CANADA DATA: Retail Sales Have Limited Momentum, But Not Off A Cliff Into Q2

Retail sales held up in March despite a pullback in consumer sentiment amid then US-Canada trade conflict. Headline sales rose 0.8% M/M SA survey (+0.8%, -0.5% prior rev from -0.5%), with ex-auto/gas sales up 0.2% (0.6% prior). Ex-auto sales alone were down 0.7% M/M (-0.1% survey, +0.6% prior), with sales of gas plummeting 6.5% M/M.

- Sales rose in 6 of 9 subsectors, with motor vehicle and parts dealers sales soaring +4.8% for the first gain in 3 months. As our Policy team noted, "Big-ticket spending led March increase with new cars +5.2%. Unclear if consumers wanted to buy before any potential tariffs on autos or a sign of unexpected confidence. Sales also grew for furniture, electronics and appliances."

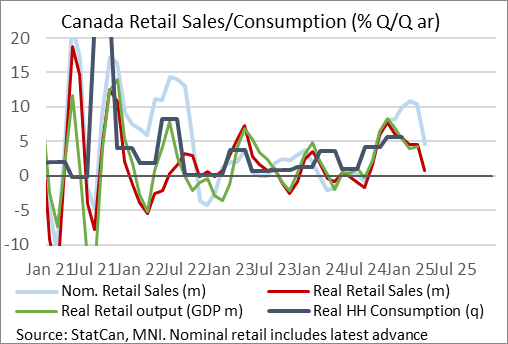

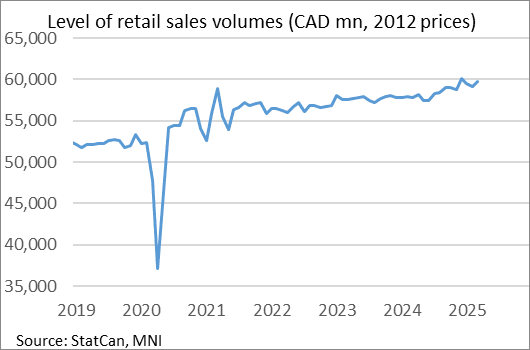

- On a price-adjusted basis, volumes rose 0.9% M/M after two consecutive months of contraction, leaving them below levels seen at end-2024 albeit at all-time highs outside of that.

- In other words, despite a sharp slowdown in momentum in January-February, the 3M/3M annualized rates of growth slowed but remained positive by the end of the quarter (4.7% nominal, 0.8% real).

- StatCan's advance estimate of retail sales for April is for 0.5% nominal M/M growth, suggesting that while the labor market and confidence remained soft at the start of Q2, consumer demand hasn't fallen off a cliff.

- On the margin then the retail sales release reduces the impetus for a BoC cut in June (market-implied probability slipped today to around 22% from 26%, and versus close to 65% pre- this week's CPI.

- Next week we get multiple key data points ahead of that decision, with advance April manufacturing sales data on Monday and early April wholesale sales on Tuesday, with Friday bringing Q1 GDP (1.8% consensus and BoC estimate) but also the March and prelim April GDP estimates eyed for momentum at the start of Q2.

- BOC Gov Macklem noted Thursday re GDP "I expect the second quarter will be quite a bit weaker" as a consequence of pulling forward exports and inventory accumulation. The BOC's more benign (of two) scenario for Q2 sees 0.0% growth, with the more negative scenario -1.3%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Late Equities Roundup: Trade Wards Aren't an Easy Win

- Stocks hold decently positive levels in late Wednesday trade - but well off this morning's knee-jerk rally as Treasury Sec Bessent through cold water on trade hopes, clarifying there is no unilateral offer from Trump to cut China tariffs, and that a full China trade deal could take two-to-three years.

- Currently, the DJIA trades up 426.52 points (1.09%) at 39608.04 (40,376 high), S&P E-Minis up 95 points (1.79%) at 5409.5 (5499.75 high), Nasdaq up 465.6 points (2.9%) at 16762.93 (17029.86 high).

- Consumer Discretionary and Information Technology sectors continued to outperform in late trade, leading gainers included Super Micro Computer +10.89%, Amphenol +10.39%, Palantir Technologies +9.00%, Dell Technologies +7.62%, Monolithic Power Systems +7.06% and Advanced Micro Devices +6.82%. Meanwhile, Tesla rallied 8.41% while Amazon gained 4.93%.

- Conversely, a mix of Consumer Staples, Energy and Real Estate sector shares continued to underperform: Enphase Energy -14.62%, Lennox International I-8.10%, American Tower -4.92%, SBA Communications -4.36%, Teledyne Technologies -3.54%, General Dynamics-3.46% and Bristol-Myers Squibb -2.99%.

- Meanwhile, a heavy earnings docket resumes after the close with the following reporting: Whirlpool Corp, Chipotle Mexican Grill, O'Reilly Automotive, Raymond James Financial, Molina Healthcare Alaska Air, Discover Financial Services, Rollins Inc, Newmont Corp, ServiceNow Inc, FirstEnergy Corp, Lam Research Corp, Texas Instruments Inc, Community Health Systems, IBM, United Rentals, Edwards Lifesciences, Viiking Therapeutics and Las Vegas Sands.

JPY: USDJPY Session Highs As US Doesn't Eye FX Rate Targets

With Tsy Sec Bessent confirming to reporters that the US wouldn't require specific exchange rate targets for the yen in US-Japan trade talks ("absolutely no currency targets", Bessent is quoted as saying, per multiple wires), USDJPY has moved through the session high of 143.22 and now 1.3% higher on the session. Bessent had made similar comments earlier in the day in an interview with Nikkei and other media.

- The trend condition in USDJPY remains bearish and the bounce from Tuesday’s low (139.89) is considered corrective.

- That said, at the highest level since April 14 (last 141.49), Initial firm resistance identified by our tech analyst to watch is the 20-day EMA, at 144.90, about another 1% move from here.

COMMODITIES: Pullback In Gold Extends Further, WTI Crude Declines

- Spot gold has fallen by a further 3.0% today to $3,280/oz, taking the pullback from yesterday's $3,500.1 all-time high to over 6%.

- The WSJ's latest article on possible Chinese tariff rollbacks provided the latest source of pressure, coming after market fears had already been calmed somewhat as President Trump softened his stance on Fed Chair Powell.

- The pullback in gold has allowed an overbought condition to unwind, with gold piercing initial support at the April 17 low of $3,284.0. Firm support is seen at the 20-day EMA of $3,193.5. Shallower selloffs will be considered corrective at this stage.

- A dominant uptrend remains intact, however, with moving average studies firmly in a bull-mode setup. Initial resistance is at $3,500.1, the Apr 22 high.

- Meanwhile, crude has fallen in a volatile trading session, with the main bearish driver a Reuters report that some OPEC+ members are pushing for another accelerated supply return in June.

- Earlier signs that the US may ease its tariffs on China were briefly supportive.

- WTI Jun 25 is down by 2.1% at $62.4/bbl.

- Recent weakness in WTI futures has resulted in the breach of a number of important support levels, reinforcing a bearish threat. Initial support is seen at $58.29, the Apr 10 low, followed by $54.67, the Apr 9 low and bear trigger.

- Resistance is seen at $64.49, the Mar 5 low.