FED: US TSY 5Y NOTE AUCTION: HIGH YLD 3.710%; ALLOTMENT 41.92%

- US TSY 5Y NOTE AUCTION: HIGH YLD 3.710%; ALLOTMENT 41.92%

- US TSY 5Y NOTE AUCTION: DEALERS TAKE 11.94% OF COMPETITIVES

- US TSY 5Y NOTE AUCTION: DIRECTS TAKE 28.64% OF COMPETITIVES

- US TSY 5Y NOTE AUCTION: INDIRECTS TAKE 59.42% OF COMPETITIVES

- US TSY 5Y AUCTION: BID/CVR 2.34

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

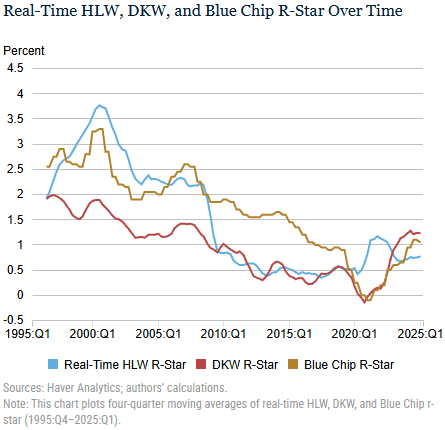

FED: Low R-Star Era Far From Over – NY Fed Staff

A Liberty Street Economics blog post from NY Fed staff including President John Williams (FOMC permanent voter) writes that “a reasonable estimate is that r-star has risen by a relatively modest 1/4 to 1/2 percentage point from its 2018 level. Thus, despite the recent rise in TIPS yields, the evidence suggests that the low r-star era is far from over.” This is “significantly smaller” than the 1.5pp increase in the longer-term TIPS yield over the same period. However, we add that this isn’t new rhetoric ahead of Williams’ appearance later today at 1915ET.

- “Some commentators claim that the prior decline in r‑star has reversed, pointing to the recent rise in future real interest rates implied by the bond market. But before declaring the death of this “low r‑star” era, a natural question to ask is: how reliable are market-based measures of r‑star?”

- They compare market-based measures of r-star with corresponding real-time estimates from the Holston, Laubach, and Williams (HLW) model.

- “In contrast to the real-time HLW measure of r-star, the TIPS-based measure has essentially no predictive power for real rates three years in the future. […] One plausible explanation for this poor forecasting performance is that TIPS yields do not necessarily correspond to market expectations of short-term interest rates, owing to liquidity and risk premiums embedded in these yields.”

- The report notes that their measures of r-star from the D’Amico, Kim and Wei (DKW) model plus one constructed from Blue Chip long-run forecasts have historically differed significantly but are “broadly similar” since the onset of the pandemic.

- Both have predictive power for future real interest rates but don’t improve findings relative to the HLW.

