SOUTH KOREA: Retail Sales Up (amended)

Jul-30 02:11

- June's retail sales data painted a different picture to the very strong consumer confidence index released earlier this month.

Retail Sales YoY for June rose +7.3%, from 7.0% in May to remain below the 3-year average.

- Department store sales actually declined -0.9% YoY from the May expansion of +2.3% YoY.

- Discount Store Sales YoY also declined, down -2.8% YoY from May's result of +0.2%.

- July's consumer confidence rose to the highest level in seven years suggesting that the consumer is finding confidence given the rate cuts, new government and stable currency.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

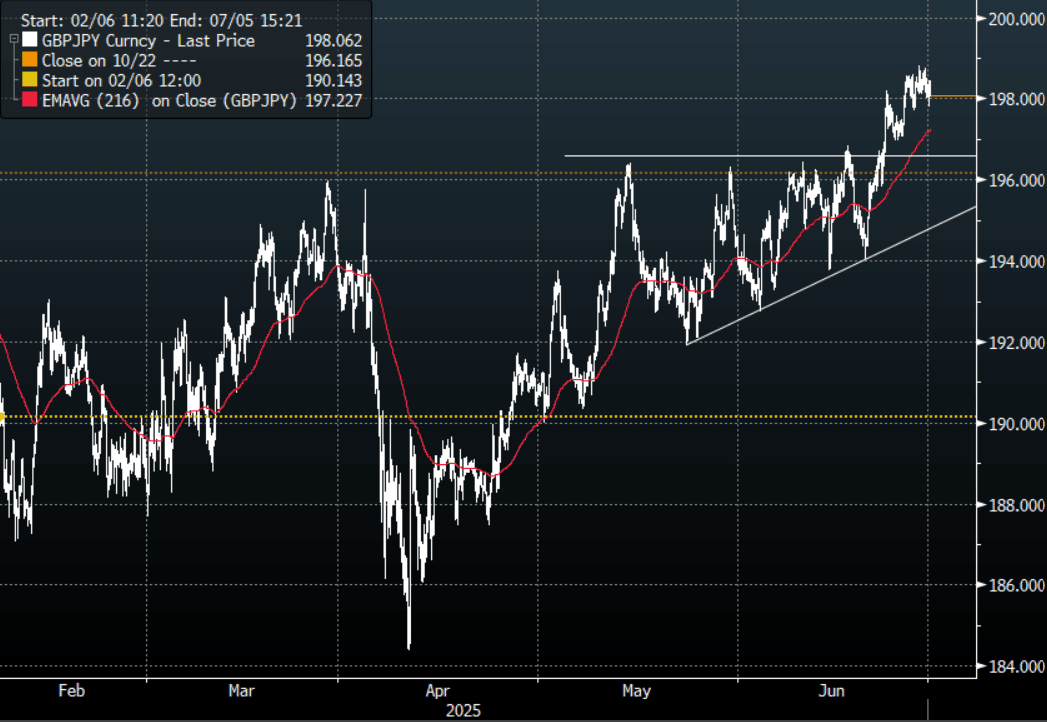

FOREX: JPY Crosses - JPY Continues To Underperform Against EUR & GBP

Jun-30 01:51

The JPY performance has been mixed in the crosses, struggling against the EUR and GBP but holding steady against the AUD and NZD. It continues to perform best against the CNH.

- EUR/JPY - Friday night range 168.77 - 169.81, Asia is trading around 169.25. The dips in this have been very well supported recently, with good upward momentum. First support is back towards the 167.50 area, and is currently eyeing a move back above 170.00.

- GBP/JPY - Friday night range 198.02 - 198.75, Asia trades around 198.05. Considering the pullback in USD/JPY cross-JPY remains well supported. Look for dips to remain supported in the short-term, first support is back towards the 196.50 area. The focus is now turning back to the 200.00 area.

- NZD/JPY - Friday night range 87.41 - 87.81, Asia is currently dealing 87.65. NZD/JPY again found decent supply back towards the 88.00 area, a sustained break above here is needed for the market to turn its focus back to the 90.00 area.

- CNH/JPY - Friday night range 20.1248 - 20.2016 Asia is currently trading around 20.1450. A big reversal from the 20.50/20.60 resistance area. In the middle of its recent range awaiting clearer direction.

Fig 1 : GBP/JPY Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Holding Cheaper, Subdued Session

Jun-30 01:47

ACGBs (YM -3.0 & XM -4.5) are holding weaker after a subdued Sydney morning session.

- Private credit rose 0.5% m/m (estimate +0.6%) in May versus +0.7% in April.

- Melbourne Institute inflation index rose 0.1% m/m in June versus -0.4% in May. Inflation index rose 2.4% y/y versus +2.6% in May.

- (Dow Jones) Recent turmoil in global financial markets is fueling overseas demand for New South Wales state government bonds, despite concern about a rise in public-sector debt levels in Australia.

- Cash US tsys are slightly mixed, with a steepening, in today's Asia-Pac session after Friday's modest losses.

- Cash ACGBs are 3-5bps cheaper with the AU-US 10-year yield differential at -10bps.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 94% probability, with a cumulative 81bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- This week, the AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Wednesday and A$1000mn of the 2.25% 21 May 2028 bond on Friday.

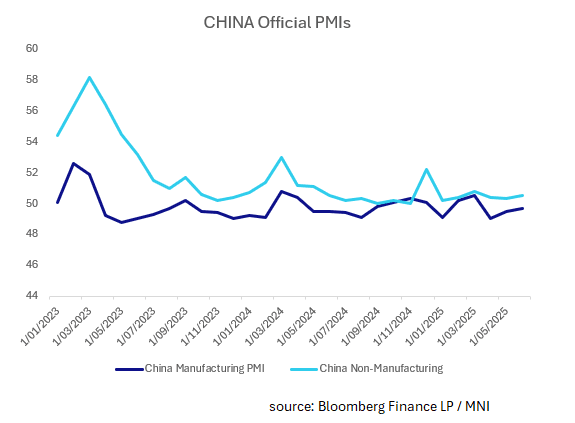

CHINA: Official PMIs for June

Jun-30 01:42

- The Official PMIs followed the familiar theme of recent releases with the PMI manufacturing in mild contraction and the PMI non-manufacturing barely holding in expansion.

- The PMI Manufacturing print of +49.7 was the third successive print below 50. Output and New orders rose relative to last month whilst employment declined.

- The PMI Non-manufacturing print of 50.5 was a modest improvement on last month's release of 50.3 whist New orders up whilst employment was down.

- This is the first full month of data since the agreement between Beijing and Washington to a halt to the trade war.