JGBS: Slightly Mixed, Post-Auction 30Y Rally Stalls At 50D-SMA

JGB futures are stronger, +12 compared to settlement levels.

- "Adviser to Takaichi's policy circle says weak yen is good for the economy." RTRS

- "Ex-BOJ Deputy Governor Wakatabe said the BOJ will likely find it hard to justify raising rates this year given prospects of weak Q3 GDP. He added the BOJ must coordinate policy with the government but does not need to keep rates low solely to fund government spending." RTRS

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are 1bp richer to 2bps cheaper across benchmarks, with the futures-linked 7-year outperforming.

- The benchmark 30-year yield is 1.9bp higher at 3.176% versus the cycle high of 3.351% set earlier in the week ahead of supply.

- With the auction results only being mixed, the recent ~20bp rally in the 30-year appears to have been an unwind of the yield overshoot associated with the change in political leadership over the weekend. Today’s move, therefore, potentially suggests that the market may have gone too far the other way now, with the 50D-SMA acting as resistance.

- Tomorrow, the local calendar will see PPI and Bank Lending data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

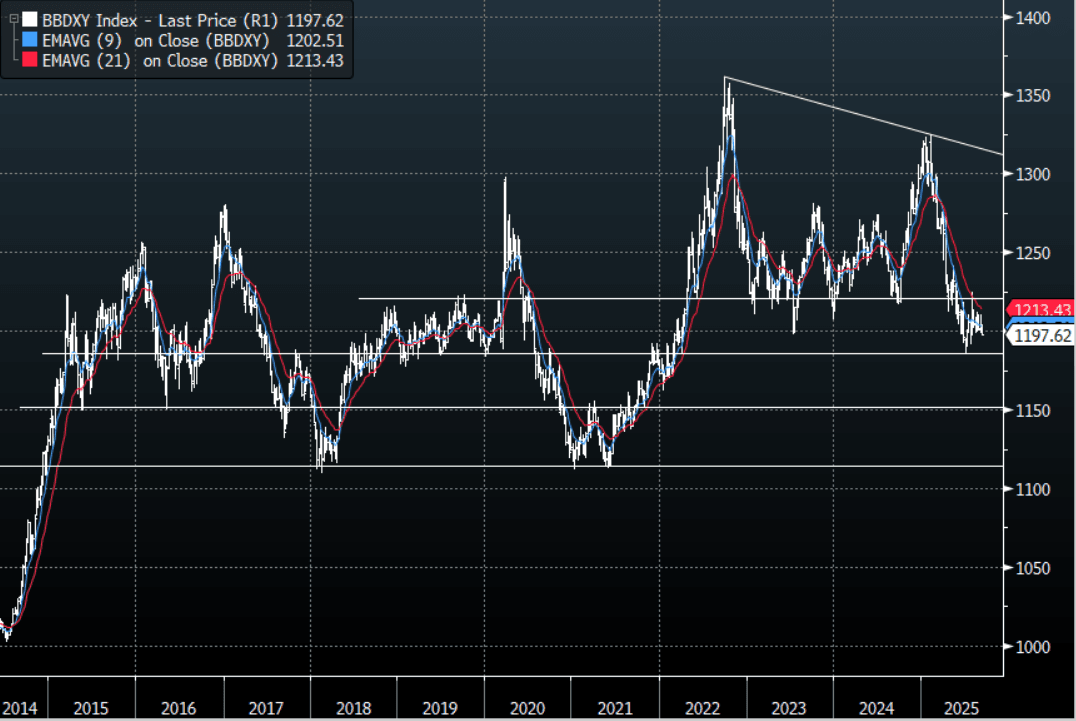

FOREX: Asia FX Wrap - BBDXY Probing Below 1200

The BBDXY has had a range of 1197.30 - 1198.68 in the Asia-Pac session, it is currently trading around 1197, -0.08%. The USD trades very heavy as the moves in US yields start to take their toll. The headwinds for the USD seem to be compounding and a look below 1195 feels almost inevitable. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. Should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken.

- EUR/USD - Asian range 1.1759 - 1.1778, Asia is currently trading 1.1770. The pair continues to grind higher with focus turning back towards the range highs. EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3544 - 1.3574, Asia is currently dealing around 1.3570. The pair bounced strongly off its support around 1.3350 last week. The pair is grinding higher looking towards the top end of its 1.3350-1.3650 range.

- USD/CNH - Asian range 7.1168 - 7.1238, the USD/CNY fix printed 7.1008, Asia is currently dealing around 7.1200. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3652, US 10-Year 4.05%, BBDXY 1197, Crude Oil $62.66

- Data/Events : France Industrial Production MoM

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Another New Record High, US Payroll Revisions Later

Gold prices reached a new record high of $3654.57/oz during today’s APAC session but are currently around $3652.8 to be up 0.5% on the day. Friday’s disappointing US payroll data has bolstered Fed cut expectations with over 25bp now priced in for September 17 and almost 75bp by year end. The market is also waiting for the ruling on whether Fed Governor Cook can be removed. The US dollar is 0.1% lower today while yields are little changed.