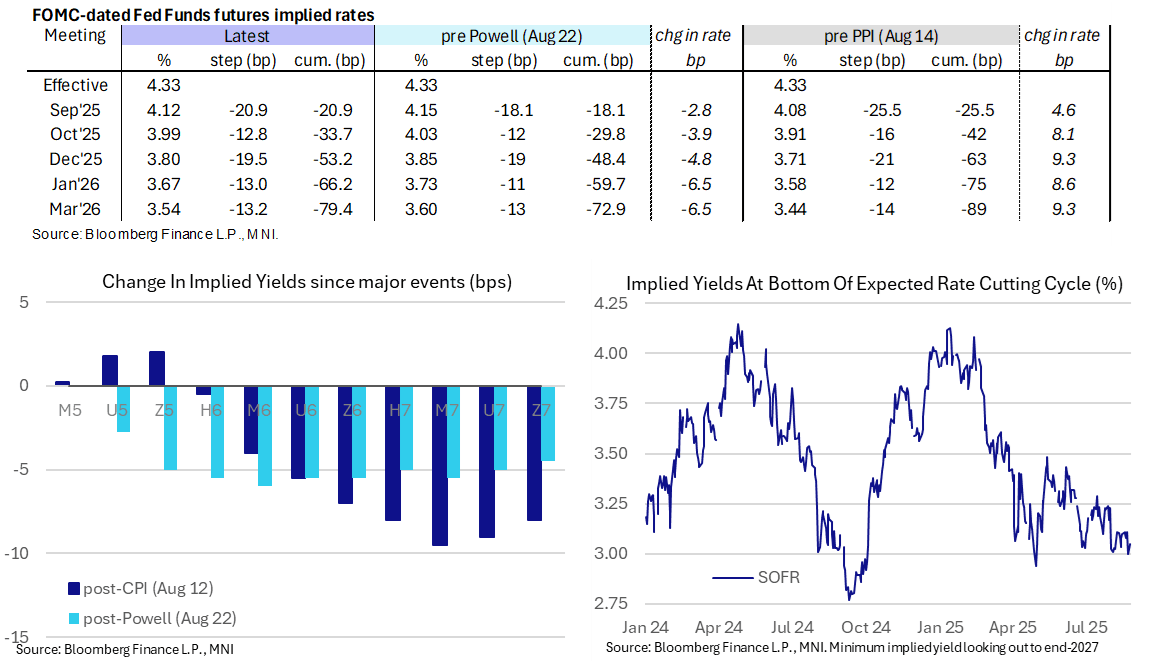

STIR: A Little More Than Two Cuts Priced To Year-End, Fedspeak Still Ahead

- Fed Funds implied rates for nearer-term meetings have seen little change since the NY crossover (after mostly modest increases overnight).

- The SOFR curve has however steepened amidst broader FI pressure to unwind a sizeable portion of Friday’s Powell-induced flattening on a Z5/Z6 basis.

- Cumulative cuts from 4.33% effective: 21bp Sep, 33.5bp Oct, 53bp Dec, 66bp Jan and 79.5bp Mar.

- The SOFR implied terminal yield of 3.05% (SFRH7) is 5bp higher on the day after Friday’s close of 3.00% was the lowest since late April.

- In doing so it falls back into a well-kept range seen since the Aug 1 payrolls report of 125bp +/-5bp of cuts from current levels, having closed yesterday with 133bp of cuts priced.

- Still to come, today’s Fedspeak could see some further ‘patient’ rhetoric, something generally seen last week prior to Powell, which could see some renewed focus on the “may” aspect of Powell’s remarks. That could be especially so with Logan but at the same time a relatively dovish tone from her would be more notable.

- 1515ET - Dallas Fed’s Logan (’26 voter, hawk) speaks at Banxico conference. This will be her first post-July FOMC comments having said on Jul 16 that she supports holding rates to keep cooling inflation and that the tariff impact won’t be clear until at least into the fall.

- 1915ET – NY Fed’s Williams (permanent voter) gives keynote remarks at Banxico conference. Speaking after the weak revisions of the Aug 1 payrolls report, he said Aug 2 that “modestly restrictive” policy is still needed and that the labor market is “still solid”. He sees economic growth rebounding in 2026.

US OUTLOOK/OPINION: GS See USD On Downward Descent

Writing after Fed Chair Powell’s Jackson Hole address, Goldman Sachs view the move up in the USD over the past week “as a short incline in an otherwise downward descent”, seeing “multiple paths to a weaker Dollar, some more benign than others.”

- “One of those benign paths is our baseline scenario, where we expect successive Fed cuts to keep elevated recession risk at bay but nevertheless erode the attractiveness of the US front-end in a stall speed economy.”

- They now expect incoming data to shape the market debate shifting to a 25bp vs 50bp cut next month.

- “If the downward revisions to job growth in the last payrolls report—typical around cycle turning points—portend a more significant slowing in the labour market, policy may need to adjust more rapidly as well, putting even more pressure on the Dollar.”

- “But it is also possible that firmer tariff-induced inflation is seen as a policy constraint that pressures equity risk, causing Dollar weakness to be more narrowly concentrated against ‘safer’ currencies like JPY, EUR, and CHF.”

- Dollar shorts should also provide exposure to concerns about the Fed’s independence.