FED: US TSY 29Y-11M BOND AUCTION: HIGH YLD 4.651%; ALLOT 44.54%

Sep-11 17:02

- US TSY 29Y-11M BOND AUCTION: HIGH YLD 4.651%; ALLOT 44.54%

- US TSY 29Y-11M BOND AUCTION: DEALERS TAKE 9.96% OF COMPETITIVES

- US TSY 29Y-11M BOND AUCTION: DIRECTS TAKE 28.01% OF COMPETITIVES

- US TSY 29Y-11M BOND AUCTION: INDIRECTS TAKE 62.03% OF COMPETITIVES

- US TSY 29Y-11M BOND AUCTION: BID/COV 2.38

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: White House Press Conference Underway Shortly

Aug-12 17:02

White House Press Secretary Karoline Leavitt is shortly due to deliver her first press conference since July 31. LIVESTREAM In around an hour, State Department spokesperson Tammy Bruce will brief reporters at State. LIVESTREAM

- The White House presser is likely to be dominated by President Donald Trump's announcement yesterday that the federal government would assume temporary control of the Washington, DC police force and deploy 800 National Guard troops to tackle crime in the US capital. The federal takeover is expected to last 30 days and comes after Trump deployed 4,700 National Guard members and Marines to Los Angeles to quell protests related to White House immigration policies.

- The White House confirmed this morning that South Korean President Lee Jae Myung will meet Trump at the White House on August 25 for a first meeting between the pair since Lee took office in June. Lee’s three-day trip takes place less than a month after Seoul struck a trade framework with the US to avoid a 25% across-the-board tariff.

BONDS: EGBs-GILTS CASH CLOSE: Bear Steepening, With Gilts Underperforming

Aug-12 17:01

European curves bear steepened Tuesday.

- US CPI data in early afternoon was the session's global focus, and initially brought a positive reaction in core FI as it appeared to allay fears of upside pressure on goods prices from inflation.

- However the move swiftly reversed, with Bunds leading a global selloff. There was no identifiable trigger for the long-end German sell-off, which saw 30Y yields hit the highest since 2011 amid heavy volumes in futures. 10Y German yields stopped just shy of the July high of 2.769% (hitting 2.758%).

- There was some extension of the selloff in sympathy with long-end Treasuries as President Trump said on social media that he was considering allowing a "major lawsuit" against Fed Chair Powell to proceed.

- That said, Gilts underperformed Bunds on the day. The August UK labour market release was on balance stronger-than-expected, bringing a mildly hawkish market reaction, though private sector regular pay data remains consistent with slowing wage growth. Our review of the data is here.

- Both the German and UK curves bear steepened, with periphery/semi-core EGB spreads closing mixed.

- Wednesday's calendar is lighter, with final Spanish and German CPI readings on offer.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.967%, 5-Yr is up 2.9bps at 2.318%, 10-Yr is up 4.8bps at 2.744%, and 30-Yr is up 7.3bps at 3.299%.

- UK: The 2-Yr yield is up 2.2bps at 3.885%, 5-Yr is up 3.9bps at 4.04%, 10-Yr is up 6.1bps at 4.626%, and 30-Yr is up 7.5bps at 5.467%.

- Italian BTP spread down 0.1bps at 78.8bps / French OAT up 0.5bps at 66.8bps

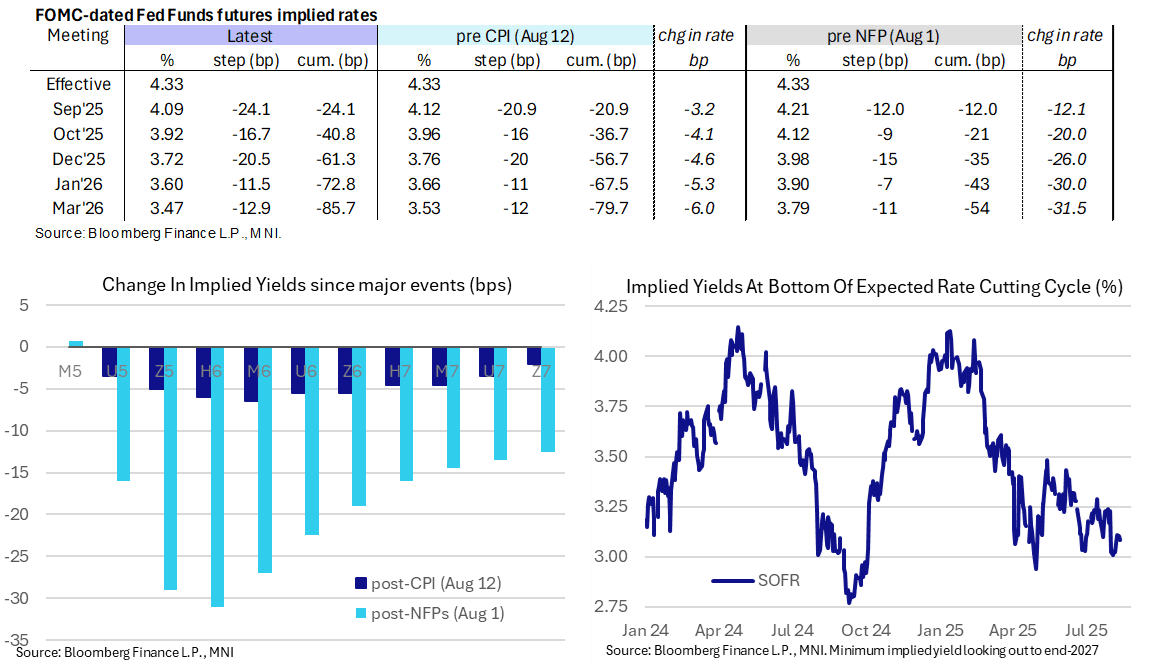

STIR: Holding The Shoring Up Of A 25bp September Fed Cut

Aug-12 17:00

- Fed Funds implied rates saw little reaction to post-CPI Fedspeak earlier, when Barkin (non-voter) said the balance between dual mandate variables still unclear whilst Schmid (’25 voter) sounded like he would dissent to a September cut.

- Fed Gov Nominee Miran meanwhile said there’s just no evidence of tariff inflation whilst he sees service disinflation as imminent.

- More broadly today, implied rates pared some of the snap reaction to the CPI release but are holding the net push lower on the dovish core goods and headline CPI details, albeit keeping within ranges seen since the July payrolls report on Aug 1 having seen a mild hawkish drift ahead of today’s CPI report.

- Cumulative cuts from 4.33% effective: 24bp Sept (vs 21bp pre-CPI), 41bp Oct, 61.5bp Dec (vs 56.5bp), 73bp Jan and 85.5bp Mar (vs 79.5bp).

- SOFR implied terminal yield pricing is 4.5bp lower post-release for -2bp on the day at 3.085% (SFRH7), chipping away at modest increases pre-data. It firms up pricing of five cuts from current levels.