EU COMMUNICATIONS: Telekom Austria: Q3 Results

Oct-15 10:55

(TKAAV; A3/A-/A-)

EBITDAal rose 3% YoY, supported by higher ICT and equipment revenues and stable core OPEX, though lower equipment margins and restructuring charges weighed. Marginal positive on stronger FCF (lower maintenance/rental costs), and a further tick lower in leverage. FY guidance reaffirmed.

- Q3 Revs: €1.4bn (+3% YoY, 1% miss). YTD: €4.1bn (+4% YoY).

- Q3 EBITDAal: €563mn (+3% YoY, 2% miss). YTD: €1.6bn (+4% YoY).

- Q3 FCF: €196mn (+13% YoY). YTD: €528mn (+52% YoY).

- Reported leverage 0.9x vs. 1x QoQ vs. 1.1x YoY

- FY guidance affirmed. Capex guidance tweaked lower.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

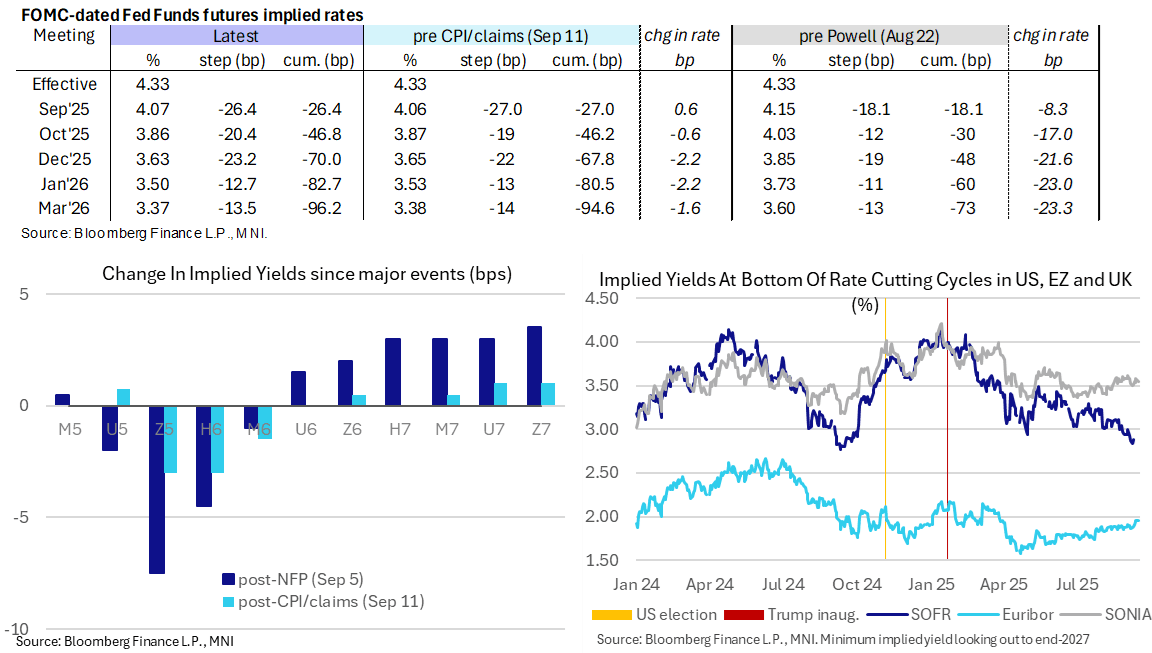

STIR: Fed Personnel Deliberations Watched Later On

Sep-15 10:51

- Fed Funds implied rates for near-term meetings are near unchanged since Friday’s close.

- Two Fed personnel deliberations today:

- Senate cloture vote on CEA’s Miran nomination as a Fed Governor at ~1730ET before full confirmation voter ~2000ET. Expected to pass having already passed 13-11 in the Senate Banking Committee.

- Watching for a reaction after the Trump administration on Sunday filed an appeal for a stay on a lower court block on Gov Cook's firing, a long-shot bid to remove Cook ahead of the FOMC meeting. The administration previously asked for a ruling by today. While unlikely, the Trump administration is targeting an emergency ruling from the Supreme Court on the so-called 'shadow docket'.

- Data picks up tomorrow with retail sales whilst the FOMC decision of course looms large on Wednesday. MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Sep2025_60a3bc30d1.pdf

- Cumulative cuts from 4.33% effective: 26.5bp Sep, 47bp Oct, 70bp Dec, 82.5bp Jan and 96bp Mar.

- SOFR futures see minor twist flattening, 1 tick lower in the U5 to 1.5 ticks firmer through 2027 contracts.

- The SOFR implied terminal yield of 2.915% (SFRH7, -1.5bp) remains off last Monday’s close of 2.84% (lowest since Sep 2024 and one of the lowest for the cycle) but still points to more than 140bp of cuts ahead.

OUTLOOK: Price Signal Summary - Gold Bull Remain In The Driver's Seat

Sep-15 10:39

- On the commodity front, Gold remains in a clear bull cycle and continues to trade at its recent highs. The yellow metal traded to a fresh all-time high once again, last week. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a 2.382 projection of the Dec 30 ’24 - Apr 3 - 7 price swing. Initial firm support lies at $3504.1, the 20-day EMA. Initial firm support lies at $3504.1, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

FOREX: Dollar Index Tilts Lower, GBPUSD Rises Above 1.3600

Sep-15 10:39

- The dollar index has been edging lower heading into the NY crossover on Monday, as markets await a stacked data and central bank calendar this week, headlined by the Fed. Amid the moves, GBP is a clear outperformer, with cable rising above 1.3600 to a fresh two-month high.

- Bullish conditions for GBPUSD have been bolstered this morning, following the break of the bull trigger located at 1.3595, the August 14 high. The rally that started Sep 3 has retraced the steep Sep 2 sell-off and highlights a stronger bullish development. This suggests the corrective cycle between Aug 14 - Sep 3 is over.

- Immediate resistance is found at 1.3636, the 76.4% retracement of the Jul 1 - Aug 1 downleg, before 1.3681, the Jul 4 high.UK Labour market figures, CPI data and the BOE decision will place a huge amount of attention on sterling this week.

- Softer dollar dynamics have also allowed AUDUSD to rise back towards cycle highs. Last week’s gains plus the breach of 0.6625, the Jul 24 high and bull trigger, confirmed a resumption of the technical uptrend, and the pair has narrowed the gap substantially to the US election related highs at 0.6688.

- In similar vein, EURUSD has edged higher above 1.1750 in recent trade. While underlying bullish conditions remain intact for EURUSD, this week’s Fed decision could be a pivotal moment for the pair, with the 1.1829 bull trigger and the 50-day EMA (intersecting at 1.1639) remaining the key short-term parameters.

- US Empire State manufacturing data headlines a relatively quiet economic calendar on Monday. No surprises are expected from ECB President Lagarde, due to speak at Montaigne Institute’s 25th anniversary event, in Paris.