CNH: USD/CNH Holds Near 7.1500 Despite Equity Pullback

Spot USD/CNH sits near 7.1530 in early Thursday dealings, after posting little net change for Wednesday's session. Yesterday's intra-session low in the pair was at 7.1457, close to late July lows of 7.1441. The focus is likely to remain on downside risks in the pair, although some of the recent equity outperformance stalled on Wednesday. Broader USD indices were down a touch for Wednesday. Spot USD/CNY finished up at 7.1517, while the CNY basket tracker edged a little higher to 96.57.

- For USD/CNH spot technicals, little has changed. The downside focus will remain on a test into the 7.1400/7.1500 region. The USD/CNY fixing bias remains skewed lower, while USD/CNY spot traded at fresh YTD lows yesterday of 7.1458.

- The lower US Tsy yield backdrop, particularly at the front end, is a CNH support, although US-CH 2yr spreads are still above 2025 lows.

- Focus today may be on equity market trends and whether we see any negative sentiment spill over to CNH. Yesterday, the CSI 300 closed down 1.49%, pushing the index back under 4400, with sharp losses post the lunch time break. In Wednesday US trade, the Golden Dragon index lost 2.58%, the first decline in six sessions.

- There didn't appear a direct catalyst for the move: BBG noted: "Concerns are mounting over a surge in leveraged trading and speculative bets on Chinese technology stocks. Margin financing has climbed to its highest level in a decade, while producer prices remain mired in nearly three years of deflation."

- The local data calendar is empty until Sunday's official PMI prints.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

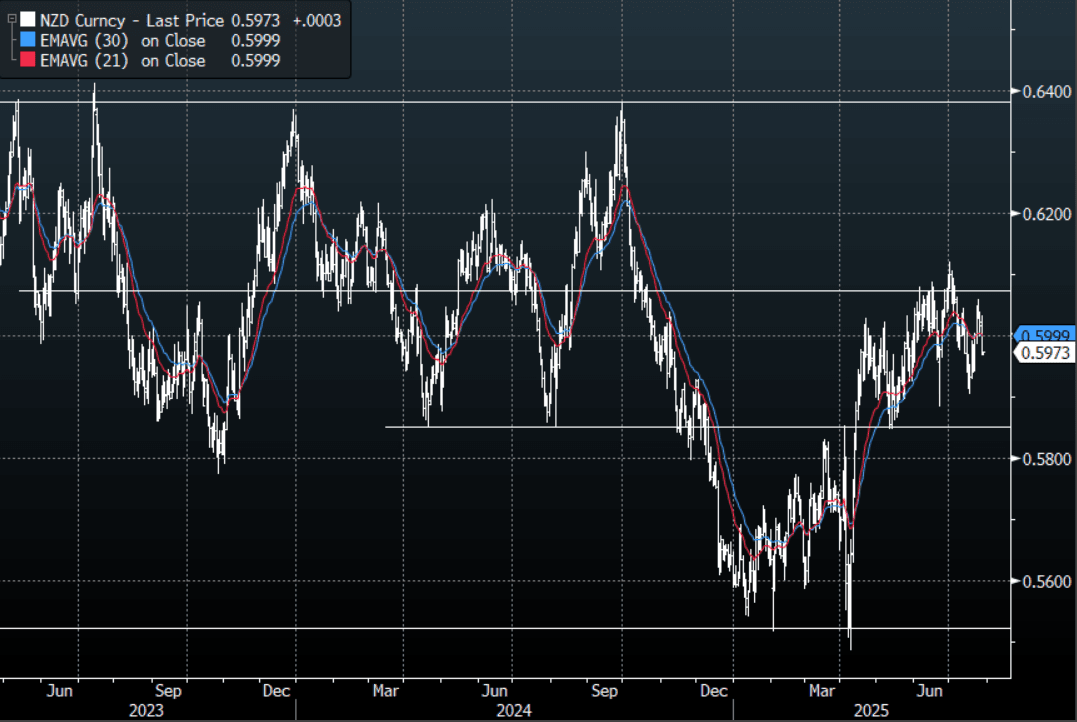

NZD: NZD/USD - Fails Above 0.6000 As The USD Makes A Recovery

The NZD/USD had a range overnight of 0.5967 - 0.6010, Asia is trading around 0.5975. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. There is lots of event risk coming up this week and we are also heading into the corporate month-end today so there could be an extra demand for USD’s further pressuring the USD shorts. Support now seen back towards the 0.5850/0.5900 area.

- Bloomberg - “New Zealand’s recovery from deep recession in 2024 looks wobbly, writes Bloomberg Economics’ James McIntyre. Spending remains contained, and the labor market is weakening. While the direct impacts from tariffs are minimal, the spike in uncertainty is taking a toll. The central bank has already cut rates aggressively. But the recovery needs more stimulus. With fiscal policy tight and migration slowing, the case for the RBNZ to loosen monetary policy further in 2025 and 2026 is stronger.”

- “China’s latest move to offer cash handouts nationwide to entice people to have children marks a new step in establishing a long-term subsidy program for boosting the birth rate.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30), 0.5965(NZD424m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- Data/Event :

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE 10-YEAR TECHS: (U5) Fades Through Thursday

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.625 @ 19:28 BST Jul 28

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures traded under pressure for much of last week, keeping prices subdued and within range of the recent pullback lows. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

US TSYS: Yields Edge Higher, Led By The Long-End

TYU5 reopens at 110-25, up 0-01 from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.3660% - 4.4178%, closing around 4.41%.

- Treasury yields ended generally higher overnight; led by the long-end causing the yield curve to steepen (2s10s +1.75 at 47.785, 5s30s +1.54 at 98.705).

- MNI US-EU: European Leaders Divided On Deal To Avert Worst Of Tariffs. A number of high-ranking European politicians have expressed their disappointment at the trade deal agreed between US President Donald Trump and European Commission President Ursula von der Leyen over the weekend in Scotland. Most prominent has been French PM Francois Bayrou, who posted on X: “It is a dark day when an alliance of free peoples, united to assert their values and defend their interests, resigns itself to submission”. Chair of the European Parliament's Trade Committee, German MEP Bernd Lange said "My first assessment: not satisfactory. This is a lopsided deal. Concessions have clearly been made that are difficult to accept."

- MNI US DATA: Dallas Mfg Rounds Out Regional Fed Surveys Eyeing Nudge Higher In ISM. The Dallas Fed manufacturing index was stronger than expected in July as it increased to 0.9 (cons -9.5) from -12.7 in June. It’s a third consecutive increase from the -35.8 in April, at what had been its lowest since Jan '16 outside of Mar-May 2020, and leaves it at the first positive reading since January.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward.