CHILE: USDCLP In Consolidation Mode, Pension Regulator Considering New Measures

- The Chilean peso has opened firmer, after posting modest gains against the dollar yesterday, buoyed by an uptick in copper prices. As noted, USDCLP is currently in consolidation mode, with medium-term resistance seen at 977.57, the Sep 2 high.

- Meanwhile, Hacienda has said that it will continue to hold dollar auctions totalling up to US$300 million per week between October and December of this year, unchanged from the previous quarter. As usual, it said that the amount of this announcement is subject to change, considering possible changes in financing needs or significant changes in market conditions.

- In other news, Chile’s pension regulator is studying the best way to regulate how pension funds are using derivatives, according to a report in Mercurio. The regulator’s superintendent, Osvaldo Macias, said that he is very worried and that at the moment it is possible for the funds to take more risk than is prudent. He said that the measures will be announced soon.

- With no macro data due the rest of this week, attention turns to key Sept CPI data scheduled for Oct 08, where focus will be on the ex-volatiles measure which has been tracking above expectations, prompting the BCCh’s recent hawkish tilt.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWEDEN: Riksbank Sep Cut In The Balance Ahead Of Flash Inflation Data

The Riksbank September decision is priced as essentially a coin toss between a hold at 2.00% and a 25bp cut. This pricing is justified, in our view. Thursday’s August flash inflation report is the key focus for Riksbank Executive Board members and markets, and a soft print would tilt expectations in favour of a September cut despite a better set of Swedish activity signals over the past few weeks. We will send out a more comprehensive preview of the August inflation release tomorrow.

See below for a concise update on Swedish macro developments:

- Riksbank Commentary: The August Minutes portrayed a board that is willing to deliver another rate cut this year, potentially as soon as September, conditional on spot inflation rates declining back towards the previous projections.

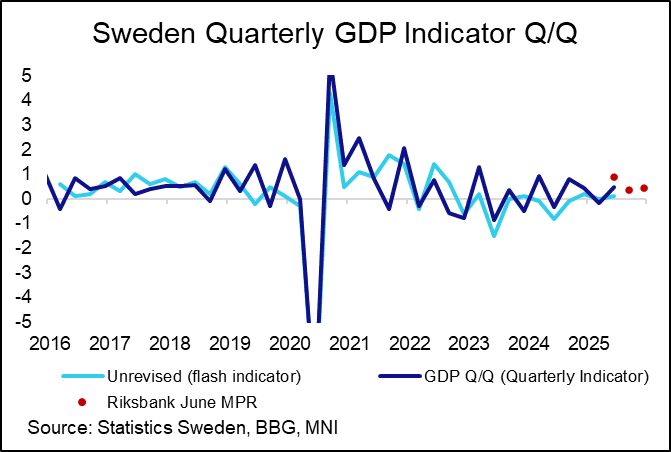

- Activity Data: Q2 GDP was upwardly revised to 0.5% Q/Q (vs 0.1% flash), but was still substantially below the Riksbank’s 0.9% projection from the June MPR. The details of the report were mixed, with positive contributions from consumption and investment, a significant positive contribution from inventories and a negative contribution from net trade. Household and business lending growth also accelerated in July.

