US STOCKS: S&P(ESU5) - Tops Out Above 6500 Again, Nvidia Results Add Headwinds

The S&P(ESU5) overnight range was 6459.25 - 6505.50, SPX closed +0.24%, Asia is currently trading around 6475, -0.30%. The ESU5 contract once again stalled above 6500 with the poor Nvidia quarterly earnings seeing it move lower into the close. The fallout from Nvidia has carried through into the Asian open with futures opening back up under pressure, E-minis -0.30%, NQU5 -0.50%. The S&P remains in a bullish uptrend, but if Nvidia sneezes the whole market will catch a cold, so how the market absorbs this input over the next couple of days will be important.

- (Bloomberg) - “Hedge funds are shorting the VIX at levels not seen since 2022, betting the market calm will last. But such extreme positioning historically foreshadowed sharp volatility spikes and stock losses.”

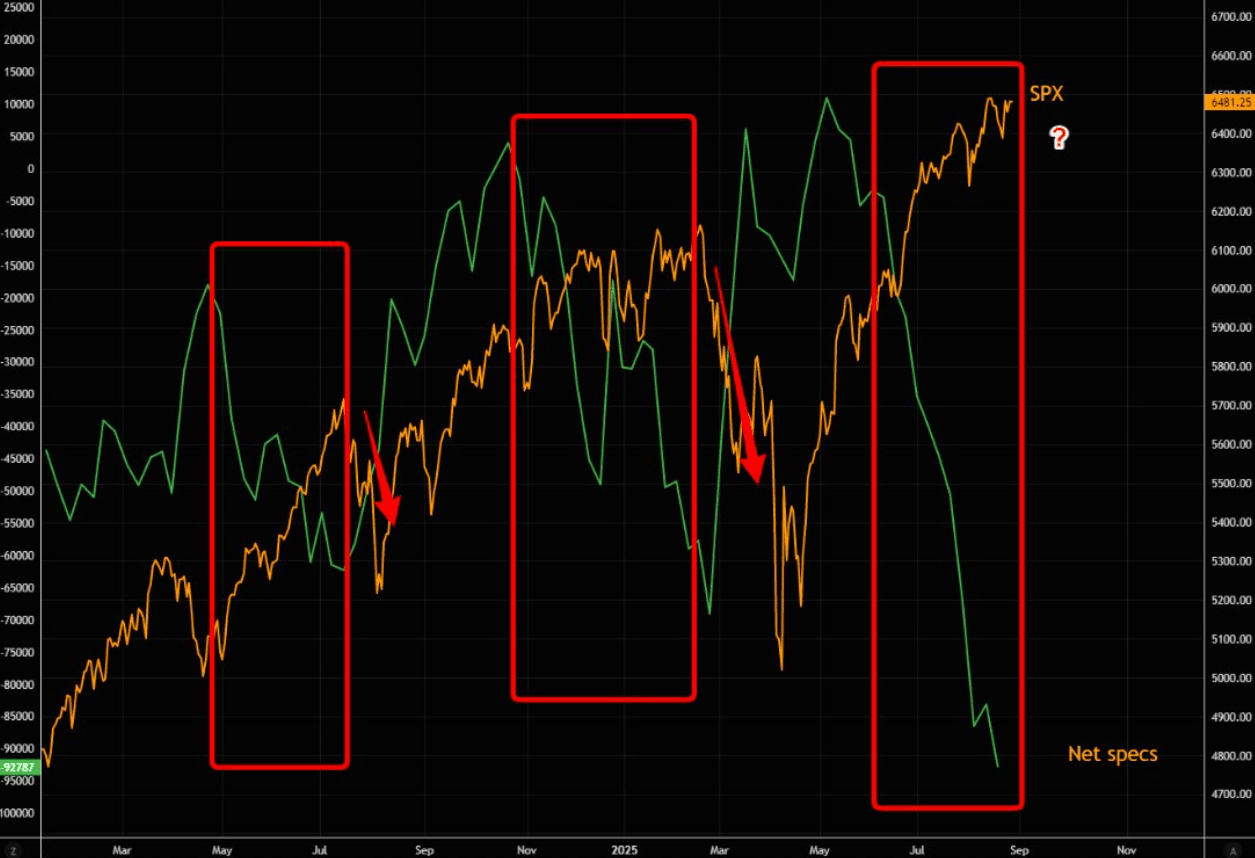

- Lance Roberts on X: “Watch closely when VIX specs short VIX in size as the markets are rising. Previous two episodes of large VIX selling over the past year ended with the SPX correcting... and this time the VIX action has been extreme. Speaking of the VIX, we are into the seasonally strong period of the year for volatility which is at least worth considering given the strong run markets have had since April.” See Fig.1 Below.

