OIL: *US SANCTIONS IRAN’S SHAMKHANI OIL-TRADING NETWORK

*US SANCTIONS IRAN’S SHAMKHANI OIL-TRADING NETWORK *NEW IRAN RESTRICTIONS MOST SWEEPING SINCE 2018, US SAYS - bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Lat SOFR/Treasury Option Roundup: SFOR Vol Spread, 10Y Calls

SOFR & Treasury option trade looked mixed on net, some chunky flows traded sporadically: Large Mar'26 SOFR Straddle buy vs. calls, while Treasury options say a pick-up in Sep & Aug 10Y call buying in the second half. Projected rate cut pricing gains slightly vs. late Friday (*) levels: Jul'25 at -5.3bp (-4.8bp), Sep'25 at -28.6bp (-28.2bp), Oct'25 steady at -46.3bp, Dec'25 at -66.8bp (-66.2bp).

- SOFR Options:

- -4,000 0QZ52QZ5 96.00 put spd, 2.0 net flattener

- +2,000 0QQ5 96.62/2QQ5 96.50/3QQ5 96.12 put fly, 1.5 net db

- +45,000 SFRH6 96.12 straddles vs. 97.00 calls, 28.5-29.0 vs. 97.00/0.20%

- +5,000 SFRN5 95.75/95.81 put spds, 0.25

- +2,000 SFRU5 95.75/95.81/95.87 put flys, .25 ref 95.985

- +4,000 2QZ5 96.25 puts, 9.0 vs. 96.785/0.20%

- Block/screen, 4,000 SFRU6 97.00/97.75 2x1 put spds, 4.0 net ref 96.91 to -.92

- -1,500 0QQ5 97.50 calls, 3.0 ref 96.92

- 2,000 SFRN5 95.87 puts

- -3,000 SFRU5 96.12/96.25 1x2 call spds, 5.5

- Treasury Options:

- +30,000 TYU5 112 calls, 1-04 ref 112-03

- 12,500 TYQ5 113 calls, 21 ref 112-02.5

- 3,500 TYQ5 110.75/111.25 put spds

- 10,000 TYU5 108/110 put spds ref 111-29

- -2,000 FVQ5 107.75 puts, 5

- over +11,300 FVQ5 108 puts, 7.5-8

- 6,000 TYQ5 110 puts

- +1,500 TYU5 109.5/111 put spds, 24 ref 111-31.5 vs. 111-29/0.10%

- +2,000 wk1 TY 111.25 puts, 6 vs. 111-28.5/0.10%

- +1,100 USQ5 116/119 2x3 call spds, 105 ref 114-30/0.36%

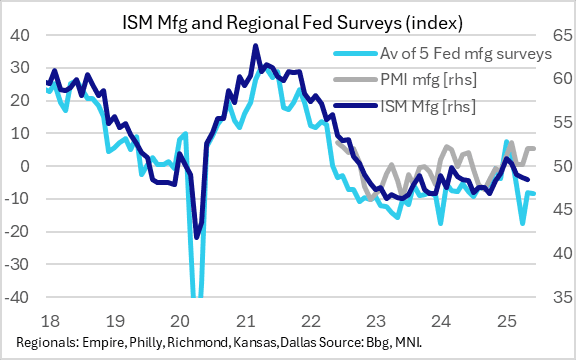

US OUTLOOK/OPINION: ISM Manufacturing Set To Come In Slightly Higher (1/2)

After surprising to the downside last month, the ISM Manufacturing index (Tuesday 1000ET) is expected to show a slight pickup in June vs May but remain in contractionary territory for a 4th straight month, edging up to 48.8 (analyst range of 47.0 to 50.2) from 48.5. This would be the first rise after 4th consecutive declines. New orders are seen 0.5 points higher at 48.1, with employment (closely-watched ahead of Thursday's June nonfarm payrolls) 0.3 points higher at 47.1.

- The broad consensus appears consistent with mixed regional Fed manufacturing survey composite indices for the month. The average z-score (5-year lookback) was -0.7 for the major 5 surveys, the same as in May, suggesting no improvement or deterioration.

- New York’s deteriorated, Philadelphia’s was steady, but Dallas, Richmond and Kansas City (as well as Chicago's regional manufacturing activity) improved modestly. All were still in weak territory as trade policy uncertainty lingers, though we wonder whether the Empire State underperformance was due to the survey period earlier in the month, given that the regional readings appeared to improve as the month went on.

- In other indicators, MNI's Chicago Business Barometer translated into national ISM weights eased 3.5 points to 43.1 in June, the lowest level of 2025, though the index did see a rise in New Orders; the flash S&P Global PMI was steady in June at 52.0 though this has has a positive gap with the ISM for 12 consecutive months.

EURJPY TECHS: Support Remains Intact

- RES 4: 171.09 High Jul 23 ‘24

- RES 3: 170.47 76.4% Fibonacci retracement for Jul - Aug ‘24 downleg

- RES 2: 169.91 1.236 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 169.81 High Jun 27

- PRICE: 169.64 @ 17:03 BST Jun 30

- SUP 1: 167.92 Low Jun 24

- SUP 2: 166.94 20-day EMA

- SUP 3: 165.91 Low Jun 16

- SUP 4: 164.95 50-day EMA

The trend set-up in EURJPY is unchanged, it remains bullish. Recent gains have resulted in a break of 166.69, the Oct 31 ‘24 high. Scope is seen for a climb towards 170.47, a key Fibonacci retracement point. Note that the uptrend is in overbought territory, a pullback would unwind this condition. Support to watch lies at 166.94, the 20-day EMA. Clearance of this EMA would suggest potential for a deeper retracement.