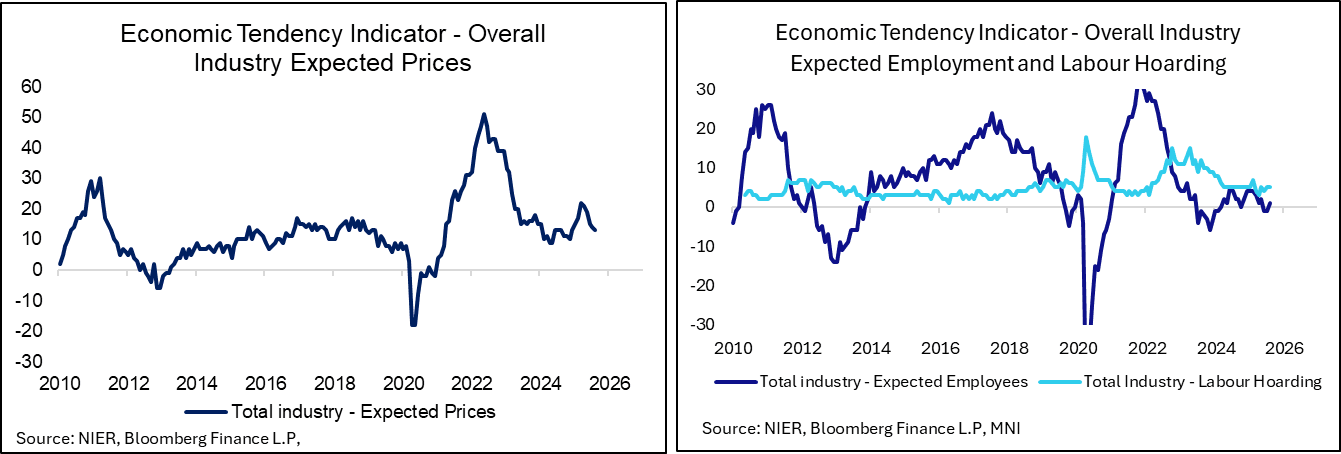

- Sentiment: The August Economic Tendency Indicator rose to a 6-month high of 96.0 (vs 94.3 prior), and the August manufacturing PMI also rose to a multi-year high of 55.3. However, more dovish signals in the Economic Tendency Survey came from another inch lower in business price plans alongside still-subdued employment expectations.

- Fiscal: Finance Minister Svantesson announced that the 2026 budget (set to be announced on Sep 22, the day prior to the Riksbank decision) will contain SEK80bln of expansionary commitments. This was well above NIER’s latest expectation of SEK34bln and also analyst estimates we had seen in recent weeks (the highest we had seen was SEK75bln from Swedbank).

- SEB have written that the proposed expansion is “unlikely to have notable impact on near-term [the] Riksbank outlook”, but “on margin reduces [the] probability of second cut this autumn”.

PIPELINE: Corporate Bond Roundup: Asia Banks Kick Off September US$ Issuance

- Date $MM Issuer (Priced *, Launch #)

- 09/02 $Benchmark MUFG 6NC5 +105a, 11NC10 +120a, PerpNC10 6.875a

- 09/02 $Benchmark Sumitomo Mitsui Trust 3Y SOFR, 5Y, 11NC10 +145a

- 09/02 $Benchmark Kingdom of Saudi Arabia Sukuk 5Y +95a, 10Y +105a

- 09/02 $Benchmark Mitsubishi 3Y +70, 3Y SOFR, 5Y +80a, 10Y +95a

- 09/02 $Benchmark Credit Agricole PerpNC10 7.625%a

- 09/02 $Benchmark Norinchukin 5Y +125a, 10Y +140a

- 09/02 $Benchmark Nomura 10.75NC5.75 +160a

- 09/02 $Benchmark HSBC 11NC10 +170a

- 09/02 $Benchmark ING PerpNC7 7.37%a

- 09/02 $Benchmark Orix Corp 5Y +100a

SPAIN: Spain Plans To Write-off E83bln of Regional Debt - Bloomberg

Latest from Bloomberg

- "Spain is moving ahead with a plan to write-off €83.2 billion ($96.8 billion) of regional governments’ debt as part of broader political negotiations to bolster support for Prime Minister Pedro Sanchez."

- "The measure, which would apply to loans owed to the central government, “is historic” and will allow Spain’s 17 regions to “regain financial and political independence”, Budget Minister Maria Jesus Montero said at a press conference on Tuesday. The measure is part of the investiture agreement signed with Catalan separatist party ERC to elect Sanchez as premier in 2023 and will need parliamentary approval."

- "The government has said that, if approved by parliament, the move won’t affect the central administration’s debt levels. Madrid had originally announced the plan in February"

On the last bullet point, current central government debt would be unaffected because the E83bln transfer from the central to regional government's has already been carried out (and thus, is already "accounted for" in Spain's fiscal/issuance plans). The aforementioned plan to write-off the debt would essentially transform this E83bln transfer into a subsidy (rather than a loan). As such, the move could in theory affect future debt levels, relative to the counterfactual of the regional government debt having been paid back.