UK DATA: UK GfK Highest Since Nov-21

Jun-20 23:01

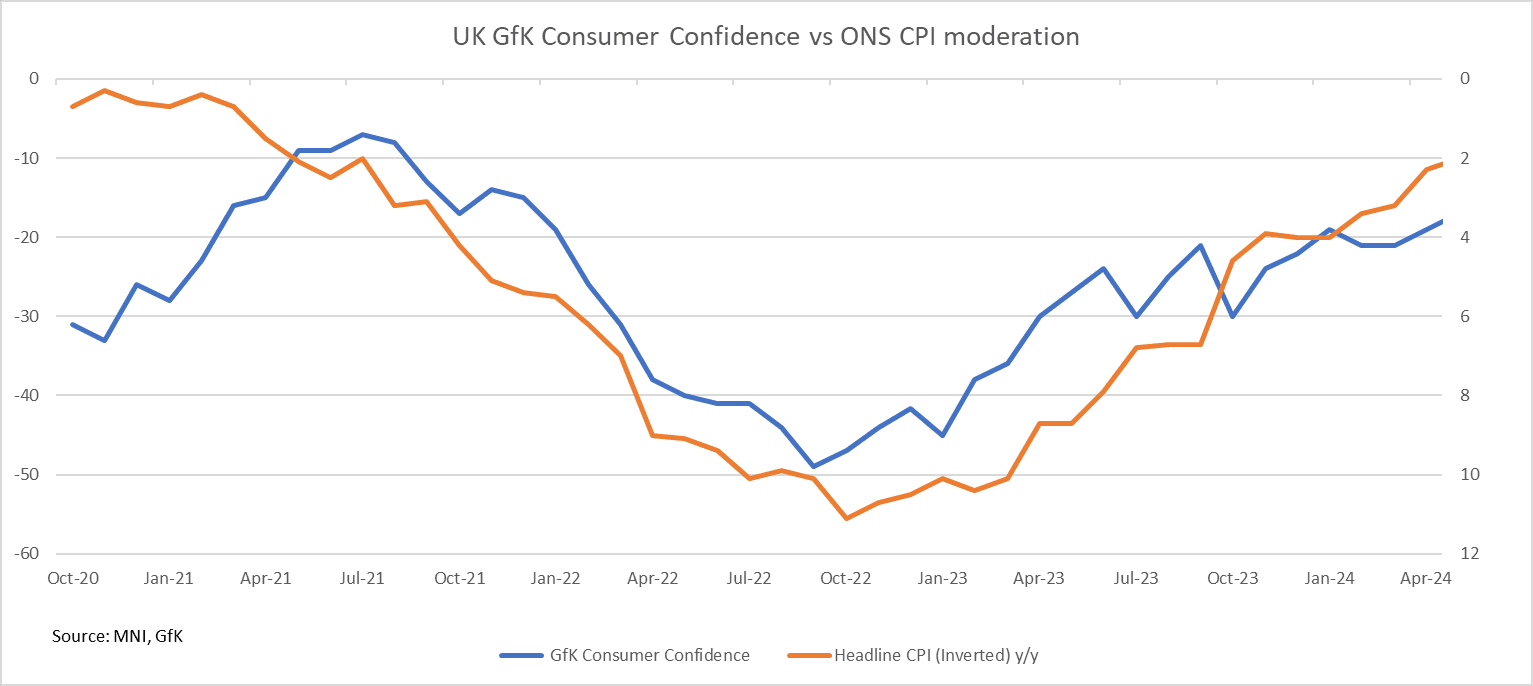

UK GfK Consumer Confidence rose for the third consecutive month slightly more than expected by 3 points to -14 (vs -16.0 consensus, -17 prior) in June - the highest level seen since November 2021.

- 3 of 5 subcomponents improved, although all are above levels seen in June 2023. In particular, 'General Economic Situation over next 12 months' improved by 6 points to -11 and 'Major Purchase Index' rose 3 points to -23.

- Meanwhile, 'Personal Financial Situation over next 12 months' fell 3 points to 4.

- The chart below shows, that although the progress is slowing, as inflation continues to soften consumer confidence continues to rise.

