US STOCKS: Rotation To Other Sectors Continues

The ESU5 overnight range was 6235.50 - 6279.50, Asia is currently trading around 6277. A dip early on due to the UK fallout, but then normal business resumed with good demand on the dip and then new highs, the laggers continued to outperform as rotation to these sectors plays out, Russell 2000 +1.31%, Dow Transport +1.17%, Regional Banks +1.62%. These laggers are just starting to gain some momentum and this rotation could play out more in the short-term which would certainly help with the market breadth. This morning has seen US futures have a subdued open with the focus on the NFP out tonight, ESU5 +0.03%, NQU5 +0.03%.

- (Bloomberg) -- “The US stock market is expected to outperform European peers due to stronger earnings growth driven by AI adoption and investment. BlackRock predicts 6% US corporate earnings growth in Q2, compared to 2% in Europe, and expects the next US earnings cycle to ramp up this month. The firm views US stocks as a better investment than Treasuries.”

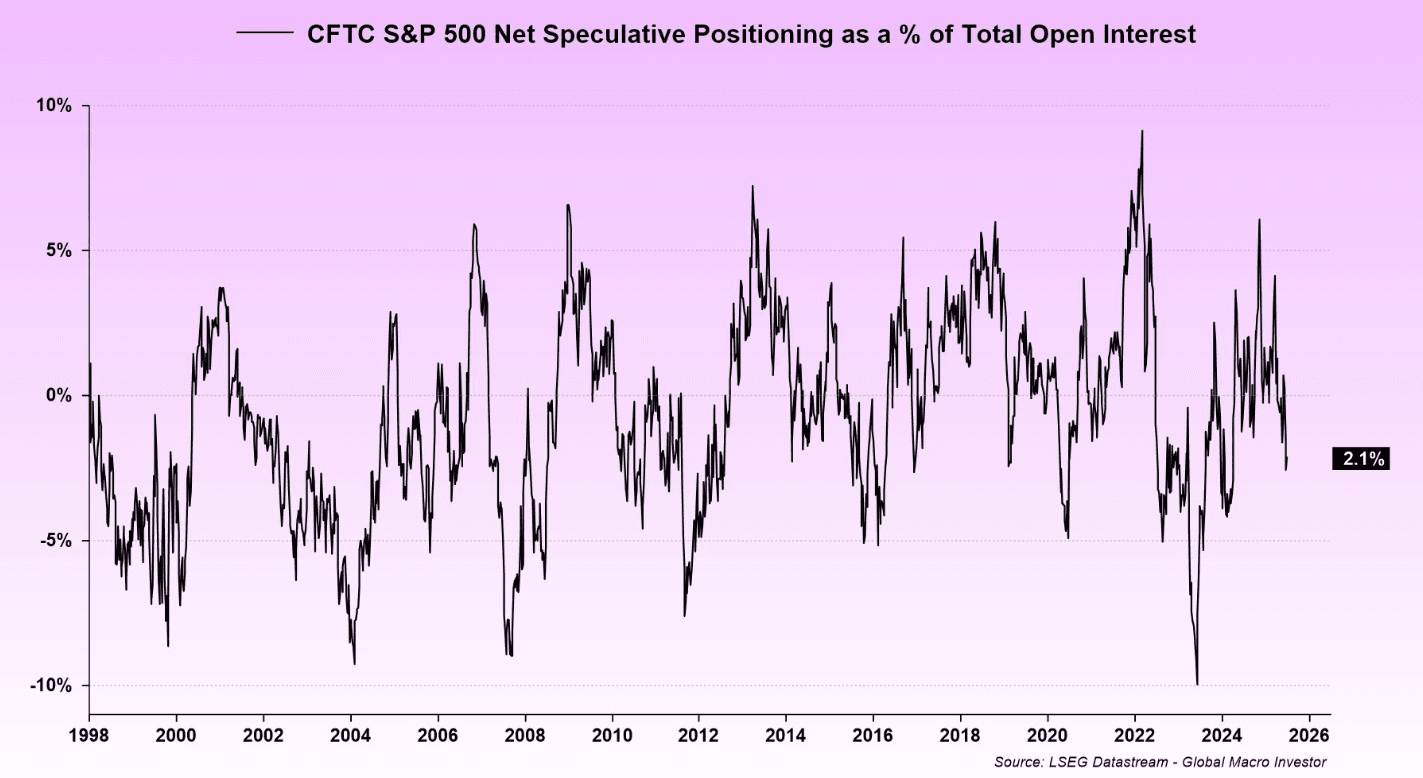

- Julien Bittel on X: “ The S&P 500 is up nearly 30% off the April lows and sitting at new all-time highs, while speculators have remained stubbornly short the entire time and are still betting against this rally. Classic pain trade setup…When everyone’s positioned wrong, the market tends to keep grinding higher – squeezing the shorts until max pain.” See Graph Below

