FED: US TSY 7Y AUCTION: NON-COMP BIDS $96 MLN FROM $44.000 BLN TOTAL

Aug-28 16:45

- US TSY 7Y AUCTION: NON-COMP BIDS $96 MLN FROM $44.000 BLN TOTAL

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: MNI BoC Preview-July 2025: Data Calls For Further Patience

Jul-29 16:39

We've published our BOC preview for this week's meeting - Download Full Report Here

- Data developments since the June meeting mean the Bank of Canada will maintain the overnight rate target steady at 2.75% for a third consecutive meeting on Wednesday.

- Better-than-expected labour market data and stubbornly high core inflation, combined with continued uncertainty over the US-Canada trade dispute, give the BOC impetus to wait until its next meeting in September before committing to further moves.

- While the BOC is likely to retain its easing bias, judging from market pricing, the question now is whether the BOC’s easing cycle is at an end after 225bp of cuts through March.

- We note that while most analysts still expect at least one further cut, median expectations of the terminal overnight rate as tracked by MNI have crept up to 2.25% from 2.125% since prior to the June meeting.

- The latest Monetary Policy Report is likely to include two tariff-related scenarios as in the previous round, with a less negative estimate for Q2 GDP and slightly higher core inflation.

- The policy statement should reflect this better-than-expected economic activity evolution as well, but once again we do not expect any firm forward guidance.

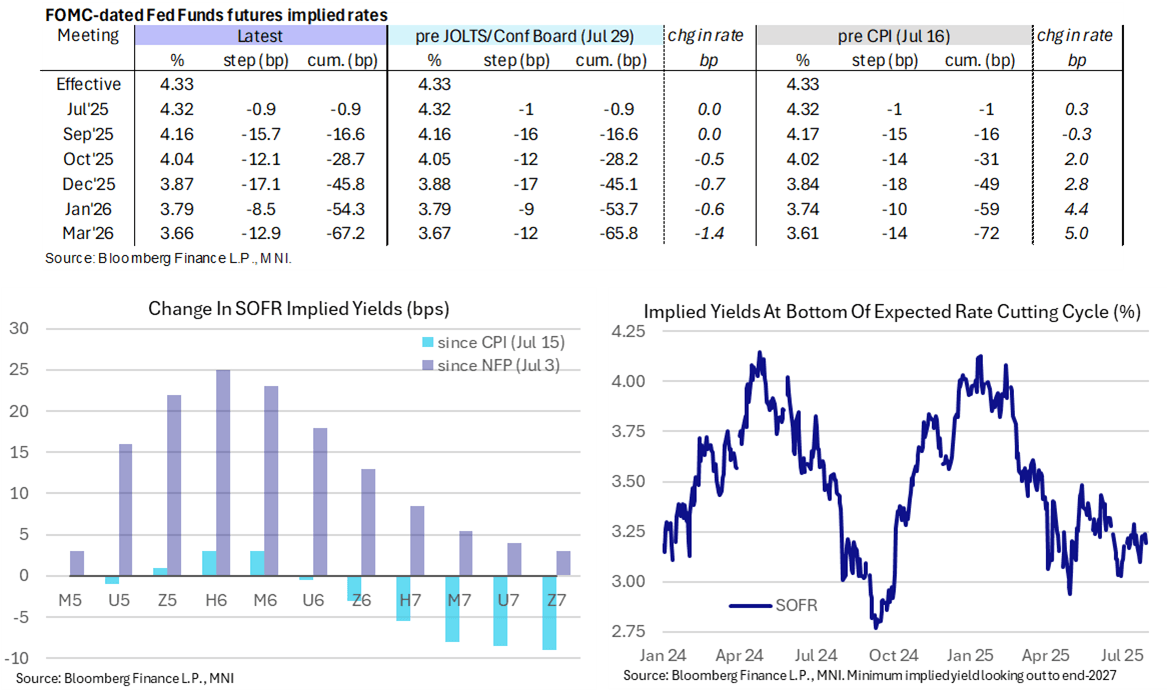

STIR: Soft JOLTS Report Mildly Adds To Day’s Dovish Shift Ahead Of FOMC Tomorrow

Jul-29 16:37

- Fed Funds implied rates continue to hold what was a marginally dovish reaction to a soft JOLTS report and mixed Conference Board consumer survey, which saw stronger than expected confidence but weaker labor differential).

- The Dec’25 implied rate is only 0.7bp lower post-1000ET data for -1.8bp on the day.

- Cumulative cuts from 4.33% effective: 1bp for tomorrow’s decision, 16.5bp Sep, 28.5bp Oct, 45.5bp Dec, 54.5bp Jan and 66.5bp Mar.

- The SOFR implied terminal yield of 3.195% (SFRH7) is 4.5bp lower on the day but only 1bp lower post the 1000ET data. It pushes it back towards the middle of the 3.1-3.3% range seen through July.

- Earlier in the day, trade and inventory data have left stronger GDP tracking for Q2 ahead of Thursday’s Q2 advance release (Atlanta Fed GDPNow revised up from 2.4% to 2.9%) but with soft domestic demand estimates (GDPNow sees PDFP closer to 0.7pp in Q2 after 1.6pps in Q1).

- MNI Fed Preview ahead of tomorrow’s decision: https://media.marketnews.com/Fed_Prev_Jul2025_With_Analysts_002622ac0e.pdf

OPTIONS: Expiries for Jul30 NY cut 1000ET (Source DTCC)

Jul-29 16:25

- EUR/USD: $1.1525(E765mln), $1.1550(E902mln), $1.1700-10(E1.1bln), $1.1800(E1.7bln)

- USD/JPY: Y147.50($878mln), Y148.25-30($989mln), Y148.65($945mln), Y149.00($853mln)

- AUD/USD: $0.6550(A$1.0bln), $0.6600-10(A$1.2bln)

- USD/CAD: C$1.3695-10($969mln), C$1.3770-75($1.7bln)