BOJ: Rinban Purchase Offer

The BoJ offers to buy a total of Y1.075tn of JGBs from the market:

- Y425bn worth of JGBs with 1-3 Years until maturity

- Y450bn worth of JGBs with 3-5 Years until maturity

- Y200bn worth of JGBs with 10-25 Years until maturity

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOJ: Fixed Rate Purchase Offer

The BoJ offers to buy an unlimited amount of 5- to 10-Year JGBs at a fixed rate of 0.50%.

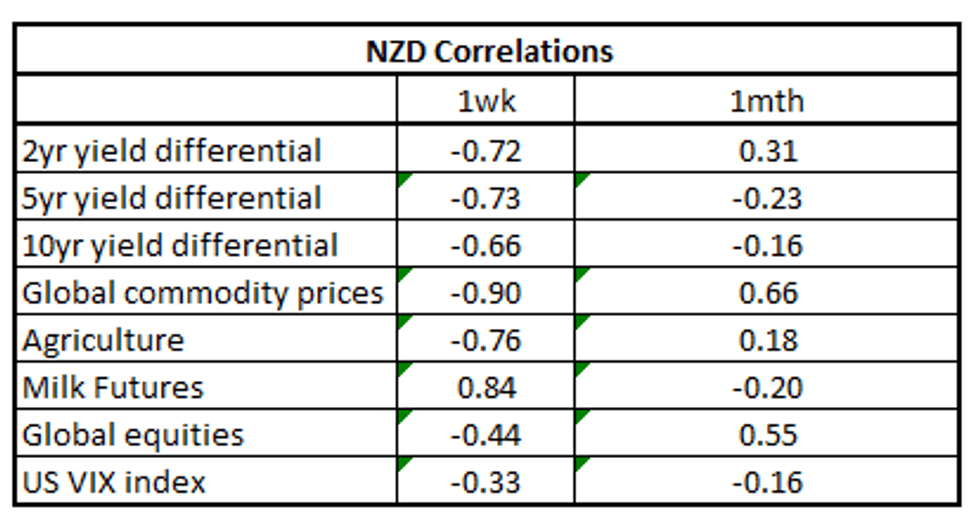

NZD: Milk Futures Dominant Driver Last Week

NZD/USD correlations with Milk Futures have strengthened over the past week, standing out as a key macro driver in recent dealings. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- Last week's weakness in NZD/USD looks to be associated with falling milk futures prices. NZD/USD fell ~3%, its biggest weekly fall since late May.

- The pair looked through widening rate differentials as well as strength in Global Commodity prices.

- Over the longer time frame Global Commodity prices and global equities stand out as the dominant drivers.

Fig 1: NZD/USD Correlation with Global Macro Drivers:

Source: MNI/Bloomberg

JGBS: Futures Pare Gains In Early Tokyo Trade, BoJ Policy Meeting On Friday

JGB futures are stronger, +45 compared to settlement levels, but below the post-Tokyo closing level ahead of the weekend. At 148.23, JBU3 sits 51 points below Friday’s overnight high of 148.74.

- According to MNI’s technicals team, the sharp rally on Friday reaffirms the buy-on-dips theme in markets at present. Moves continue to mirror near-term strength in US bond markets following the soft CPI, helping keep the upside impetus intact for now. Key resistance lies ahead at 149.21/53, highs from May and March. Clearance of these levels would highlight an important break.

- Preliminary PMI prints for July were reasonably close to June outcomes. The Jibun Bank manufacturing PMI edged back to 49.4 from 49.8, while the services slipped to 53.9 from 54.0. This still left the composite PMI unchanged at 52.1 for the month. Later today see Department Store Sales data.

- Cash JGBs are mixed in early Tokyo trading with the futures-linked 7-year zone outperforming (2.0bp richer). The benchmark 10-year yield is 1.2bp higher at 0.462%, below BoJ's YCC limit of 0.50%. The 40-year zone is 0.9bp lower at 1.491% ahead of tomorrow’s supply.

- The swap curve has bear steepened with rates 0.1bp to 3.1bp higher. Swap spreads are wider across the curve.