RENEWABLES: UK Morning Wind Forecast

Oct-01 07:28

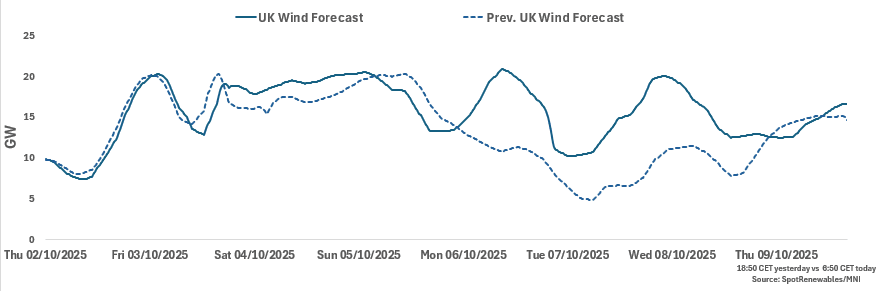

See the latest UK renewables forecast for base-load hours for the next seven days. UK wind output is anticipated to be relatively high over 2-9 October to be between 40-67% load factors.

UK: Wind for 2-9 October

- 2 October: 11.45GW

- 3 October: 17.12GW

- 4 October: 19.17GW

- 5 October: 17.28GW

- 6 October: 17.50GW

- 7 October: 12.97GW

- 8 October: 16.23GW

9 October: 14.04GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SPAIN DATA: Manufacturing PMI Outperforms In August

Sep-01 07:27

- Spanish August manufacturing PMI firmer than expected at 54.3 (52.1 consensus, 51.9 July) in a very strong report. Key highlights: "Fastest growth of the manufacturing sector since last October [...] output, new orders and employment all rose to stronger degrees compared to July. Expectations were positive that growth will be sustained, although buying activity increased only slightly amid ongoing supply-side challenges"

- "Positive projections for growth also helped to support recruitment activity, with firms typically predicting a rise in output from

present levels in 12 months’ time. Confidence overall improved since July to a six-month high and was notably above the

survey’s long-term trend." - On prices: "Another modest increase in input prices was registered during August. Firms reported that inflation reflected

higher prices for foodstuffs and metals. Increased costs were passed on by manufacturers to clients wherever possible via a

rise in output charges. The rate of inflation was also modest despite rising to the highest level in five months."

STIR: EUR Short End Still Leans Towards One Further Cut

Sep-01 07:24

Weakness further out the curve has promoted modest hawkish repricing in the front end of the EUR rates space (early focus this week falls on incoming EUR supply and political risk in France).

- Euribor futures are flat to -3.5, steepening. August lows are untested across the strip

- ECB-dated OIS shows little changed to 1bp less dovish but still leans towards 1 further cut in the cycle, pricing ~17bp of easing through June.

- ECB President Lagarde has reaffirmed the Bank’s ongoing monitoring of EGB spreads, along with the need for fiscal discipline and stressing that the toppling of any Eurozone government presents worry for the Bank. She also stressed that the Bank’s inflation target has been met, while pushing the need for swifter European reforms and highlighting a reduction in economic uncertainty.

- Elsewhere, acting Slovenian central bank Governor Dolenc suggested that the ECB is probably done with rate cuts in the current cycle.

- Meanwhile, Governing Council member Rehn said there is "no room for complacency", while tipping his hat to downside risks to inflation.

- Manufacturing PMI data headlines the Eurozone calendar today. While they are final readings for the larger economies (and Eurozone on the whole), it is worth noting that Spain’s reading was firmer than expected.

- Note that ECB’s Schnabel & Cipollone with chair panels at the ECB legal conference today, with Lagarde set to speak at that event this evening.

ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

Sep-25 | 1.922 | +0.2 |

Oct-25 | 1.900 | -2.0 |

Dec-25 | 1.839 | -8.1 |

Feb-26 | 1.815 | -10.6 |

Mar-26 | 1.770 | -15.0 |

Apr-26 | 1.758 | -16.2 |

Jun-26 | 1.748 | -17.2 |

MNI: SPAIN AUG MANUF PMI 54.3 (52.1 FCAST, 51.9 JUL)

Sep-01 07:15

- MNI: SPAIN AUG MANUF PMI 54.3 (52.1 FCAST, 51.9 JUL)