NZD: Trades In A Range

The NZD had a range overnight of 0.5924 - 0.5968, Asia is trading around 0.5930. US Stocks reacted to the break higher in yields and saw some reversion after its recent rally higher. The NZD struggled to hold onto its earlier gains as it drifted lower in the US session in sympathy with stocks.

- “New Zealand’s budget update is likely to project a slower near-term fiscal consolidation path as a weaker economy weighs on revenues. We expect larger deficits in the near term, before a cyclical recovery in revenues drives a return to surplus in 2028-29.”(BBG)

- “The USD declined overnight on speculation that Washington may press the case for a weaker US currency at a Group of Seven meeting this week.”(BBG)

- This morning headlines from the meeting between Bessent and Kato suggest that this was not the case : “*BESSENT, JAPAN'S FM: EXCHANGE RATES SHOULD BE MARKET DETERMINED" - BBG, whilst adding "US TREASURY DEPT: AS THEIR PREVIOUS MEETING, THEY DID NOT DISCUSS FOREIGN EXCHANGE LEVELS - [RTRS]"

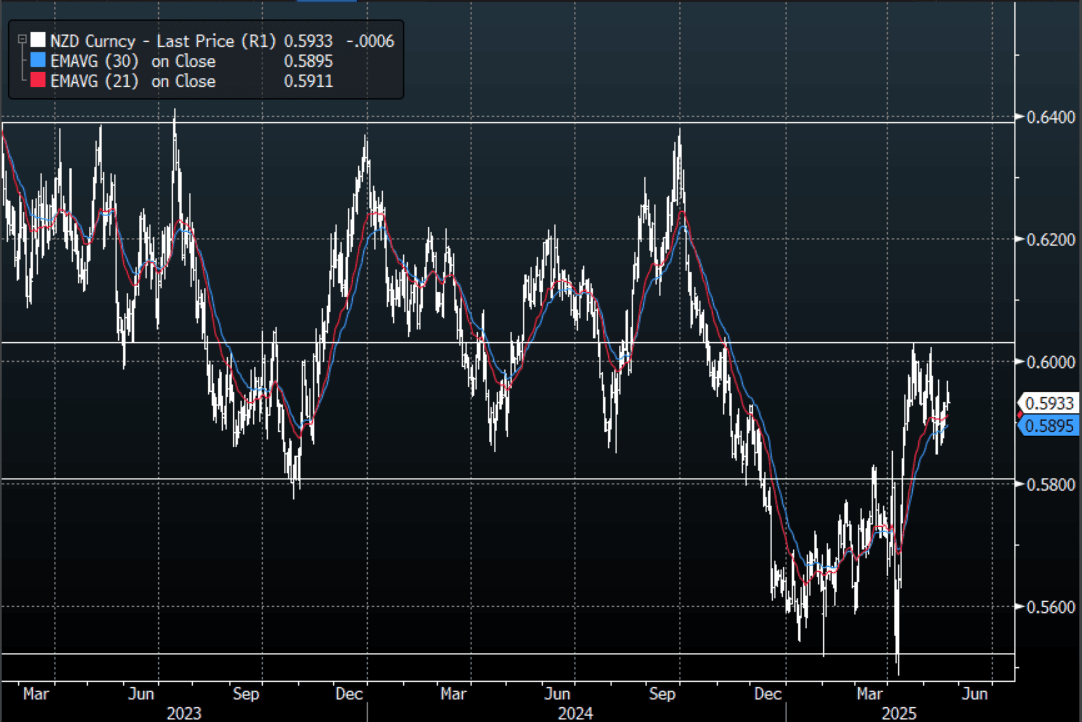

- The NZD continues to look comfortable in a 0.5850/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here is needed to regain momentum.

