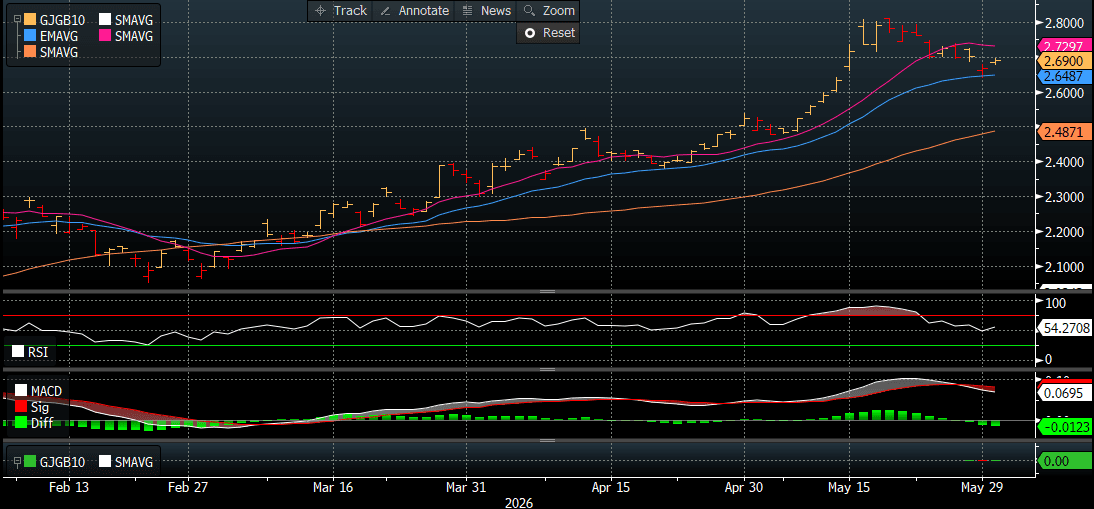

JGBS: Selling Extends After A Heavy End To Last Quarter, 10Y Supply Tomorrow

JGB futures are weaker, -25 compared to settlement levels. * MNI BRIEF: BOJ Tankan: Business Inflat...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Tech Explosion Sees Another Day of Gains for AI stocks

The broader Asia equity story is still being driven by AI-related demand, and that is spilling into China's technology supply chain. Investors are focusing on semiconductor equipment, chip design, data infrastructure, and advanced manufacturing names that benefit from China's push for technological self-sufficiency. Several onshore stories raised the possibility for an increase in passive inflows of around $40bn into semiconductor and technology stocks from upcoming CSI index rebalancing. However a moderation in manufacturing PMIs today was enough to weigh heavy on domestic equities with the CSI 300 down -0.55% whilst offshore sees the Hang Seng up +0.8% on renewed optimism that an agreement is near in the Iran US conflict.

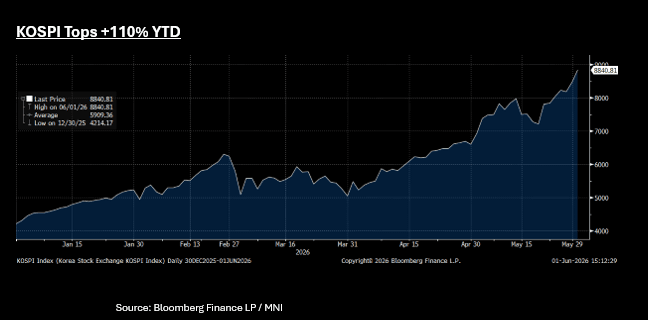

The same thematics played out in the KOSPI today after very strong export data saw Samsung up +9% and the KOSPI up +4.5% to reach a new high of 8,856. This takes the KOSPI year to date performance through +110% - even despite a trading halt today given the rapid move higher.

For the NIKKEI, continued enthusiasm around AI infrastructure, chips, and data-center spending sees the index up +0.8%. Japan's AI-linked names are again leading gains, with investors extending the global technology rally seen in the US and elsewhere in Asia.The NIKKEI did break above 67,000 and reach a new high of 67,231 before falling back as profit takers stepped in. Softbank Group has led the way with gains of +13% today. A growing global thematic - observable in Japan - is only a few industry groups are delivering positive returns, with IT-related sectors overwhelming the returns of all other sectors. This raises questions as to the health of the broader economy.

JGBS: Cheaper With US Tsys Despite Q1 Capex Miss, 10Y Supply Tomorrow

JGB futures are weaker but off lows, -21 compared to settlement levels.

- Japan Q1 capex printed well below forecasts. The headline y/y was flat, versus a 4.0% estimate, while 6.5% was the prior. The ex-software Capex print was -1.4%y/y, against a 5.4% forecast and Q4 print of 7.3%. In q/q terms, Capex ex software fell 3.5%.

- The company profits print was better than forecast though, up 14.6%y/y, versus 5.3% forecast and 4.7% prior. This result, all else equal, may leave businesses in a solid place to deliver firm wage outcomes, which remains a key policy goal for the authorities. Manufacturing profits were up 42.9%y/y, while non-manufacturing rose 1.4%y/y.

- Cash US tsys are 2-3bps cheaper in today's Asia-Pac session as uncertainty over a peal deal between the US and Iran pushes oil prices higher. Brent crude rises more than 2%, rebounding from a six-week low, after the US and Iran traded messages over the weekend seeking changes to a draft agreement that would extend a ceasefire and open the Strait of Hormuz.

- Cash JGBs are 1-3bps cheaper across benchmarks, with the 20-year leading.

- The swaps curve has twist-flattened, with rates 1bp higher to 5bps lower. Swap spreads are tighter.

- Tomorrow, the local calendar will see Monetary Base data alongside 10-year supply.

Bloomberg Finance LP

BUND TECHS: (M6) Resistance Remains Exposed

- RES 4: 127.31 61.8% retracement of the Mar 2 - May 18 bear leg

- RES 3: 127.00 Round number resistance

- RES 2: 126.64 High Apr 8 and key resistance

- RES 1: 126.54 High May 29

- PRICE: 126.121 @ 05:51 BST Jun 1

- SUP 1: 125.48 20-day EMA

- SUP 2: 124.60/123.74 Low May 21 / 18 and the bear trigger

- SUP 3: 123.59 1.764 proj of the Mar 10 - 13 - 18 price swing

- SUP 4: 123.15 2.000 proj of the Mar 10 - 13 - 18 price swing

Short-term conditions in Bund futures remain bullish following recent gains. Last week’s rally resulted in a break of the 50-day EMA - currently at 125.64. This signals scope for a continuation higher near-term. Key resistance to watch is 126.64, the Apr 8 high. A move through this hurdle would highlight a stronger reversal. It is still possible that the latest recovery is a correction. Key support has been defined at 123.74, the May 18 low.