CROSS ASSET: USD Firms, Equities Slip on Waller Report

USD sees support on the back of the Waller sources headline - EUR/USD breaks to a new daily low while equities see a spell of weakness. E-mini S&P down to 6390.00, but still off overnight lows at 6364.25.

- While Waller (with Bowman) dissented against the last rate decision and opted to cut rates, his credibility as an insider candidate relative to Hassett is showing in this market reaction. As the piece notes: "Trump advisers are impressed with Waller’s willingness to move on policy based on forecasting, rather than current data, and his deep knowledge of the Fed system as a whole"

- This report doesn't the answer the question on who could replace Kugler after her resignation - with a separate sources report yesterday suggesting advisers were pushing for a temporary candidate to bridge the gap to next year - buying time to appoint Powell's successor.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Session Lows Intact, Curve Holds Steeper

Gilt bears are unable to force a break below session lows.

- Note futures pierced next support at 91.50 and bears will now target the June 2 low at 91.16.

- Yields 1-6bp higher, curve steeper.

- 2s10s set for the highest close since April, 5s30s set for the first close above 140bp since ’17.

- Fundamentals point to further steepening pressure, but pre-existing positioning and activist approaches re: preventing yield spikes from the DMO & BoE present risks to that idea.

- Note the June 2 high in 10-Year yields (4.702%) is ~5bp above today’s high

- The gilt/Bund spread has tended back towards 200bp after failing to break below the April closing low last week (see earlier bullet for more colour there).

- Hawkish adjustments in the short end given moves further out the curve.

- SONIA futures 0.5-5.5 lower.

- BoE-dated OIS 0.5-2.0bp less dovish on the day, showing 52bp of cuts through year-end. Next cut still more than fully discounted through September, with over 80% odds of such a move priced through August.

- Macro headline flow remains light at this stage.

- UK headline flow has been light since this morning’s OBR release, which, although it failed to generate a meaningful market reaction, underscored some of the well-documented fiscal challenges that the country faces at present.

- The BoE will present its latest FSR tomorrow, that shouldn’t be much of a market mover.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.007 | -21.0 |

