BUND TECHS: (U5) Bear Threat Remains Present

- RES 4: 130.26 High Aug 8

- RES 3: 130.06 High Aug 14

- RES 2: 129.69/90 50-day EMA / High Aug 28

- RES 1: 129.42 Intraday high

- PRICE: 129.33 @ 05:36 BST Sep 4

- SUP 1: 128.64 Low Aug 15 and the bear trigger

- SUP 2: 128.40 Low Apr 9

- SUP 3: 128.19 Low Mar 27 (cont)

- SUP 4: 127.83 76.4% retracement of the Mar 11 - Apr 7 bull leg (cont)

Bund futures have traded lower this week. The latest move down undermines a recent bullish theme and attention is on support at 128.64, the Aug 15 low and a bear trigger. A break of this level would confirm a resumption of the downtrend and highlight a range breakout - the contract has traded in a range since April. This would open 128.40 next, the Apr 9 low. Key short-term resistance is at 129.90, the Aug 28 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Richer Despite Poor 10Y Auction

JGB futures are holding stronger, +26 compared to settlement levels, despite today’s poor 10-year auction.

- (MNI) A few Bank of Japan board members said they would consider resuming interest rate hikes if trade tensions were expected to ease without further escalation, according to minutes of the June 16-17 meeting released on Tuesday. However, the minutes offered no indication on the timing or pace of future rate increases.

- Bloomberg - "MUFG CEO Hironori Kamezawa called on the BOJ to raise its policy rate as early as the next meeting to combat strong inflation."

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally.

- Cash JGBs are 1-4bps richer across benchmarks, led by the 10-year. The benchmark 10-year yield is 4.1bps lower at 1.475% after today's supply.

- The 10-year JGB auction delivered weak results, with the low price failing to meet expectations at 100.21, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.0592x from 3.5070x, and the tail lengthened to 0.14 from 0.03.

- Swap rates are flat to slightly lower. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Cash Earnings data.

FOREX: Asia FX Wrap - BBDXY Finds Demand Sub 1210

The BBDXY has had a range of 1208.49 - 1211.50 in the Asia-Pac session, it is currently trading around 1211, +0.04%. The USD, with a huge rejection of the 1220/1230 area on Friday, had a knee-jerk reaction lower to the outsized move in US rates as the market's view on growth and interest rate cuts is re-evaluated. The USD is consolidating just above its 1205 support, with very little reaction to either rates extending lower or Equities bouncing strongly.

- EUR/USD - Asian range 1.1554 - 1.1588, Asia is currently trading 1.1560. The pair has bounced nicely off the important 1.1300/1.1400 area. The market is consolidating just ahead of its first resistance towards 1.1650/1.1700.

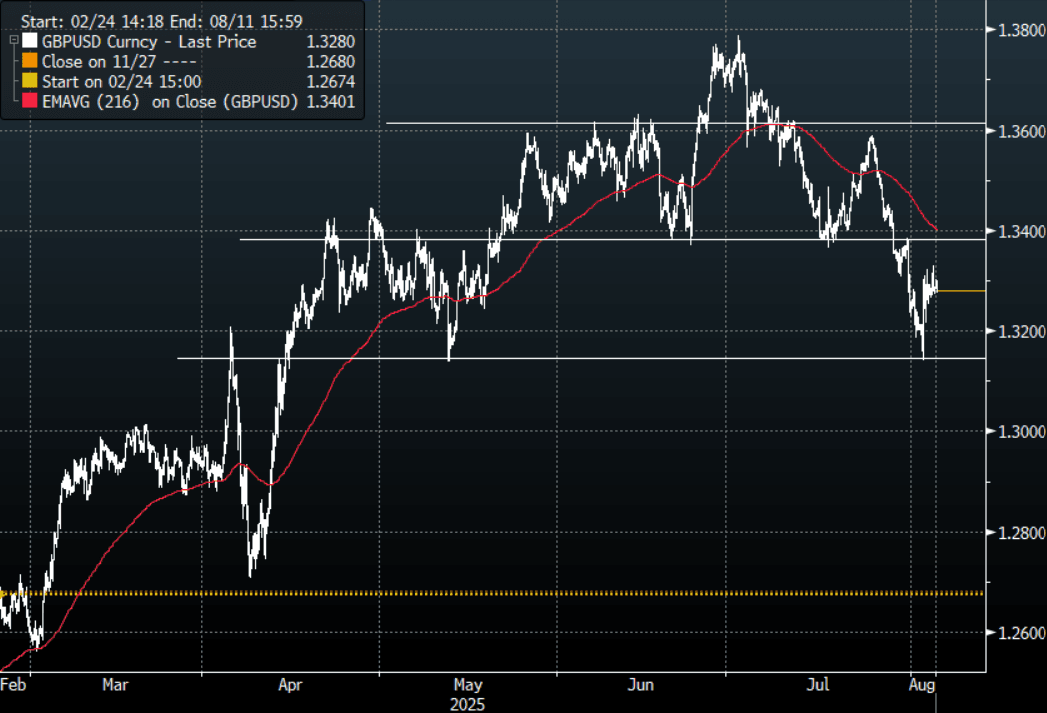

- GBP/USD - Asian range 1.3278 - 1.3303, Asia is currently dealing around 1.3280. This pair bounced nicely off the 1.3100/1.3200 support area. I would suspect sellers would be around on a bounce back towards 1.3400 initially.

- USD/CNH - Asian range 7.1774 - 7.1843, the USD/CNY fix printed 7.1366, Asia is currently dealing around 7.1830. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3372, US 10-Year 4.20%, BBDXY 1211, Crude Oil $66.16

- Data/Events : France Industrial/Manufacturing Production/HCOB PMI’s, Spain Homes Sales/Industrial Production/HCOM PMI’s, Italy HCOM PMI’s, Germany HCOB PMI’s, EZ HCOM PMI’s/PPI

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Richer But Off Bests, Mar-36 Supply Tomorrow

ACGBs (YM flat & XM +4.0) are holding richer but well off session bests.

- June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today's US calendar will be the US ISM services index for July.

- Cash ACGBs are 11bps richer after being closed for a bank holiday yesterday, with the AU-US 10-year yield differential at +1bp.

- The bills strip is richer, with pricing flat to +1.

- RBA-dated OIS pricing is giving a 25bp rate cut in August a 100% probability, with a cumulative 65bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$900mn of the 4.25% 21 March 2036 bond. A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.