NEW ZEALAND: VIEW: Westpac Sees Headline In Band But Above 2% In 2025

Q1 CPI printed above consensus and the RBNZ’s February forecast of 0.8% q/q & 2.4% y/y. Westpac notes that there had been large monthly price increases in volatile items since the RBNZ made its projection and which are not important for monetary policy. It believes “the underlying trend in inflation is looking well contained” and that headline will stay in the band over the year but remain above 2% as imports won’t be as disinflationary as they have been. The RBNZ’s own core inflation data is published today at 1500 NZST/1300 AEST.

- There were “large increases in the prices of volatile items like food and overseas holiday costs, which are not the key focus for monetary policy. In addition, today’s result was boosted by a change in how tertiary education costs are measured.”

- Westpac doesn’t “expect a return to the high rates of tradables inflation that we saw in the wake of the pandemic. However, with the drop in the NZ dollar since late last year and prices already picking up, tradables inflation is expected to continue pushing higher over the coming months. That’s important as it will limit the downside for overall inflation over the remainder of this year.”

- “The stronger than expected non-tradables inflation in the March quarter was mainly due to the large increase in education costs … more generally, we are seeing pressures easing, consistent with the softness in domestic activity which has seen muted growth in wages and service sector prices. We’ve also seen an easing in rents and subdued increases in the cost of new housing. Price changes on this front will be a key focus for the RBNZ.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Korea Enjoys Second Day of Big Inflows.

South Korea has recorded another day of solid inflows whilst outflows dominated elsewhere.

- South Korea: Recorded inflows of +$346m yesterday, bringing the 5-day total to -$858m. 2025 to date flows are -$5,203m. The 5-day average is -$172m, the 20-day average is -$192m and the 100-day average of -$119m.

- Taiwan: Had outflows of -$303m yesterday, with total outflows of -$3,266 m over the past 5 days. YTD flows are negative at -$14,010m. The 5-day average is -$653m, the 20-day average of -$548m and the 100-day average of -$197m.

- India: Saw outflows of -$98m as of the 13th, with a total outflow of -$702m over the previous 5 days. YTD outflows stand at -$15,932m. The 5-day average is -$140m, the 20-day average of -$294m and the 100-day average of -$201m.

- Indonesia: Posted outflows of -$54m yesterday, bringing the 5-day total to -$228m. YTD flows are negative at -$1,648m. The 5-day average is -$46m, the 20-day average is -$53m the 100-day average of -$33m.

- Thailand: Recorded outflows of -$39m yesterday, totaling -$188m over the past 5 days. YTD flows are negative at -$942m. The 5-day average is -$38m, the 20-day average of -$40m the 100-day average of -$19m.

- Malaysia: Experienced outflows of -$64m Friday, contributing to a 5-day outflow of -$303m. YTD flows stand at -$1,699m. The 5-day average is -$61m, the 20-day average of -$46m the 100-day average of -$33m.

- Philippines: Saw inflows of +$6m yesterday, with net inflows of +$14m over the past 5 days. YTD flows are negative at -$213m. The 5-day average is +$3m, the 20-day average of -$3m the 100-day average of -$7m.

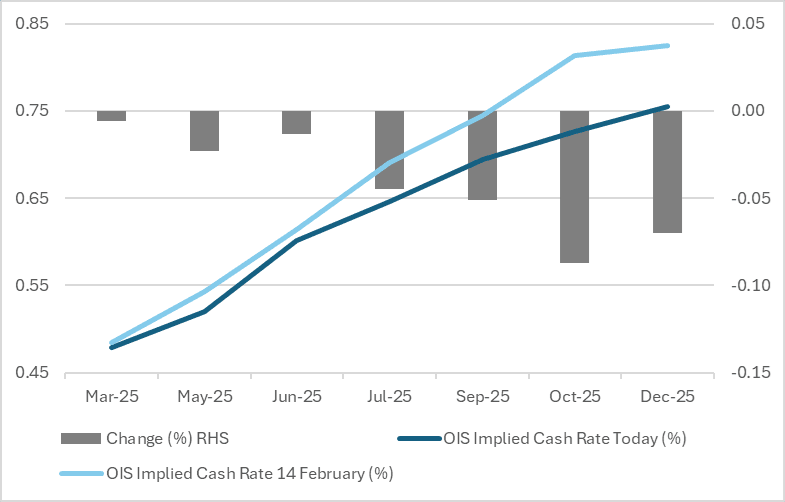

STIR: BoJ-Dated OIS Pricing Softer Than Mid-February Levels

BoJ-dated OIS pricing has softened 1-8bps since mid-February, reflecting uncertainty over the BoJ’s willingness to tighten policy amid fluctuating domestic and global economic conditions.

- The move over the past two weeks leaves pricing mixed compared to late January levels - flat to 3bps firmer out to June but 1-2bps softer beyond.

- Markets currently assign a 1% probability to a 25bp hike at this week’s meeting, a cumulative 50% chance by June, and fully price in a 25bp increase by October — in mid-February a hike was fully priced by September.

Figure 1: BoJ-Dated OIS – Today Vs. Friday 14 February

Source: MNI – Market News / Bloomberg

CHINA PRESS: Additional Treasury Funds To Drive Consumption

Beijing’s CNY300 billion special treasury funds for consumer goods trade-ins are expected to drive a net increase of CNY700-800 billion in consumption and quicken spending on goods by 1.5-1.6 percentage points, said Wang Qing, chief macro analyst at Golden Credit Rating. Government childcare subsidies could reach CNY100 billion, Wang estimated, based on a CNY10,000 subsidy for 10 million newborns, though policies may vary across local governments. (Source: 21st Century Business Herald)