CLP: Sell-Side Views on CLP Following Surprise Reserves Plan Announcement

- HSBC note that they have been positive on the CLP on the back of tariff developments, resilient local growth, and a fairly constructive local policy outlook; and have an open sell USD/CLP 1m NDF trade idea. While the recent move has erased some of the gains since they put on the trade, the main drivers of the trade remain in force, for now. That being said, constant USD purchases from the central bank will now change flow dynamics for the currency and mechanically reduce the scope of future gains, all else equal, they add.

- JP Morgan note that while CLP was trading ~1% weaker on the BCCh headlines, they don’t see the weakness lasting. They note the program is designed so that neither the exchange rate evolution nor the monetary policy decisions are altered. They think current conditions are more benign and CLP should be more resilient. The macroeconomic fundamentals in Chile are more robust while valuations are pointing to some cheapness in CLP. They are therefore keeping their CLP longs for the time being but will be closely monitoring price action to see whether some reassessment is warranted.

- ING say the announcement probably means that USD/CLP is more likely to stay nearer to the middle of a 900-1000 medium-term trading range. But ING add that its low carry and now this FX reserve build program suggest it will underperform the rest of the Latam FX complex.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FRANCE DATA: Tariff Impact Clear, But Several Risks Still In Pipeline (2/2)

