CNH: USD/CNY Fixing Edges Up, Error Term Widens

The USD/CNY fix printed at 7.1526, versus a Bloomberg consensus estimate of 7.1901.

- Today's fixing nudged a little higher, in line with broader USD gains, but the fixing error widened too -375pips from -242pips yesterday (so it also took some of the USD rise). This was the widest fixing error since May 9.

- USD/CNH is little changed so far today, last near 7.1815.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA SETS YUAN CENTRAL PARITY AT 7.1789 MON VS 7.1772

- CHINA SETS YUAN CENTRAL PARITY AT 7.1789 MON VS 7.1772

NEW ZEALAND: Slower Growth Expected But Inflation Eases To Band Mid-Point

The NZIER June survey of forecasters has been published and is showing a downward revision to NZ growth this financial year and next compared with the March results. FY25 is down 0.3pp to 1.1% and FY26 0.2pp to 1.9%, the recovery remains in place supported by lower rates. Residential investment is the main driver of the projection changes with the NZIER citing “reduced pipeline of housing construction”. However, inflation was revised up 0.2pp to 2.5% for FY25 but FY26 was unchanged at 2.2% and it holds around the RBNZ’s 2.0% band mid-point thereafter.

- Despite expectations for slower growth the unemployment rate was revised down 0.1pp to 5.1% in FY25 & FY26 but employment growth is weaker in FY25 down 0.3pp to -0.7% but FY26 remains at 1.4%.

- Forecasters revised up near-term export expectations due to increased demand for food stuffs. However, the current highly uncertain global growth environment and increased trade protectionism drove a downward revision in FY27 with FY28 unchanged.

- See NZIER “Consensus Forecasts” here.

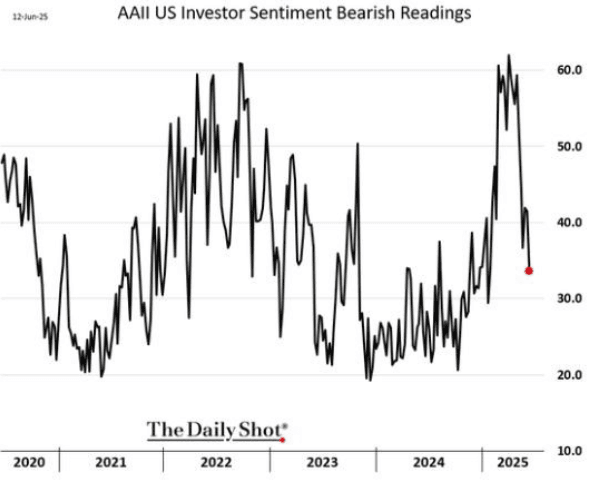

US STOCKS: Market Seems Gun-Shy To Short It Again

The ESM5 Friday night range was 6006.00 - 6082.50, Asia is currently trading around 6040. A potentially protracted Middle East war, a short oil market surging and President Trump commenting the US “could get involved”, and still the US stock market continues to be very well supported on any dip. A market that was caught very short all the way and has now been forced back in seems very reticent to attempt to sell it again.

- Bob Elliott on X: “ A lot of bears have capitulated.” See Graph Below

- Lance Roberts on X: “Equity allocations across major investor groups have reached a record 53%, while allocations to debt and cash have fallen to multi-decade lows of 18% and 13%, respectively. Despite all of the headline concerns, investors are chasing risk assets more than ever. Of course, that also highlights increased vulnerability to shifts in risk sentiment.”

- “In 2025, U.S. companies are announcing record share buybacks, with repurchases projected to surpass $1 trillion for the year—a move intended to support stock prices and improve financial metrics.”

- Friday night saw strong demand back below the 6000 area and at 1 point it had almost erased all its losses before falling away into the close. This morning US futures initially tried lower but in very similar price action have bounced back and they are currently trading positive in our session. ESU5 +0.14%, NQU5 +0.22%

- Momentum type funds and share buybacks have kept the market well supported as an underweight market has been forced to reenter. Share buybacks are set to enter their blackout period starting this week, will this be the signal for a potential pullback ?

In the short-term stocks look overbought, if the S&P can’t hold above 6000 we could see the start of some sort of a retracement. The first buy-zone is back towards the 5700 area where demand could be expected.

Fig 1: US Investor Bearish Sentiment

Source: @SoberLook, The Daily Shot