AUSSIE BONDS: Sharply Cheaper After CPI Beat, 0% Chance For Cut Next Week

ACGBs (YM -8.5 & XM -4.0) are weaker and at session cheaps.

- The headline August CPI print was 3.0%y/y, against a 2.9% market consensus and 2.8% July outcome. The trimmed mean was 2.6% y/y, after printing 2.7% in July.

- Today's data will reinforce some caution for the RBA around further easing. It is likely to firm the no-change stance next week (although market pricing has priced in very little chance of a move). The Q3 CPI print is out on Oct 29, with the RBA outcome on Nov 4.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash ACGBs are 4-8bps cheaper on the day, with a flatter curve and the AU-US 10-year yield differential at +20bps.

- The bills strip is -8 to -11 across contracts.

- RBA-dated OIS pricing is sharply firmer across meetings after the data. A 25bp rate cut in September is given a 0% probability, with a cumulative 17bps (22bps pre-data) of easing priced by year-end.

- Tomorrow, the local calendar will see Job Vacancies.

- The AOFM plans to sell A$900mn of the 2.75% 21 November 2029 bond on Friday

- (Bloomberg) NSW TCorp is marketing a Feb 2039 bond that will carry a coupon of 5.25%, according to Westpac.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed With A Modest Bull-Steepener, But Off Bests

NZGBs closed showing a modest bull-steepener, with benchmark yields 1-3bps lower, after opening 5-6bps richer following the strong Friday for US tsys.

- Cash US tsys are ~2bps cheaper in today’s Asia-Pac session.

- NZGBs underperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield spreads 5bps and 3bps wider, respectively, on the day.

- Swap rates closed 2-3bps higher.

- (Bloomberg) “NZ Prime Minister Christopher Luxon said he personally agrees that the Reserve Bank should have cut the Official Cash Rate by 50 basis points last week.

- Luxon said he routinely meets with RBNZ Governor Christian Hawkesby before rate decisions to discuss how the economy is performing and that he suggested the bank should be more aggressive. Luxon emphasized that the Reserve Bank's independence is "sacrosanct" and that his conversations with RBNZ officials are constructive and do not involve directing the bank.”

- RBNZ dated OIS pricing closed slightly softer across meetings. 19bps of easing is priced for October, with a cumulative 36bps by November 2025.

- The local calendar will be empty tomorrow and Wednesday, ahead of Filled Jobs and ANZ Business Confidence on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 4.50% May-35 bond.

FOREX: Asia FX Wrap - BBDXY(USD) Looking To Test Below 1200 Again

The BBDXY has had a range of 1201.36 - 1203.53 in the Asia-Pac session, it is currently trading around 1202, +0.05%. The USD collapsed with US yields as the market interpreted Powell to be surprisingly dovish. ‘Up the stairs and down the elevator’ would be an accurate way to describe price action in the USD with the market being dragged kicking and screaming to reduce its shorts into the event but is very quick to reinstate USD shorts when it perceived very little hawkish push back. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. There are some who do not see Powell’s speech to be as dovish, price action over the next couple of days will determine who is right.

- EUR/USD - Asian range 1.1694 - 1.1724, Asia is currently trading 1.1705. The market is attempting to regain its upward momentum after Jackson Hole. The pair needs to sustain a break back above 1.1800/1.1850 to start another leg higher.

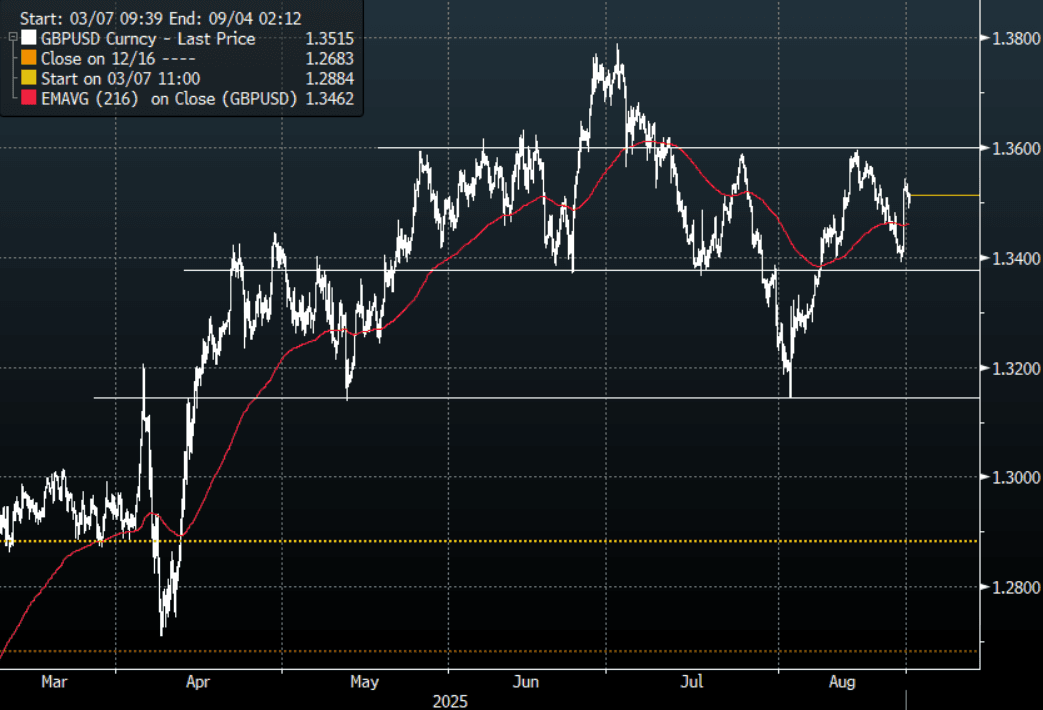

- GBP/USD - Asian range 1.3391 - 1.3544, Asia is currently dealing around 1.3515. The pair found solid demand towards its support around 1.3400 and has bounced nicely from there with the help of Powell. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1572-7.1743, the USD/CNY fix printed 7.1161, Asia is currently dealing around 7.1590. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3366, US 10-Year 4.27%, BBDXY 1202, Crude Oil $63.79

- Data/Events : Germany IFO

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Continues To Find Support From Fed Easing Expectations

Oil prices continued gradually moving higher during today’s APAC trading but remain in a narrow range. WTI fell to $63.53/bbl and then recovered to $63.89. It is now up 0.2% to $63.78. Brent is 0.2% higher at $67.86/bbl after a low of $67.57 followed by a high of $67.91. The USD index is up slightly.

- The US OIS market now has around an 88% chance of a 25bp rate cut on September 17 priced in and about 50% of another in October. Improved easing prospects should support oil as it improves the demand outlook. The market will watch upcoming key data to gauge where the economy is and especially any feed through of increased tariffs on US inflation.

- July PCE prices this Friday, August ISM next Tuesday and August payrolls Friday 5 September are key upcoming releases.

- Trump has again threatened Russia with “massive sanctions or massive tariffs or both” if an agreement isn’t reached in two weeks but a decision would be made then whether to take these steps or admit “it’s your fight” and do nothing. Punitive tariffs on consumers of Russian crude are the main market worry. India could still face an additional 25% US duty.

- The Fed’s Logan and Williams speak later. July Chicago Fed index and August Dallas Fed manufacturing print as well as some July US housing data and Germany’s August Ifo survey. The UK is closed for a holiday.