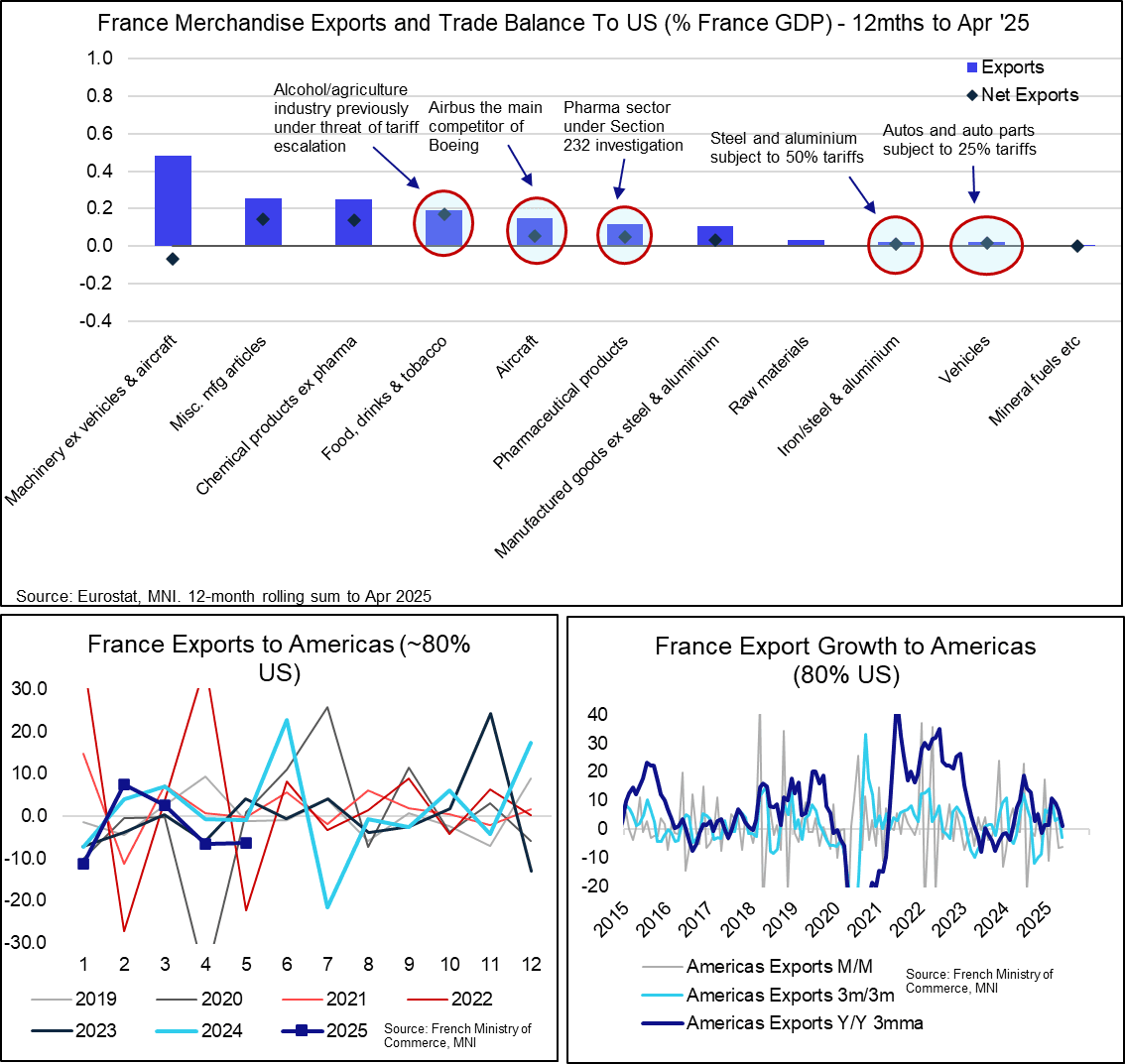

Ministry of Commerce data highlights a sharp drop in Y/Y French exports to the Americas since March, with exports falling 6.5% M/M in April and 6.4% M/M in May. The US makes up around ~80% of “Americas” exports. Clearly, already implemented tariffs and associated trade policy uncertainty are having an impact on trade with the US.

- However, Eurostat data suggests France is not too exposed to the sector-specific 50% steel/aluminium and 25% autos levies imposed by the US.

- Instead, officials will be more concerned by French sensitivity to:

- (i) Pharmaceuticals, which are currently subject to a Section 232 investigation.

- (ii) Aircraft, given Airbus’ position as Boeing’s main competitor.

- (iii) Food, alcohol and tobacco, with the agricultural sector threatened with 17% tariffs over the weekend and the alcohol sector previously being threatened with punitive measures following initial EU retaliatory plans.

- Other machinery/manufacturing exports to the US are also worth ~0.8% GDP, so are impacted by the 10% baseline reciprocal tariff.

- This sensitivity to potential future tariff announcements has likely underscored the French Government’s slower, more detailed, preference for trade negotiations than the likes of Germany (whose auto industry is more sensitive to already-announced sector-specific tariffs, for example). Reports that spirits and aircraft may be exempted from tariffs in the latest US offer will come as a relief to some French producers.

