US-RUSSIA: US 'Prepared To Implement Additional Measures' If No Peace By 8 Aug

Reuters reports comments from the acting US Representative to the United Nations, Dorothy Shea, saying to the UN Security Council that President Donald Trump "has made clear a deal to end Russia's war in Ukraine must be done by August 8th". Adds that the US "is prepared to implement additional measures to secure peace in Ukraine."

- While neither of these comments is technically 'new', Shea does outline that the 8 August deadline refers to 'a deal to end the war', rather than Russia simply agreeing to new talks or another 'lesser' commitment.

- It remains to be seen what the 'additional measures' might refer to and who they may be imposed on.

- On 30 July, Kremlin spox Dmitry Peskov claimed that Russia has developed an 'immunity' to US sanctions, while Foreign Ministry spox Maria Zakharova said the threat of new sanctions was 'routine'.

- Focus will be on whether the US engages in significant secondary sanctions/tariffs against those trading with Russia, notably China and India, regarding substantial hydrocarbon purchases.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

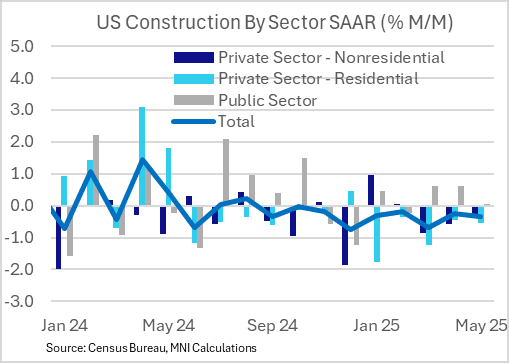

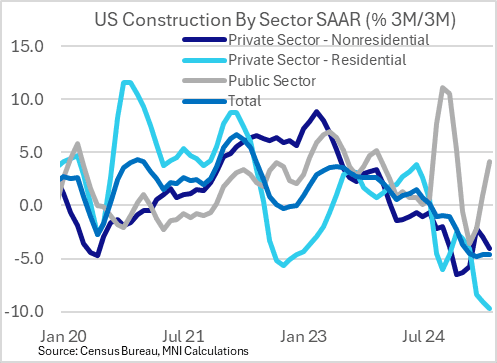

US DATA: Construction Values Continue To Contract With Residential Activity Weak

May's Construction Spending report showed a 7th consecutive monthly drop in value terms, of -0.3% (-0.2% prior rev up from -0.4%), basically in line with -0.2% consensus. This was another weak report that showed broad based weakness across private sector construction, with negative momentum building.

- Overall construction value is now down 3.5% from the May 2024 peak of $2.215T (SAAR) and is contracting at a 4.7% 3M/3M (ie quarterly) annualized rate. While this series is in nominal terms, it's notable that 3M/3M changes are as weak as they have been in the last 25 years.

- That's true across sectors: total private sector construction value fell 0.5% M/M (hasn't posted a positive month since May 2024), led by another weak reading for residential construction (which is half of private sector construction - falling 0.5% M/M).

- Residential construction is now falling at a 9.7% 3M/3M annualized pace, the most since July 2009 amid the US housing crash.

- Two notes on the more positive side from a growth perspective: Manufacturing construction's decline slowed (-0.1%, "best" in 5 months) and is now shrinking at a 3.6% 3M/3M rate, the least bad since November 2024, leaving the door open to a 2nd half recovery. And public sector (one-quarter of overall construction) momentum is roundly picking up, rising 0.1% M/M for the 3rd consecutive sequential gain, and now increasing at a 4.1% 3M/3M pace, fastest in 5 months.

- This report merely confirms that residential investment is contracting and is likely to subtract from GDP this year, with nonresidential structures investment continuing to look weak as well.

FRANCE: Gov't Censure Motion Vote Set To Start 17:30CET, Result ~20:30CET

Members of the National Assembly are due to vote on a censure motion against the gov't of PM Francois Bayrou at around 17:30CET (11:30ET, 16:30BST) with a result expected at around 20:30CET (14:30ET, 19:30BST) reports Europe1. There is little-to-no jeopardy in the vote for the incumbent, with the parties of the left-wing New Popular Front (NFP) the only ones likely to back the motion. The far-right Rassemblement National (National Rally, RN) has already confirmed it does not intend to back the motion, ensuring its failure.

- Earlier today, the leader of the RN in the National Assembly, Marine Le Pen, said to reporters that "we [would] vote for a motion of censure when we want to protect the French from toxic measures that could be taken. Censuring today would bring nothing to the French. We will be attentive to the fate of the multi-year energy programming and the budget that will be presented by François Bayrou's government."

- With the National Assembly set to go on its summer recess from mid-July until September, the Bayrou gov't is likely safe until the 2026 budget process gets underway.

- Alternatively, from 7 July (one year after the last election) President Emmanuel Macron could look to dissolve the National Assembly and hold a snap election. This would be an even riskier move than in 2024, with his centrist alliance polling poorly and at risk of further seat losses.

GILTS: Away From Highs On U.S. Cues

Gilts trade away from highs given cues from Tsys, although the move in U.S. paper is far more aggressive as U.S. data drives matters. Global cues have dominated for much of the day.

- Futures pierced next resistance (93.68) before, topping out at 93.76, before a retrace to ~93.50.

- Next resistance of note located at 94.00, with the bullish technical theme intact.

- Yields 1.0-7.5bp lower, curve flattens on the day.

- 2s10s remains above 60bp, while 5s30s is comfortably above 125bp.

- Year-to-date highs on both curves remain some distance away.

- While fundamentals and fiscal fragility point to further steepening, already elevated steepener positioning and a more activist official approach to cutting the WAM of issuance present risks to this idea.

- Foreign investors were sellers of gilts in May (for the fourth month in five, as detailed in an earlier bullet), with local participants (both private and financial institutions) filling the gap.

- Comments from dovish BoE dissenter Taylor and 4.375% Mar-28 gilt supply are due Wednesday.