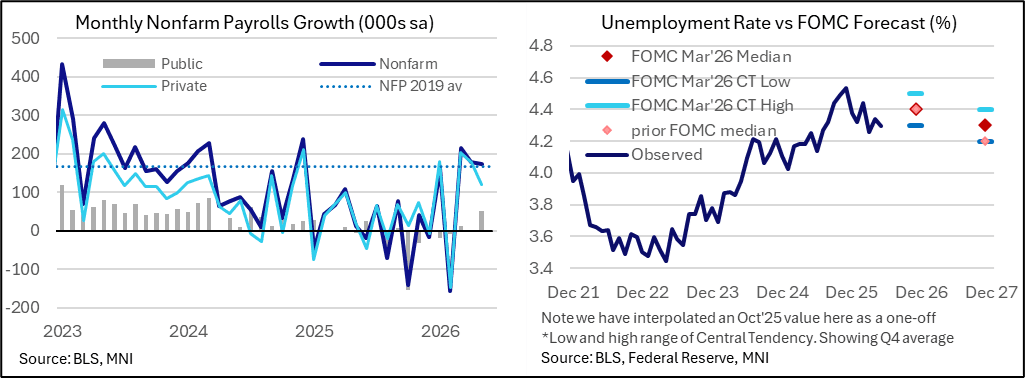

Labor Market: Improvement Confirmed

- The two nonfarm payroll reports and a slew of generally solid labor releases since the late April meeting have significantly altered the market backdrop as the downside labor risks to the dual mandate recede, leaving upside inflation risks firmly in focus.

- The latest payrolls report for May saw a seasonally adjusted monthly increase of 172k, far stronger than consensus of 88k, following 179k in April and 214k in March after a sizeable boost from a two-month upward revision of 93k. May jobs growth may have been supported by the seasonal adjustment process and a weather boost, but broader trends are still impressively strong.

- That includes a three-month average of 188k, the highest since Mar 2024, although the six-month average of 92k helps better smooth out significant volatility earlier in the year and is at a joint high with Feb 2025.

- When thinking about payrolls growth, it’s also worth noting QCEW data released in the inter-meeting period tentatively point to small positive revisions come the benchmark adjustment due in early 2027 in a change from the material negative revisions of the previous two years.

- The unemployment rate meanwhile was as expected in May at a healthy 4.30% for levels close to estimates of the natural rate. It continues its broad stabilization since the summer although in doing so suggests that dwindling estimates of payrolls breakeven pace, some around zero, had become overly pessimistic.