Sep-25 | 3.949 | -26.9 |

Nov-25 | 3.780 | -43.7 |

Dec-25 | 3.697 | -52.1 |

Feb-26 | 3.568 | -64.9 |

Mar-26 | 3.538 | -67.9 |

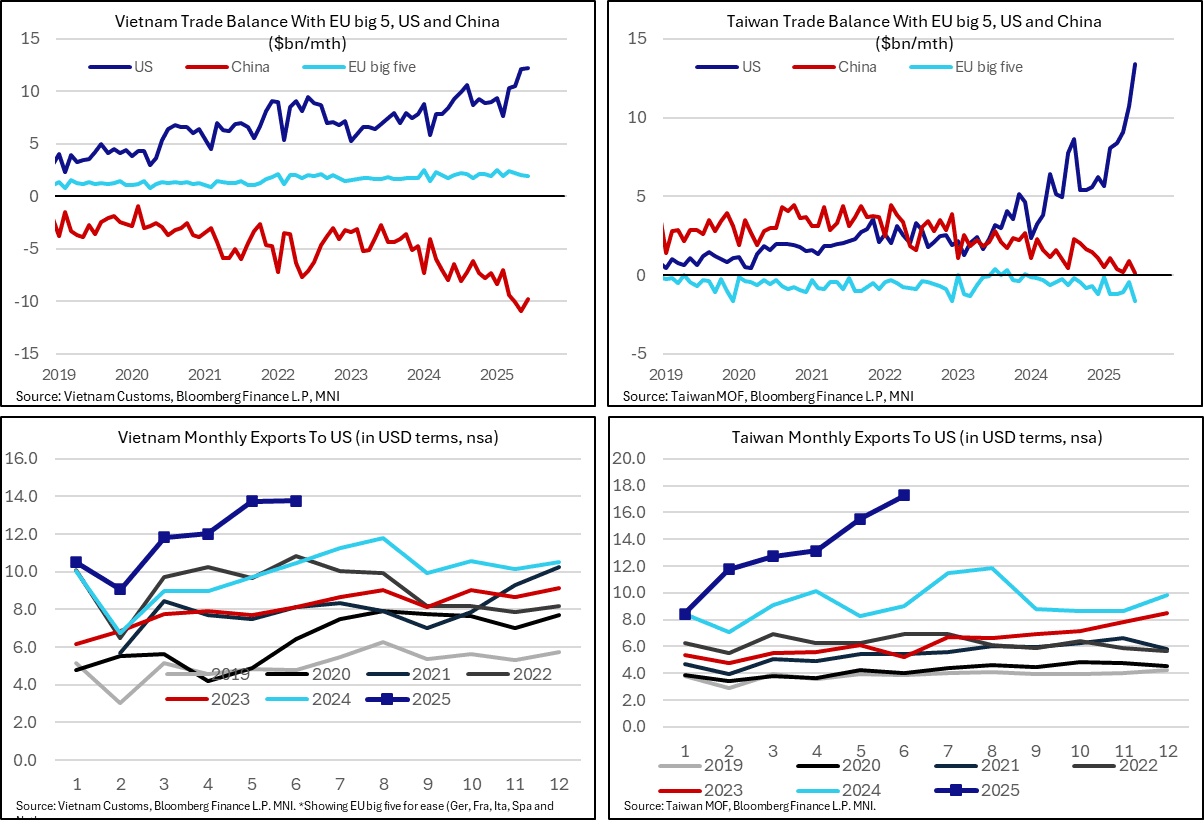

INTERNATIONAL TRADE: Vietnam and Taiwan Exports To US Continue To Grow Strongly

Vietnamese and Taiwanese exports to the US continued to exhibit strength in June, with Chinese transshipments and tariff front-running seemingly remaining prevalent. With Eurozone and US trade data only (or in some cases, not even) updated for May, the Asian data provides a more timely indicator of global goods trade flows.

- Vietnamese exports to the US have risen more than 30% Y/Y in each month since February 2025. Meanwhile, Taiwanese exports averaged 45% Y/Y between February and April, before jumping to 87% Y/Y in May and 91% Y/Y in June.

- Vietnamese import growth from China has averaged 35% Y/Y between February and June, above the 30% Y/Y averaged through 2024. In Taiwan, 24% Y/Y average growth since February contrasts with a 13% Y/Y average in 2024.

- The US and Vietnam agreed on a trade deal last week. Vietnamese exports will be subject to a 20% tariff rate, with any goods deemed to be transshipments (i.e. from China) facing a 40% levy. A reminder that Vietnam was faced with a 46% reciprocal tariff rate following the original April 2 Liberation Day announcement.

- Focus in the next few months will be on whether the Vietnamese trade deficit with China narrows as a result of this agreement, or if current trends extend (which could be interpreted as Asian exporters calling the US’ bluff in being able to accurately identify transshipments).

- While there were fairly benign developments in Vietnamese net trade with the EU in June (proxied by the five largest EU economies), the Taiwanese trade deficit with the EU widened to USD1.7bln from USD0.4bln in May. This was due to a USD0.5bln rise in Taiwanese imports from both Germany and the Netherlands – the latter likely a function of ASML’s activities in the country.

- Chinese trade data for June is due next Monday (14th July), which will give an update on direct exports to the US, and whether tariff-related disinflationary trade diversion to the Euro area is being realised.

US TSY OPTIONS: Recent 10Y Trade

- +15,000 TYU5 113 calls, 13

- 1,500 TYQ5 109/109.5/110.5 broken put flys, 17 ref 110-23.5

- 4,300 Wed wkly TY 111/111.25 call spds (exp Wed) vs. wk2 TY 111.25 calls (expire Fri)