AUSSIE 10-YEAR TECHS: (U5) Recovers With Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 14:34 BST Aug 8

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed a poor NFP print. This keeps Aussie 10-year futures toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Rolling Off Highs

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.660 @ 16:08 BST Jul 09

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures traded under pressure for much of last week, keeping prices pressured and within range of the recent pullback lows. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

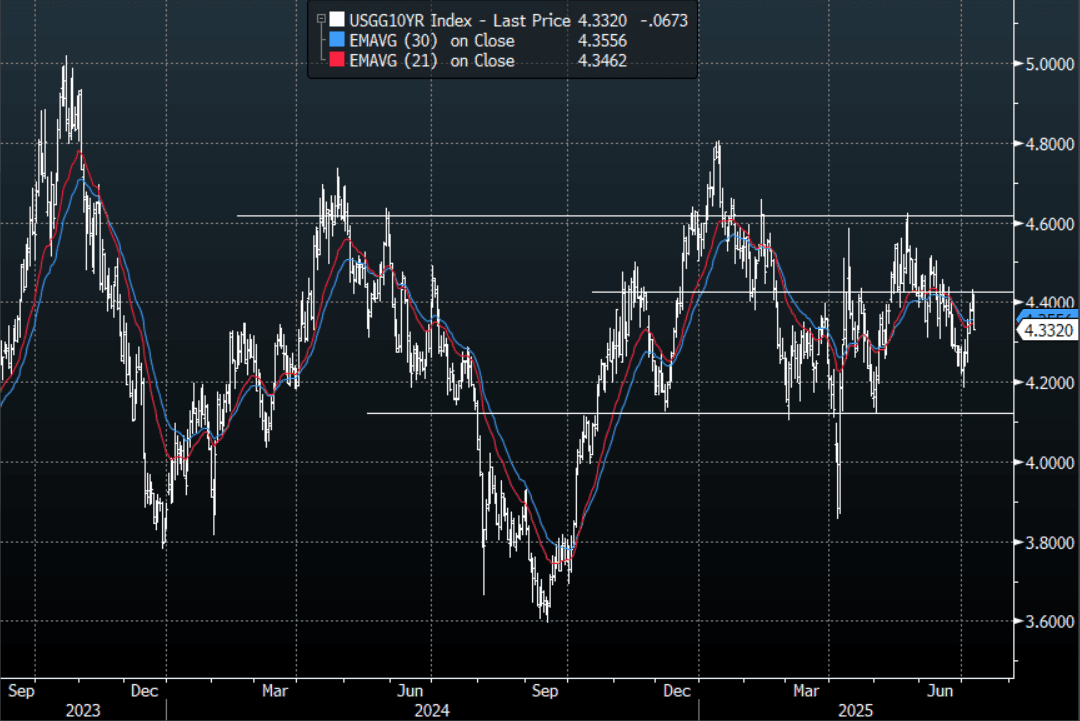

US TSYS: Yields Lower Led By Long-End

TYU5 reopens at 111-10, up 0-01+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.3320% - 4.4191%, closing around 4.33%.

- Treasury yields gave back a lot of their recent gains; this was led by the long-end which saw the yield curve flatten (2s10s -2.17 at 48.284, 5s30s +0.87 at 96.048).

- “The emerging divide among Federal Reserve officials over the outlook for interest rates is being driven largely by differing expectations for how tariffs might affect inflation, a record of policymakers’ most recent meeting showed.” - BBG

- MNI FED: Minutes Clearly Signal A July Hold, While Keeping Future Options Open. The June meeting minutes captured a Committee that was leaning in a slightly more hawkish direction than earlier in the year, though probably no more than should have been expected. The Dot Plot released at the meeting already captured most of the story: a divided Committee retains its overall easing bias but needs varying degrees of certainty before supporting a resumption of the easing cycle.

- The 10-year yield has topped out just above the 4.40% area, giving the bulls some reprieve. No clear direction though has seen the 10-year chop around in a wider 4.10% - 4.60% range with the 4.40% area being the pivot. A sustained close back above the 4.45% area could see more of the longs pared back but while this area holds they would be happy to stick with their position looking for a move back to the lower end of the range.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CNH: USD/CNH Hold Above 7.1800, Implied Vol Continues To Fall

USD/CNH is holding around 7.1825 in early Thursday dealings. The pair was little changed for Wednesday's session. Broader USD sentiment was also little changed, with the BBDXY index finishing steady, consolidating above recent lows. USD/JPY saw a modest pullback. Spot USD/CNY finished up just above 7.1800, while the CNY CFETS basket tracker edged a little higher to 95.59 (per BBG).

- For spot USD/CNH, upside focus will remain on the 50-day EMA (near 7.1970). The pair couldn't breach 7.1900 in Wednesday trade, but dips remained fairly shallow. Recent lows rest just under 7.1700.

- Implied volatility remains very low for USD/CNH, the 1 month last close to 3.30%, near lows back to July last year.

- Broader focus remains on US tariff/trade letter announcements. A number of countries received notifications on Wednesday US time, with Brazil, threatened with a 50% tariff rate, the most notable announcement (the initial reciprocal tariff announcement was 10%). BRL weakened sharply, but broader spillover to EM Asia FX isn't evident so far.

- This follows Trump's recent threats on further tariffs if BRICs aligned countries adopt anti-American policies, although the Brazil announcement is also reflective of how firmer leader Bolsonaro was treated (per Trump's Truth Social post).

- On the local data front, we await the June new loans/aggregate finance data due between now and the 15th of July). Next Monday delivers June trade data.