US TSYS: Repo Reference Rates

Sep-16 12:11

- Secured Overnight Financing Rate (SOFR): 2.28%, $981B

- Broad General Collateral Rate (BGCR): 2.26%, $407B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $383B

- (rate, volume levels reflect prior session)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

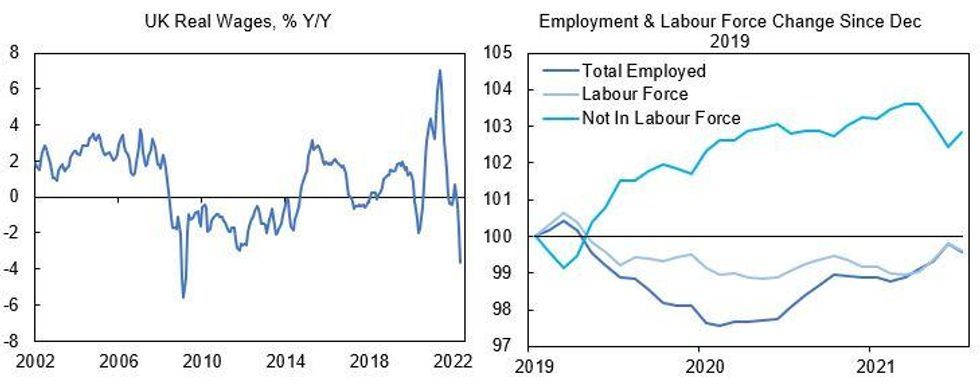

UK: Stresses Intensifying On Economic Lynch Pin #2

Aug-17 12:10

While UK wages have started to respond to the higher cost of living, the magnitude of second-round effects has been limited thus far.

- In the first chart below we have deflated average weekly wages by the UK CPI and transformed to a Y/Y series. Real wage growth has collapsed and is returning to 2009 levels.

- Continued job gains are eroding space capacity, although the growing population of inactive workers (outside of the labour force) has been the main factor behind the tightening labor market. Indeed, while the economically active population has increased by 0.76% since December 2019, employment has contributed -0.27pp (total employment is still below pre-pandemic levels) while the stock of workers outside of the labour force has contributed 1.03pp.

- Even with the labour market still tightening, concerns about the economic outlook are being well-telegraphed (not least by the BoE's own particularly gloomy assessment at the August MPC meeting) and could work against wage negotiations when job security starts to trump maintaining purchasing power.

- A persistent squeeze on real incomes, heading into another surge in household energy bills, would require spending down savings or liquidating assets in order to maintain consumption, otherwise household spending would need to adjust lower.

MARKET INSIGHT: What to Watch: July FOMC Minutes, Retail Sales, 20Y Bond Sale

Aug-17 12:06

Tsys futures under pressure, extending overnight lows last few minutes after initial selloff on jump in UK CPI (+0.6% MoM; +10.1 YoY) renews rate hike expectations. Yield curves steepening (2s10s +1.004 at -45.157, but off -42.169 high) as expectations for additional hikes climb (rate cut hopes for late 2023 evaporating).

- Markets looking toward this afternoon's July FOMC minutes release at 1400ET for voting member guidance mindset.

- Upcoming data at 0830ET:

- Retail Sales Advance MoM (1.0%, 0.1%); Ex Auto MoM (1.0, -0.1%)

- Ex Auto and Gas (0.7%, 0.4%); Control Group (0.8%, 0.6%) followed by:

- Business Inventories (1.4%, 1.4%) at 1000ET

- Fed speakers: Double billing from Fed Gov Bowman today:

- On tech/innovation financial services, text, Q&A, livestreamed at 0930ET; and again at 1420ET at Arkansas Women's Comm meeting, also livestreamed.

- Treasury auctions:

- $30B 119D bill CMB auction at 1130ET

- $15B 20Y Bond (912810TK4) at 1300ET.

- Equity earnings: Stocks weaker (ESU2 -36.25 at 4271.5) part on extended rate hike pricing and after Target (TGT) earnings miss (irony) -$0.39 vs. $0.725 est. Meanwhile, Lowe's Group (LOW) beat: $4.67 vs $4.611 est; Analog Devices (ADI) beat: $2.52 vs. $2.442 est.

- After the close: Synopsys (SNPS) $2.038 est; Cisco (CSCO) $0.816 est; Bath and Body Works (BBBI) $0.446 est.

US: MNI POLITICAL RISK - US Daily Brief

Aug-17 11:57

- President Biden returned from his summer holiday to sign the Inflation Reduction Act into law at the White House yesterday.

- Two of former President Donald Trump’s key White House legal councils have been interviewed by the FBI as the fallout continues from the search of Mar-a-Lago.

- Rep Liz Cheney (R-WY) lost her primary election in a landslide but her new political career may just be beginning.

- With Cheney gone, the bloc of GOP House Reps in Congress who voted to impeach Trump has shrunk to two.

- China’s ambassador to the US, Qin Gang has indicated that Beijing is not prepared to step away from aggressive force posture in the Taiwan Strait.

- The US and the EU have received the final comments from Iran on the EU proposal for the restoration of the Joint Comprehensive Plan of Action nuclear accords but a positive outcome remains uncertain.

- Poll of the Day: Voter anger may be an additional metric to consider ahead of November’s midterms.

Full Article: https://marketnews.com/mni-political-risk-analysis...