- Guy LeBas on X: ”BMO Economics: Anecdata for June NFPs "skewed heavily to the downside" by 9:2”

- The market has been caught underweight and with momentum type funds(CTA’s) adding through all-time highs these reluctant PM’s are being forced to return to the market.

- Short-term this does look a little overdone but dips should find demand, first support is back towards the 6100 area.

Fig 1: CFTC S&P 500 Net Speculative Positioning

Source: MNI/@BittelJulien/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: Trades Heavy, The BBDXY Eyes The Pivotal 1200 Area

The BBDXY range overnight was 1208.17 - 1214.16, Asia is currently trading around 1209. Asia opens near the overnight lows, with the BBDXY eyeing the 1200 area. The price action in the USD stands out and has the feel it could begin to pick up momentum.

- (Bloomberg) - “After a synchronized fall since the start of the year, the dollar has languished even as stocks have rebounded on signs of de-escalation in the trade war and progress with President Donald Trump’s tax bill. Their newly found positive correlation, however, suggests that either equities will fall to match the dollar, or resilience in the US economy will lift the greenback.”

- “The trade war has upended traditional macro relationships, including the one between stocks and the dollar, which are typically negatively correlated. However, the emergence of the “Sell America” trade means they’re now moving more in sync than before.”

- “The dollar will face its next big test Friday with the release of the May jobs report -- a hot report could slow its cyclical slide, but a weak one could pressure it further.”(BBG)

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. The US trade war has degraded the worlds view of the US and whether the USD is actually a safe haven any longer.

- The market is still clearly focused on the “sell America” trade. What last week’s price action highlighted is the short-term market is all the same way so the frequency of sharp pullbacks will increase.

- The BBDXY rejected the 1125 area pretty strongly, the USD should continue to be met with supply should this 1225/30 area cap price.

- We are approaching some key Weekly support towards the 1200 area in the BBDXY. A break below here could signal the move is about to accelerate. The price action has been particularly dire for the USD and does allude to further losses.

Data/Events : Factory Orders, Durable Goods Orders, JOLTS

Fig 1: BBDXY Weekly Chart

Source: MNI - Market News/Bloomberg

JGBS: Modest Twist-Flattener Ahead Of 10Y Supply

In Tokyo morning trade, JGB futures are weaker, -12 compared to settlement levels.

- Japan’s monetary base fell 3.4 per cent in May from a year ago.

- BoJ Governor Ueda is scheduled to appear in Parliament at 1000 JT.

- “The Bank of Japan will likely decide to stop reducing the amount of its government bond purchases in a plan for the next fiscal year. The bank has been reducing its buying of government bonds by ¥400 billion every quarter since last summer, but that process will come to a halt.” (per BBG)

- Cash US tsys are flat to 1bp richer, with a steepening bias, in today’s Asia-Pac session after yesterday’s sell-off.

- Cash JGBs are 1bp cheaper to 2bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 0.4bps higher at 1.517% ahead of today’s supply.

- “The bond market is likely to stay weak following the rise in US Treasury yields and position adjustments ahead of the 10-year auction, said Ataru Okumura, a senior interest-rate strategist at SMBC Nikko Securities.” (per BBG)

- Swap rates are slightly mixed, with a flatter curve. Swap spreads are mixed.

AUSTRALIA: Minimum Wage To Rise 3.5%, Unlikely To Concern RBA

The Fair Work Commission has announced that the hourly minimum wage will be increased 3.5% to $24.94 on July 1 after 3.75% in 2024, bringing it to 25.7% above the 2020 level. Q1 wages rose 3.4% y/y while headline CPI was 2.4% y/y and the trimmed mean 2.9%, thus the rise amounts to a real wage increase. The increase will directly impact about 0.7% of workers but with around 20% on award wages, the indirect effect could be larger. The decision will not concern the RBA as it will continue to monitor economy-wide wage growth relative to productivity, which has been lacklustre (Q4 -1.2% y/y). There will be an update on the latter and average compensation per employee in Wednesday’s Q1 national accounts.