INR: S&P Ratings Upgrade Provides Some Respite to Rupee

Aug-14 10:03

USDINR dipped moderately on the S&P’s ratings upgrade, paring some of the earlier advance, though the move struggled to gain any significant traction and spot ultimately ended the session around 0.1% in the green. Sovereign 10-year bonds yields fell as much as 10bps on the back of the upgrade. Note that Indian financial markets are shut Friday over a national holiday.

- The more benign outlook from S&P may offer the rupee some respite going forward after Trump’s tariff threats prompted a sharp drop in the Indian currency back towards its all-time lows. S&P noted that the effects of US tariffs on the Indian economy will be manageable.

- Broader rupee weakness has seen the RBI step up its intervention in currency markets, with Economic Times reporting yesterday that the central bank likely sold $5-6bln in the offshore market over the past fortnight to curb excessive depreciation.

- Significant intervention in both onshore and offshore markets has generally been less prevalent since Sanjay Malhotra took over as RBI governor in December 2024, but the latest episodes of rupee weakness have since underpinned the central bank’s commitment to smoothing excess volatility.

- In addition to presence in the offshore NDF market ahead of the Mumbai open, a dip in foreign exchange reserves suggests that dollar sales in the onshore market have also continued amid concerns that further INR weakness could stoke imported inflation and weigh on growth.

- Commerzbank noted recently that they expect USD/INR to remain well supported at the upper end of the 86-88 range in the near-term. They say the benign inflation environment gives RBI the flexibility to cut rates further if warranted to support growth, particularly given the tariff shock, and see another 50bp cut by year-end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - S&P E-Minis Trend Needle Points North

Jul-15 09:53

- In the equity space, the trend condition in S&P E-Minis remains bullish and the contract is trading at its latest highs. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. This was followed by a break of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a 1.236 projection of the May 23 - Jun 11 - 23 price swing. Key support is at the 50-day EMA, at 6064.44. First support lies at 6211.67, the 20-day EMA.

- A bull cycle in EUROSTOXX 50 futures remains in play and the latest pullback appears corrective. Recent gains have exposed key resistance and the bull trigger at 5486.00, the May 20 high. It has been pierced, a clear break of it would confirm a resumption of the medium-term bull cycle that began Apr 7 and open the 5500.00 handle. Support to watch lies at 5281.00, the low on Jul 1 and 4.

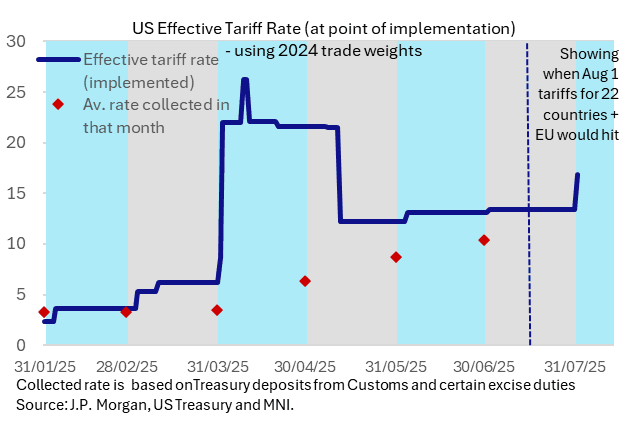

US OUTLOOK/OPINION: An Addendum To MNI US CPI Preview On Tariff Rates

Jul-15 09:46

- The below bullet is an addendum to the MNI US CPI Preview that was sent out yesterday (found here)

- It adds color to the section on the timing and magnitude of tariff hits, especially the remarks San Francisco Fed’s Daly made in a MNI webinar last week about the tariff collections data tracking below expected effective tariff rates.

- The static analysis takes effective tariff rates from J.P. Morgan calculations, in the chart below showing them at point of implementation rather than actual announcement, and compares them with average collection rates over the course of that month using US Treasury data for deposits from customs and certain excise duties.

- The latest message is similar to that from Daly: tariff collections data showed an average rate of ~10% in June after nearly 9% in May and 6% in April vs an effective rate of ~13% in June but one which could be 17% with new reciprocal tariffs slated for Aug 1; Daly referenced 8-9% collection rates vs an expected effective tariff rate of ~16%. The below also offers a useful look at how this has incrementally increased over time.

- It doesn’t however give insight into burden sharing across importers, businesses and consumers, something we go more into in the main preview.

GILTS: Firmer & Flatter, Mansion House Eyed After U.S. CPI

Jul-15 09:38

Core global FI markets have rallied this morning, curves flattening, pointing to lightening up of existing shorts & curve steepeners ahead of U.S. CPI data.

- Gilt futures +30 at 92.13 last, nearing initial resistance at 92.19, which protects the 20-day EMA (92.29). Bears remain in technical control.

- Yields 1-4bp lower, curve flatter.

- There hasn’t been much in the way of fresh headline cues, even alongside a burst of demand for bonds around the middle of the London morning.

- FT reports suggesting that U.S. President Trump privately encouraged Ukrainian President Zelenskyy to strike Moscow if possible (on July 4) provided some background support in more recent trade, although the bulk of the move happened before those headlines crossed.

- Elsewhere, the OBR reaffirmed that shifts in the bond buyer base and unexpected shocks present ongoing risks to the UK government bond market.

- This morning’s GBP1bln PGT of the 4.25% Jun-32 gilt was well received, with infrequency of primary supply and limited size helping generate solid demand and firm pricing metrics.

- BoE-dated OIS little changed on the day, showing ~57bp of cuts through year-end. A reminder that a particularly soft REC labour market report and dovish comments from BoE Governor Bailey resulted in dovish repricing on Monday.

- Note that Chancellor Reeves will appear twice today, more prominently this evening, at the Mansion House event. BoE Governor Bailey will also speak at that event (21:00).

- Meanwhile, CPI (Wednesday) and labour market (Thursday) data headline this week’s domestic calendar.