- CFTC Data showed Asset managers continuing to build back their shorts, while the leveraged community continued to reduce their own short.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.5705(NZD805m May 23), 0.5980(NZD513m May26)

Data/Event : NZ Budget

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUDUSD Higher But A$ Underperforms Overall

AUDUSD’s break above 64c yesterday was maintained with the pair rising 0.6% to 0.6415 after a high of 0.6438 earlier, but it still underperformed the rest of the G10, except CAD, pressured by weaker risk appetite. There was broad-based weakness in the US dollar with the BBDXY index down 0.7% as White House attacks on the Fed continued with President Trump saying that “preemptive” rate cuts are being “called for by many”. Worries over Fed independence have weighed on the greenback, long-dated Treasuries and US equities.

- AUDUSD has broken above resistance at 0.6409. This has opened up 0.6428, which was exceeded a number of times on Monday but not held. A clear break would open up 0.6471.

- Kiwi outperformed the G10 leaving AUDNZD down 0.4% to 1.0694 following a trough of 1.0678, the lowest since March 2024. It has started today slightly higher at 1.0697.

- The euro was an outperformer again and so AUDEUR fell 0.4% to 0.5574 off the intraday low of 0.5555 during Monday’s APAC session. This was the weakest level since March 2020. AUDGBP was only slightly lower at 0.4796.

- The yen did not perform as well as some of the European currencies but AUDJPY was still down 0.3% to 90.38 after falling to 89.97 early in the day. It is currently slightly lower at 90.32.

- Equities were closed in Europe but the S&P fell 2.4% and its e-mini is down 0.1% so far today. Oil prices fell with Brent -2.2% to $66.47/bbl. Copper is down 0.4% while iron ore remains around $99/t.

- Today preliminary April Australian S&P Global PMIs are released.

CNH: Still Lagging Broader USD Sell-off, USD/CNH Back Under 7.3000

USD/CNH tracks near 7.2940 in early Tuesday dealings, after CNH posted a 0.17% gain for Monday's session. Intra-session lows for Monday came in at 7.2833, as broader USD resumed sharp declines. The BBDXY index lost 0.70%, the DXY fell 0.88%, with US assets under pressure following Trump remarks against US Fed Chair Powell. Spot USD/CNY finished up at 7.2918, while the CNY CFETS basket tracker fell 0.18% to sub 96.00 (per BBG).

- For USD/CNH technicals, Monday intra-session lows were under the 50-day EMA (7.2875), but we couldn't sustain this down move. Below this level we have 7.2730 the 100-day EMA, while the 200-day support point is close to 7.2525. Highs from last week were just under 7.3350.

- CNH continues to lag broader USD weakness. The CNH/JPY cross got to fresh lows of 19.2757, but sits slightly higher now, last near 19.3060. EUR/CNH pushed above 8.43, but sits back closer to 8.400 in early Tuesday trade.

- Yesterday China warned countries against striking deals with the US that could impact China's interests. This follows various US media reports that the US would seek to isolate China through tariffs/trade deals with other countries/regions. China commodity import volumes for some US products have fallen sharply in recent months, particularly for LNG (per BBG).

- The local data calendar has March FX settlement figures out later today, which usually come out in the afternoon, which should provide an update on capital flow pressures for China.

US TSYS: Sell-Off

TYM5 reopens at 110-24, down 0-02 from closing levels in today’s Asia-Pac session.

- Overnight US 10-year yields had a range of 4.3287% - 4.4185%, closing near the highs around 4.41%, as US treasuries got sold when risk turned lower.

- Treasuries look to finish mostly lower Monday, curves twist steeper as the short end outperforms a sell-off in the long end, risk sentiment hampered as stocks hold at or near session lows.

- Global trade remains the greater concern, markets await something concrete in tariff negotiations vs. hopes and promises that talks with dozens of countries are going well, while Pres Trump berates Fed Chairman Powell and reiterates a call for "preemptive cuts".

- Yields have bounced off their support around the 4.25 area, and the correlation between yields and the USD continues to break down as US assets are being exited en masse.

- The IMF releases its World Economic Outlook tonight. The market will be keen to see its assessment of the recent turmoil.