EU UTILITIES: TenneT NL: Government Guarantee

(TENN; A3/BBB+/NR)

Rating actions were previously flagged, triggered by the debt transfer following state approval of the guarantee.

- All TenneT senior bonds have been transferred to TenneT Netherlands.

- As per the consent solicitation process, the below par bonds are now guaranteed by the Dutch state. These are now rated Aaa/AAA.

- TenneT NL has a baseline rating of Baa3/BB, with three/four notches uplift to A3/BBB+. This rating applies to the outstanding above par bonds at the time of consent solicitation.

- Hybrids remain at Tennet Holding and were affirmed at BB- with S&P and downgraded to Ba2 from Baa3 at Moody’s due to structural subordination to TenneT NL and TenneT DE debt.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: UK, Japan CPIs, Prelim PMIs and Fed Powell are the focus this Week

- Aside from the NZD (up 0.22%) and the AUD (up 0.11%), the rest of the G10 Currencies are closer to flat against the Dollar, the Yen is the worst performer, albeit by a small 0.16%.

- Overall, all the G10 FX ranges have been fairly contained, even the volatile USDJPY is only trading in 53 pips range.

- The main focus for the Yen this Week is on Friday's Japan CPI.

- The Pound exchanges hand in a tight 26 pips range and Market Participants will have their eyes on the UK Inflation print due on Wednesday.

- Focus this Week is on UK, Japan CPIs, Prelim services PMIs, but ALL EYES are on Powell's speech Friday.

STIR: Flash PMIs Headline This Week's Regional Calendar

This week’s regional calendar is headlined by the August flash PMIs (Thursday). The ECB-dated OIS implied probability of a September cut is less than 5%, and only a much weaker-than-expected set of flash PMI readings (alongside a downward inflation surprise at the end of the month) could put a cut back on the table. Such an outcome appears unlikely. The composite PMI has been slowly trending higher since November 2024, with the April/May tariff-induced uncertainty only having a temporary negative impact on momentum.

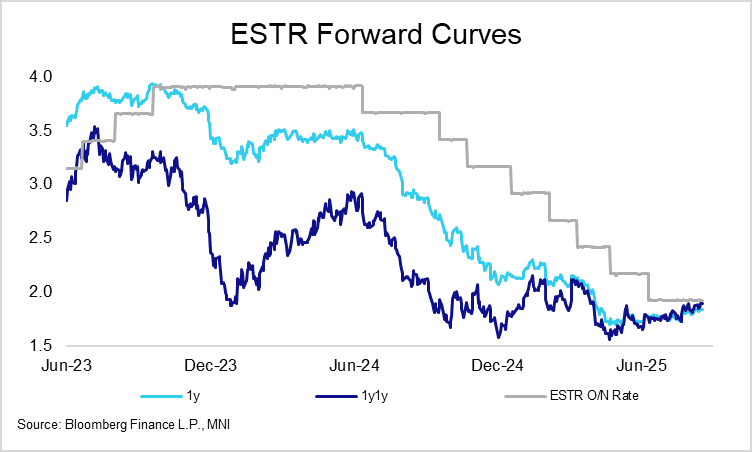

- EUR STIRs are little changed from Friday’s closing levels. The 1y ESTR swap rate is currently 1.84%, still below the pre-Liberation Day level of 1.99% but above the 1.72% seen prior to the June ECB decision. The 1y1y forward rate has seen a more notable hawkish move since early June. The chart below shows markets gradually accepting that the easing cycle is close to (or at) its close.

- Outgoing ECB Governing Councillor Holzmann called for more transparency on decisions in an interview with Bloomberg, including expressing support for a Fed-style dot plot. It’s worth noting that such an idea has been rejected by the likes of Chief Economist Lane and Bundesbank President Nagel in recent months.

- ECB Q3 Negotiated Wages are also due this week (Friday). However, the relative importance of this reading has declined in recent quarters since the ECB started publishing its forward-looking wage tracker.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.914 | -1.0 |

| Oct-25 | 1.881 | -4.3 |

| Dec-25 | 1.819 | -10.5 |

| Feb-26 | 1.798 | -12.6 |

| Mar-26 | 1.760 | -16.4 |

| Apr-26 | 1.758 | -16.6 |

| Jun-26 | 1.758 | -16.6 |

| Jul-26 | 1.762 | -16.2 |

| Source: MNI/Bloomberg Finance L.P. | ||

EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6600.00 Round number resistance

- RES 3: 6543.43 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and Alltime High

- PRICE: 6470.25 @ 07:24 BST Aug 18

- SUP 1: 6392.29 20-day EMA

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6267.88 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6392.29, the 20-day EMA, and 6267.88, the 50-day EMA.