- Andrew Ackerman on X: FT: “Chaos follows when leaders capture their central banks & force them to buy government debt or cut interest rates to hold down debt service expense. Germany in the 1920s, Hungary after the second world war. Likewise, Argentina and Turkey quite recently.”

- (Bloomberg) - “Nvidia Lost $4 Billion in Revenue After China Sales Blocked: Nvidia says its compute revenue, a subcomponent of data-center revenue, fell 1% quarter-on-quarter because of a $4 billion drop in H20 sales. Those are the chips that it sells to China -- or did at least, until the US ban on exports and Chinese restrictions on imports.”

Fig 1: SPX Vs VIX Spec Shorts

Source: MNI - Market News/@LanceRoberts/@themarketear

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: AUCTION PREVIEW: ACGB May-28 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1000mn of the 2.25% 21 May 2028, issue #TB149. The line was last sold on 4 July 2025 for A$1000mn. The sale drew an average yield of 3.3071%, at a high yield of 3.3100% and was covered 3.9550x. There were 35 bidders, 14 of which were successful and 8 were allocated in full. The amount allotted at the highest yield as a percentage of the amount bid at that yield was 45.3%.

- The latest round of ACGB May-28 supply saw the weighted average yield print 0.97bps through prevailing mids (per Yieldbroker), extending the recent trend of firm pricing at ACGB auctions. However, the cover ratio dropped to 3.9550x from a robust 4.4250x at the previous outing.

- This week's ACGB supply is at the top end of the recent average weekly issuance of $1500-2200mn, with A$1200mn of the 2.75% 21 June 2035 bond on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

LNG: Russian Sanctions Threat Makes European Gas Nervous

European and US gas diverged on Monday. US President Trump’s decided to bring forward the deadline for an end to Russian hostilities in the Ukraine otherwise there would be punitive tariffs on it and those who buy its fossil fuels. This drove European prices 1.9% higher to EUR 33.12 after an intraday low of EUR 31.99, driven by the deal to buy US energy, and it is now 3.8% off the July 25 low and slightly higher this month.

- Trump said that he would bring the deadline forward to 10-12 days from July 28. He appears to have lost patience with Russian President Putin saying he’s “not so interested in talking any more” after the latter has said one thing and done another. Trump said that he’ll likely make an announcement Tuesday. The original deadline was September 2.

- While pipeline flows from Russia to the EU are almost nil, LNG imports remain high as it refills storage, although the EU is aiming to phase them out completely. It agreed to buy $750bn of US energy over the remainder of Trump’s term.

- Pipeline flows from Norway remain close to capacity after maintenance and LNG imports in July are +39% y/y, according to Inspired Plc and Bloomberg.

- US prices in contrast fell 2.5% to $3.03 after reaching a low of $2.984, the lowest since early November and below July 2024. An expected mild start to August and continued robust supply have pressured prices this month and they are now down 12.3%. The August Henry Hub contract expires Tuesday.

- Bloomberg reports that China’s demand rose in July with LNG imports likely to be in line with July last year after lower levels over the last eight months.

US TSYS: Cash Open

TYU5 is trading 110-27, up 0-02+ from its close.

- The US 2-year yield opens around 3.912%, down 0.01 from its close.

- The US 10-year yield opens around 4.405%.

- MNI US DATA: Mixed Ability Of Firms To Pass Cost Increases On In Dallas Fed District. The improvement in the Dallas Fed manufacturing survey for July came despite an apparent relative re-compression in margins although this in turn was countered by the opposite when looking six months out.

- (Bloomberg) -- The US Treasury estimates $1.01 trillion in net borrowing for July through September, up from the $554 billion it had estimated in April. The Treasury is ramping up issuance to rebuild its stockpile of cash after Congress raised the debt ceiling by $5 trillion at the beginning of this month.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward.

- Data/Events: Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.