EUR: Viewpoint - Performance Closely Tied to Dollar Pegs

The EUR/USD has been the main beneficiary of the prevalent USD weakness this year. Robin Brooks gave his viewpoint on X around the Euro and Europe and how closely it is tied to Asia and in particular China.

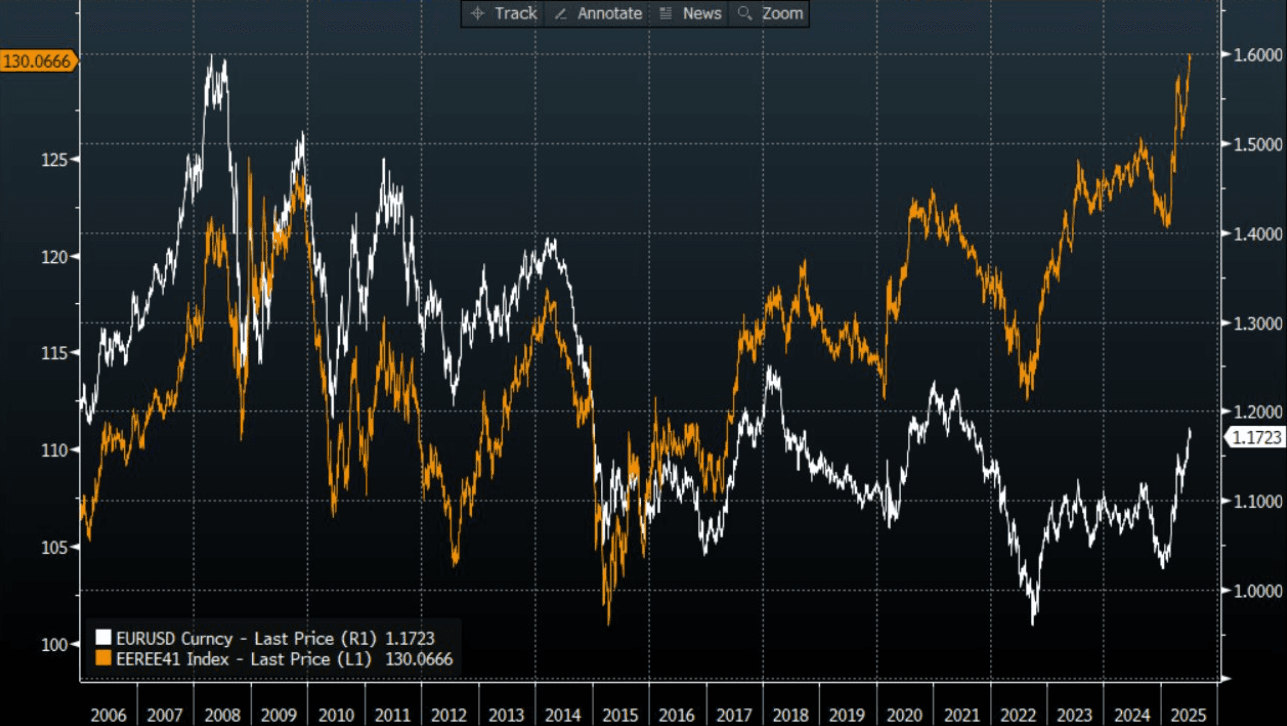

- Robin Brooks on X:“Euro makes new all-time highs every day in trade weighted terms. Many countries - above all China - peg to the Dollar. That supercharges the rise in Euro vs USD (white), taking Euro to stratospheric levels in trade-weighted terms (orange). Deflation is coming for the Euro zone...” See Graph below.

- “There's an absurd amount of optimism in the Euro zone currently. Let me put Euro zone growth - or lack thereof - into perspective. Since 2007, the US state of Alabama (AL) has outgrown Germany (GE) in real per capita terms. Italy (IT) is worse than Louisiana (LA). Come on…”

- Brad Setser on X: “Personally I prefer to look at the inflation adjusted index for the euro but there is no doubt that China's close tie (de facto peg at times) to the euro over the last 2 years has become a problem for the euro right now.”

- “The Europeans have historically treated China's currency peg as someone else's problem for a host of institutional reasons. But a yuan that is between 7.1 and 7.3 v the dollar (a very weak CNY v the USD!) is a real problem for the EU when the dollar is falling. Agree w/ Robin”

Fig1: EUR/USD Vs ECB Nominal Effective Exchange Rate Of The Euro Against Trading Partners

Source: MNI/@robin_j_brooks/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA MAY EXPORTS +4.8% Y/Y VS MEDIAN +6.0% Y/Y: CUSTOMS

- CHINA MAY EXPORTS +4.8% Y/Y VS MEDIAN +6.0% Y/Y: CUSTOMS

- CHINA MAY IMPORTS -3.4% Y/Y VS MEDIAN -1.0% Y/Y: CUSTOMS

- CHINA MAY TRADE SURPLUS +$103.2 BLN VS MEDIAN +$101.1 BLN

AUD: AUDUSD Stronger & Holding Break Above 65c As Equities Rally

AUDUSD has trended higher so far through today’s APAC session to be up 0.3% to 0.6510 supported by better risk appetite which is driving equities higher following the US’ post-payroll rally, and US yields and the dollar are lower (USD BBDXY -0.2% after Friday’s +0.3%). The pair is approaching resistance at 0.6538.

- AUDJPY has range traded and is currently around 94.06 after a low of 93.97 and a high of 94.24. AUDNZD is flat at 1.0790 off the intraday peak of 1.0803.

- AUDEUR is 0.1% higher at 0.5702 holding a break above 0.5700. AUDGBP is off its high of 0.4807 but is still up 0.1% to 0.4802.

- Equities are rallying with the Nikkei up 1.0% and Hang Seng +1.5% but the S&P e-mini is down 0.2%. The ASX is closed for a holiday. Oil prices are slower lower with WTI around $64.55/bbl. Copper is 0.3% higher and iron ore is off its intraday low to be just over $95/t.

- Later US April wholesale data and May NY Fed 1-yr inflation expectations print. The ECB’s Elderson speaks.

CHINA: Little Reaction To Inflation Daa, CNY & Equities Following Broader Trends

China asset markets aren't showing a strong reaction to the May inflation data. To recap, the CPI remain in deflation, albeit slightly above market expectations (-0.1%y/y, versus 0.2% forecast). The PPI continued to show worsening deflation at -3.3%y/y (-3.2% was forecast and prior was -2.7%). USD/CNH is down slightly, last near 7.1845/50. Broader USD sentiment is struggling to hold Friday's gains, the BBDXY last down 0.20%, which is likely aiding CNH, albeit with the usual lower beta.

- Local equities are up +0.30% for the CSI 300, last above 3880, so within recent ranges. Hong Kong markets are +1.35%. We have US-China trade talks resuming in London later, while some softening in China's rare export stance (for both the US and EU) may be helping aid sentiment ahead of the talks.

- Bond yields onshore are not showing a strong direction trend, the 10yr last 1.68%, while the 2yr was near 1.4%, still close to recent lows.

- Inflation data underscore the need for on-going policy support to maintain domestic momentum to avoid further deflationary pressures. Onshore media suggests infrastructure spending will spending will pick up while incremental policy shifts are also likely (see this link).

- Very large scale stimulus seems unlikely unless US-China trade talks break down and high tariffs by the US are reinstated.