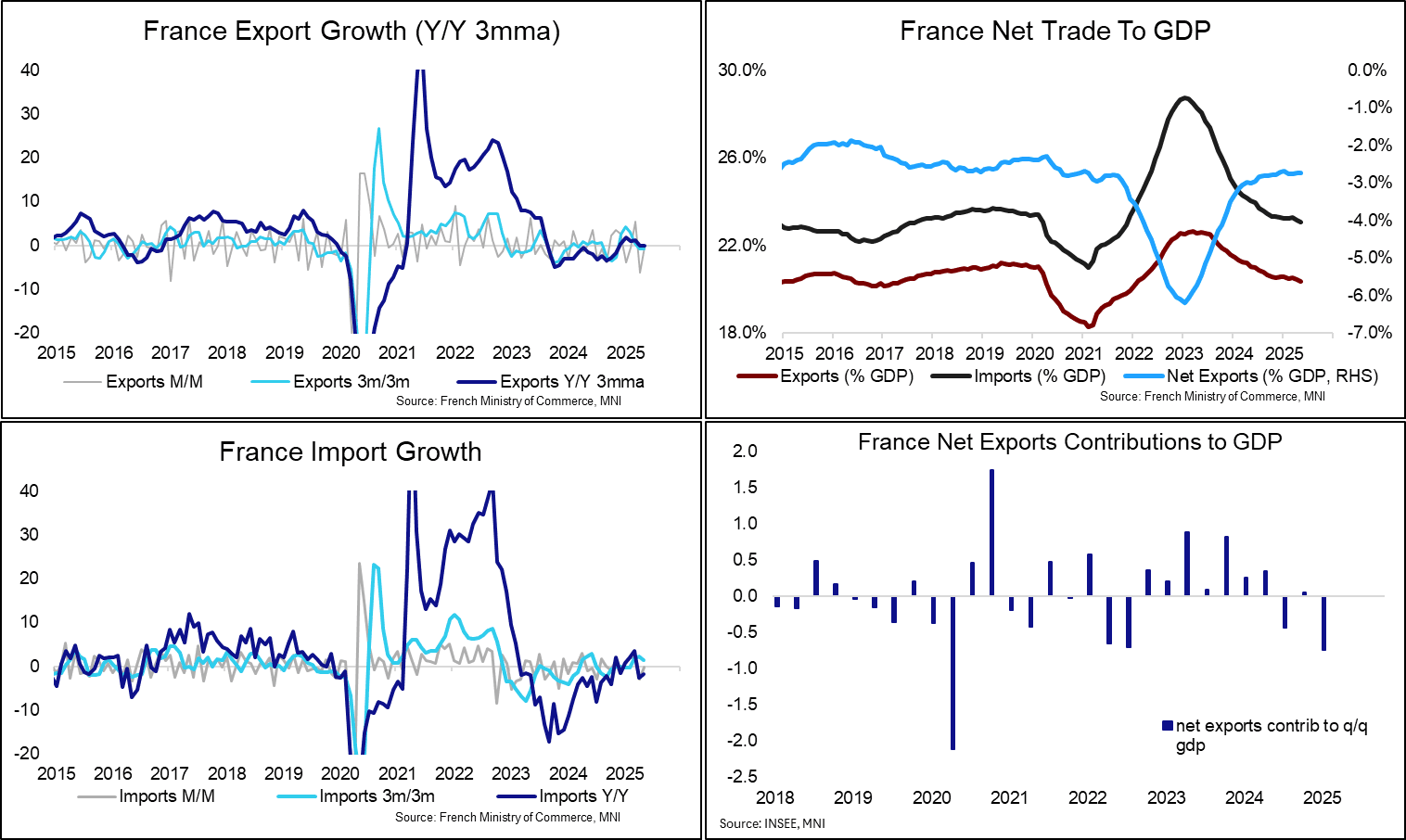

FRANCE DATA: Import and Export Trends Sluggish Post Covid (1/2)

While the French goods trade deficit to GDP is broadly back in line with pre-covid levels (~3%), the downward trend in both exports and imports is reflective of a broader sluggishness in activity. Weak demand is constraining imports, while trade uncertainty and soft partner demand is limiting export growth.

- The trade deficit was E7.8bln in May according to Ministry of Commerce data, up from E7.7bln in April. Exports (ex-military equipment) fell 0.3% M/M to E48.8bln. Export growth has been negative on an NSA sequential basis for four of the last 5 months (March was an exception with +5.3% M/M growth).

- Meanwhile, imports (ex-military equipment) fell 0.2% M/M to E56.7bln, following a 3.0% M/M fall in April. Imports were down 1.7% Y/Y in May (vs -2.6% in April, +3.4% in March), consistent with weak domestic consumption and industrial production trends seen in recent months.

- Net exports pulled Q/Q real GDP down by 0.7pp in Q1. Recent export weakness suggests a similar drag may also be seen in Q2.

