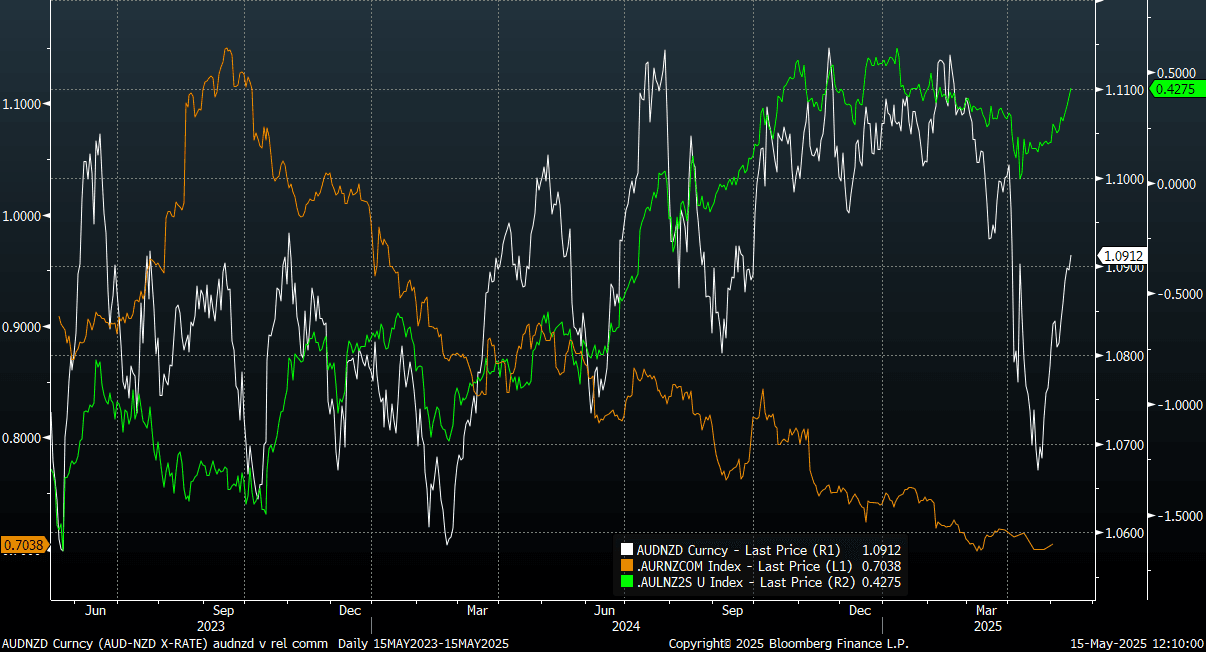

AUDNZD: Trying To Consolidate Above 1.0900, AU-NZ 2yr Spread Supportive

The AUD/NZD cross is just off multi week highs, last near 1.0910/15 (session highs rest at 1.0922). The pair is trying to consolidate a break above the 1.0900 handle, post the stronger Australian jobs data earlier. Earlier April highs we near 1.1000, then above 1.1030.

- The chart below plots the AUD/NZD cross (white line) against the AU-NZ 2yr swap spread, (the green line). This spread is now back to +43bps, fresh multi month highs. This is implying higher levels in the AUD/NZD cross, and maintains a firm directional correlation with the cross. Better data outcomes have helped in Australia, while lower US-China trade tensions have also been a factor.

- The other line in the chart, the orange one, is relative commodity prices, proxied by series from DB and CBA. NZ commodity prices have been outperforming in recent months, amidst higher dairy prices. This may be containing AUD/NZD upside to a degree, although relative trade/current account positions are still in AUD's favor.

- Rate differentials are still likely to be the most important driver for the cross. Next Tuesday we get the RBA decision, with rate cut odds easing, but still close to 100% priced for a 25bps cut.

- In NZ, tomorrow we get inflation expectations, then PPI next week as well as trade data.

Fig 1: AUD/NZD Versus AU-NZ 2yr Spread & Relative Commodity Prices

Source: DB/CBA/ MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Market Remains Calm in Storm.

- As equity markets whipsaw around globally and domestically, the one thing that is evident is the calmness of the Chinese bond market.

- Authorities have managed successfully an issuance deluge by the government in the early part of the year amongst significant global volatility

- The China 10YR government bond has moved in a 35bp range (low 1.60% - high 1.95%) since the start of the year.

- By comparison the US 10YR government bond has moved in a 80bps range (low 4.00% - high 4.80%).

- China’s bond futures are modestly higher today with the 10YR +0.06 at 109.05; remaining above all major moving averages. The nearest being the 20-day EMA of 108.46.

- China’s 2YR bond future is flat lower by -0.01 today at 102.57, touching the 50-day EMA of 102.57. Beneath that is the 20-day EMA of 102.53.

- China’s 10YR CGB is at 1.65%; -1bp lower today.

- Tomorrow sees the release of 1Q GDP where market expects an expansion of +5.2%

USD: Freefall Pauses For A Breath

The BBDXY range overnight was 1227.25 - 1235.95, Asia is dealing around 1232 currently, very similar levels to yesterday as the market tries to consolidate.

- Earlier, US Tsy Secretary Bessent said there is no evidence of sovereign sales of US government debt and the USD is still a global reserve currency. He also said there will be first-mover advantage in trade talks.(per BBG TV)

- Still, focus will remain on the USD's and US Tsys potential erosion of safe haven status. Our US based policy team noted this in an interview overnight with a former Fed and US Tsy Department official, see this link for more details.

- EUR/USD will remain in focus, with traders targeting a move back to 1.2000 in the Euro as the USD’s safe haven role is reassessed. There are structural forces underpinning these gains: Firstly Germany loosening its fiscal rules will provide a buttressing in the euro-area should there be a global downturn and secondly tariffs will eventually reduce Europe's trade surplus with the US, meaning less revenue gets invested back into USD assets.(per BBG)

- Technically, the backdrop for the BBDXY index remains quite poor. A move back below 1200 in the BBDXY would likely see the move lower gather momentum.

- After such a quick move lower though it is normal to have some positions pared back as we head towards a long weekend. Expect sellers to reengage on bounces back towards the 1250/60 area.

- Data: Upcoming US data: Empire Man 15/04, Retail Sales 16/04

Fig 1: Break down in EUR/USD and Yield Differentials

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Richer, Little Changed After Minutes, RBA Remains Cautious

ACGBs (YM +2.0 & XM +7.0) are little changed after the release of the RBA Minutes for the April Meeting. In summary:

- The Board judged that economic conditions were broadly in line with forecasts, with inflation gradually declining and the labour market still tight. Risks to the outlook were seen as balanced, including global trade uncertainty and domestic factors like wages and productivity.

- Given this, the Board decided to keep the cash rate unchanged, emphasising the need for caution. Future decisions will depend on incoming data, especially on inflation, employment, and global developments.

- The Board reiterated its commitment to bringing inflation back to target without sacrificing gains in employment and stressed the importance of flexibility in policy

- Members discussed the staff’s latest assessment of the pace at which the RBA’s holdings of government bonds were running down. The current approach is to hold these bonds until maturity.

- Cash US tsys are 1-3bps richer, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 2-7bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing +1 to +4.

- RBA-dated OIS pricing is flat to 4bps softer across meetings today. A 50bp rate cut in May is given a 39% probability.