GERMAN DATA: Q1 GDP Shows Higher Net Exports, Lower Inventories

May-22 07:28

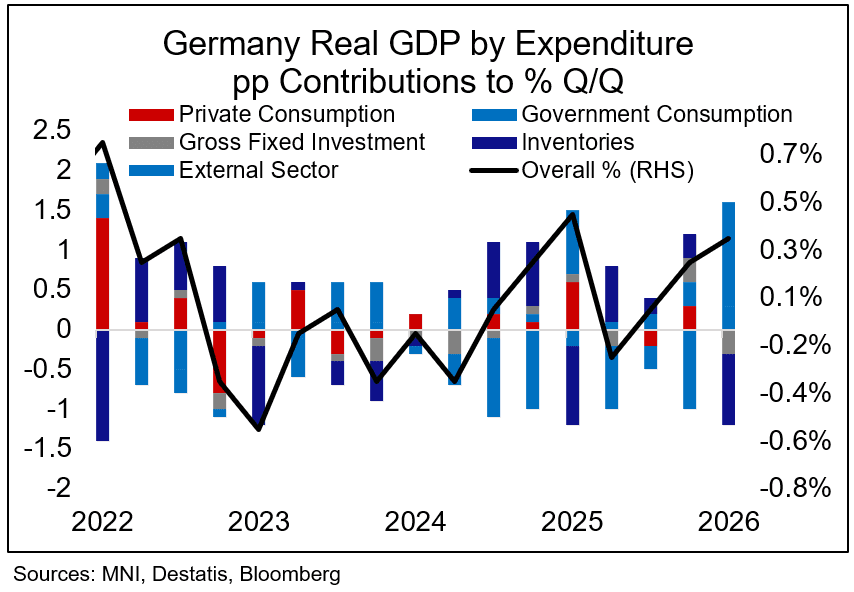

German Q1 GDP by expenditure (unrevised from flash at 0.3% Q/Q) is highlighted by a weak domestic demand figure of -0.9% Q/Q which would be even worse had it not been for government spending. Details:

- Private consumption unchanged at 0.0% Q/Q (0.2% cons, 0.6% prior, revised from 0.5%). Lower than expected after Destatis mentioned the category as a positive driver in the first release of Q1 GDP (which only included a short qualitative comment and no full expenditure split).

- Government spending 1.1% Q/Q (no cons, 1.5% prior, revised from 1.1%): Highlighting that the government's fiscal push is filtering through to the national accounts this year. Central government fiscal data yesterday showed deficits are roughly on track for FY targets into April.

- Private investment -1.5% (-0.1% cons, 1.3% prior, revised from 1.0%): Reverses the strong Q1, and likely represents the most worrying part of German GDP by expenditure in recent quarters. Inventories contributed a firmly negative 0.9pp to sequential GDP, the "lowest" contribution since Q1 2025.

- Net exports contributed 1.3pp to GDP in Q1 as exports increased 3.3% Q/Q (-1.5% Q4) while imports declined 0.1% (+1.0% Q4). In conjunction with lower inventories, one interpretation of this could be that firms ran down existing stocks to fulfil export orders rather than producing new inventory.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Latest notable Option trade

Apr-22 07:25

- ERK6 97.62/97.75/97.870c fly, bought for 4.75 in 4k.

- ERU6 97.68/97.81 cs x2 vs 97.31p x1, bought the cs for -2.5 in 5k (10k x 5k).

- ERZ6 97.62/97.75/97.875/98.0625c condor, bought for 2.5 in 8k.

GILTS: A Little Firmer On As Oil Ticks Lower & CPI Broadly Matches Expectations

Apr-22 07:23

Gilts rally alongside oil lower prices after President Trump provided an indefinite extension of the ceasefire with Iran. Iranian media reports noting that the country sees some signs that the U.S. could be ready to undo its blockade of the Strait of Hormuz also plays into the move in oil.

- Gilt futures trade as high as 88.08 before backing off to 87.95.

- Note that yesterday’s break of support (87.82) deepened bearish technical control, with moving average studies underscoring that technical theme.

- A break of yesterday’s low (87.67) would expose key support at the April 7 base (87.59). Meanwhile, bulls need to break the April 17 top (89.42) to start turning the technical picture a little more in their favour.

- Yields 1-2bp lower across the curve.

- 2s10s back to ~60bp after failing to close above 65bp during the recent steepening, while 5s30s pulls back to 120bp after failing to close above 125bp.

- Little impetus from the UK inflation data, which our macro team noted was pretty close to expectations, so isn't going to have huge implications for policy. If anything, the lack of meaningful upside surprise in the headline & core CPI readings may be factoring into the dovish GBP STIR adjustments at the margin, given the situation surrounding the Middle East and focus on upside inflation risks.

- On the fiscal front, the Resolution Foundation noted that further deterioration in the Middle East conflict could eliminate GBP16bln of the UK government's fiscal headroom in 2029-30.

- BoE’s Breeden will speak this morning, although that will be on “clarifying private credit’s impact on systemic stability”.

OPTIONS: Expiries for Apr22 NY cut 1000ET (Source DTCC)

Apr-22 07:17

- EUR/USD: $1.1580-85(E906mln), $1.1750-70(E2.9bln), $1.1800-05(E1.5bln), $1.1850(E2.9bln)

- GBP/USD: $1.3250(Gbp777mln)

- USD/JPY: Y158.00($867mln), Y158.35($573mln), Y158.70($527mln), Y160.00($626mln)

- AUD/USD: $0.6670(A$1.5bln)

- NZD/USD: $0.5560(N$1.1bln)