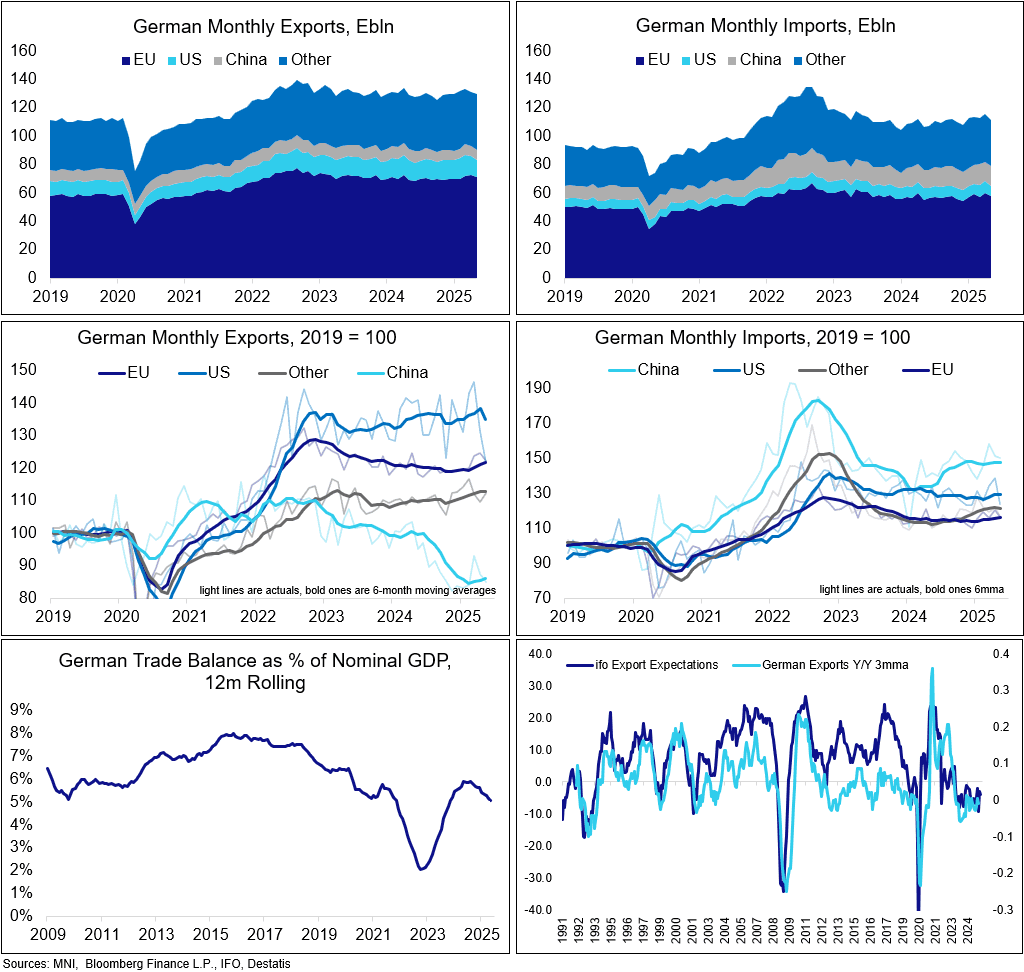

GERMAN DATA: Trade Balance Extends Real-Terms Downtrend

The German trade surplus increased in May to E18.4bln (seasonally-adjusted, vs E15.5bln cons; E15.7bln prior, revised from E14.6bln). Both exports (-1.4% M/M vs -0.5% cons; -1.7% prior, revised from -1.6%) and imports (-3.8% M/M vs -1.7% cons; 2.2% prior, revised from 3.9%) declined.

In real terms, as a % of nominal GDP on a 12-month rolling basis, the trade balance series extended its current downtrend, at 5.1% as of May, 0.9pp below levels seen around a year ago (vs 8.0% 2015 high, 2.1% 2022 low, bottom left chart).

- Across countries, an export drop to the US is consistent with the firmer tariff stance in the country. Exports to China meanwhile also dropped, sitting close to their post-pandemic lows, suggesting that an April jump might have been a one-off (mid-left chart).

- May German factory orders data showed the series holding up comparatively well from the foreign side - that could suggest some rebound in exports over the next months.

- Lower imports across the board of constituencies (mid-right chart) seen in May can be indicative of low domestic demand in the month.

- IFO export expectations fell in June, to -3.9 (-3.0 May), remaining well subdued on a historical comparison.

- "The United States has offered an agreement to the European Union that would keep a 10 percent baseline tariff on all EU goods, with some exceptions for sensitive sectors such as aircraft and spirits", Politico quoted an EU diplomat overnight - arguably, that would be quite favourable conditions for the bloc.