- June's survey was conducted among a sample of 2,011 individuals from May 31st to June 14th.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK FEB-APR MEDIAN PAY AWARDS +4.9% :Brightmine

May-21 23:01

- MNI: UK FEB-APR MEDIAN PAY AWARDS +4.9% :Brightmine

UK DATA: Brightmine: Pay Deals Rises to 4.9%; But Below Median Rate Over Last Year

May-21 23:01

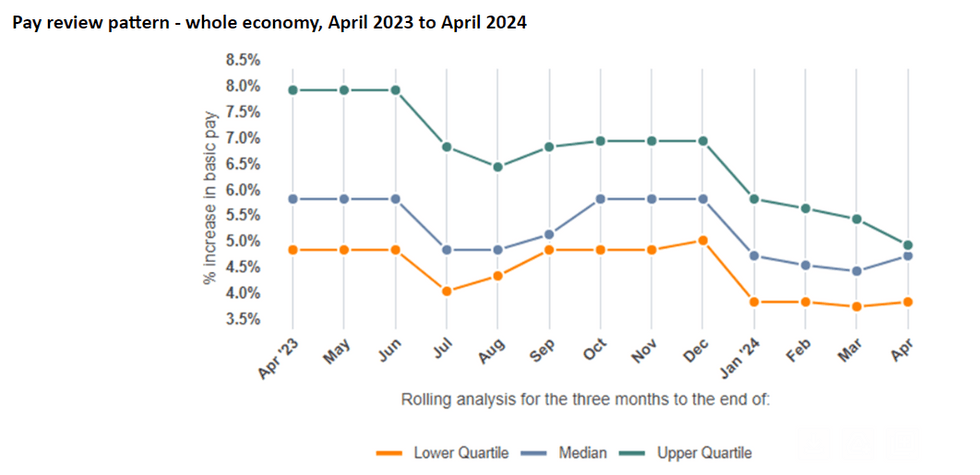

- Brightmine (previously XpertHR) median basic pay awards in the 3 months to the end of April 2024 edged up slightly to +4.9% (vs a revised +4.6% in the prior rolling quarter - originally +4.8% Y/Y 3 month average),

- In terms of pay review pattern, Brightmine found the interquartile range has narrowed falling between 4% and 5.1% - the narrowest since 2021. This data points to the continuation in the reduction in wage growth relative to last year, although not as meaningful a slowdown as the MPC would like. Note that last week's official ONS private sector regular wages number came in line with consensus and 0.1pp below the BOE's forecast, although the MPC has emphasised greater focus on CPI data due later today, specifically Services CPI. (See the MNI UK CPI Preview here).

- Data were collected between 1 February and 30 April 2024, based on a total of 102 pay settlements, representing 355,064 employees.

OIL: Crude Focus On Fundamentals, US Stock Build Reported

May-21 22:56

Oil sold off on demand concerns and signs that the market is easing but prices remained in recent ranges. The Brent prompt spread has narrowed to only 10c signalling supply outweighing demand, according to Bloomberg. The greenback strengthened briefly following Fed Waller’s comments. The USD index is up 0.1%.

- WTI fell 1.4% to $78.22 and has started today’s trading around this level. It fell to a low of $77.65/bbl before recovering. The benchmark is now down 3.8% in May. Short-term gains are seen as corrective and holding below the 50-day EMA signals the potential for a deeper correction. Initial support is at $76.36, May 15 low, while resistance is at $80.90, May 1 high.

- Brent is also down 1.4% at $82.53/bbl to be 4.4% lower this month. It made an intraday low of $82.04 finding support at $82. Conditions remain bearish with initial support at $81.05, May 15 low. The bull trigger is at $91.18, April 12 high.

- Prices took another step down on reports that US crude stocks rose last week. Bloomberg reported that oil rose 2.5mn barrels and gasoline 2.1mn but there was a distillate drawdown of 300k, according to people familiar with the API data. The official EIA numbers are released later today.

- The US government will sell 1mn barrels of its gasoline reserve to bring down costs for the summer driving season. But commentators don’t believe it will make a material difference as demand far exceeds that each day.