- Gold held below resistance at $3674.8. Today’s US payroll revisions, Wednesday’s August PPI and Thursday’s CPI will be important for the rate outlook and thus for non-yield bearing bullion.

- ETF flows into gold have also pushed prices higher with Bloomberg reporting Monday’s inflows were the highest in close to 3 months.

- Silver is off its intraday low of $41.209 to be little changed around $41.35. It reached $41.419 earlier holding below resistance $41.467.

- Equities are mixed with the S&P e-mini is up 0.1% and Hang Seng +0.8% but CSI 300 down 0.5% and Jakarta Comp -1.6%. Oil prices are higher again with WTI +0.6% to $62.66/bbl. Copper is up 0.3%.

- US benchmark revisions to payrolls are released later. US August NFIB small business optimism prints. The ECB’s Montagner & Machado and the BoE’s Breeden appear.

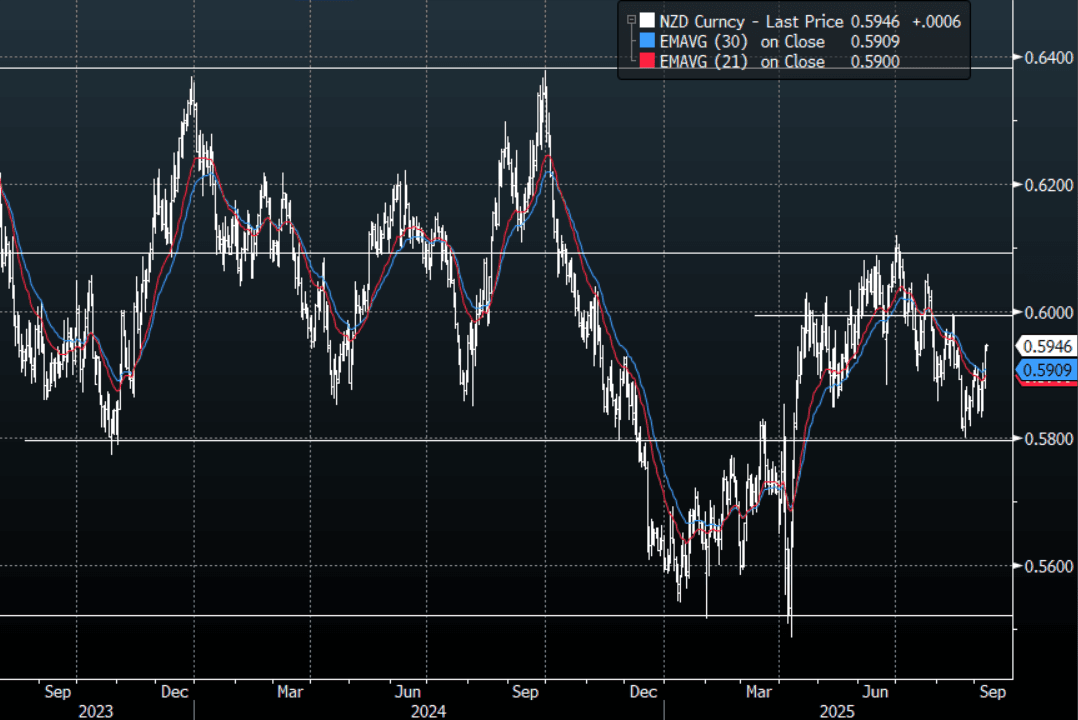

NZD: Asia Wrap - NZD/USD In The Sell Zone, The USD Is A Concern Though

The NZD/USD had a range of 0.5937 - 0.5949 in the Asia-Pac session, going into the London open trading around 0.5845, +0.10%. US rates extended lower again and the USD traded soft, the headwinds for the USD seem to be compounding which points to a potential look below its support. The NZD has bounced into what should be the perfect zone to fade for bears, the price action for the USD though gives me pause. CFTC Data shows light positioning in a market that is struggling for a strong trend as we move back into the middle of the recent 0.5800-0.6100 range.

- (Bloomberg) -- “New Zealand’s main opposition Labour Party is open to having a discussion about the RBNZ’s 1-3% inflation target, the NZ Herald reports.”

- Q2 Data Suggesting Weak GDP Outcome: Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD515m Sept 10), 0.5870(NZD320m Sept 10) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225).

- AUD/NZD range for the session has been 1.1093 - 1.1105, currently trading 1.1100. The Cross is consolidating around 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P