USDJPY TECHS: Pullback Considered Corrective

Jul-03 18:30

* RES 4: 163.70 Top of a bull channel drawn from Feb 12 low * RES 3: 163.62 2.000 proj of the Jan 27...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

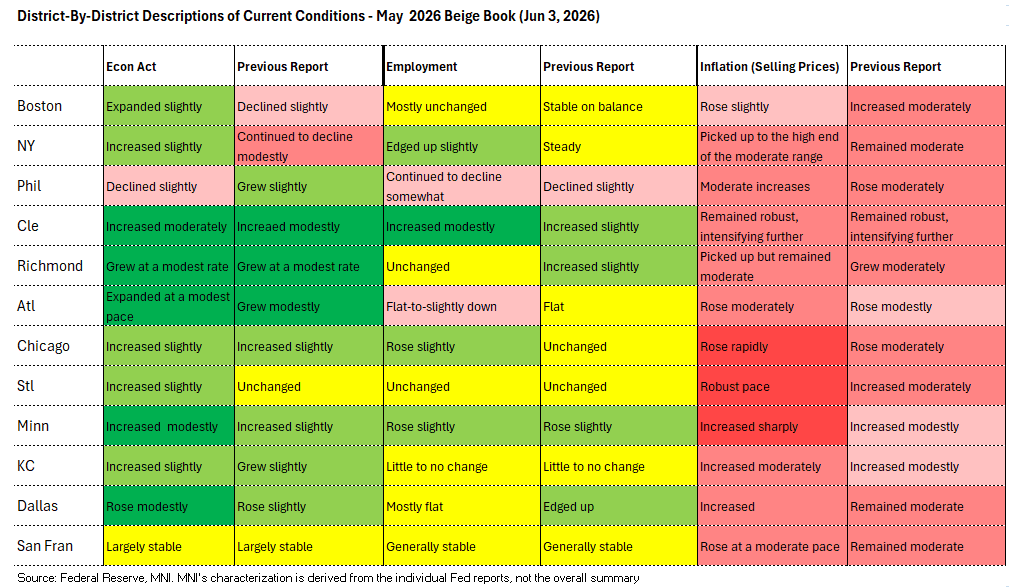

FED: May Beige Book: Broadly Stronger Economic Growth Across Districts (1/3)

Jun-03 18:15

The Fed's May Beige Book portrays a US economy that is experiencing stronger growth, steady labor markets on balance, and mounting price pressures compared with the period covered by the previous edition in April.

- Only one of the 12 Fed districts (Philadelphia) reported declining economic activity ("slightly") in the latest period, compared with two in the previous (April) Beige Book (Boston and New York). One (San Francisco) reported "largely stable" growth, vs two in April's.

- All told, of the 10 districts reporting expansion, 5 saw improved conditions vs April's report; Philadelphia was the only district to see a deterioration.

- From the Beige Book's description of national consumer conditions: "Consumer spending remained mixed across Districts and increasingly bifurcated across income groups amid affordability pressures. Higher-income households remained resilient and less sensitive to price increase, while middle-income households were described as "squeezing more life out of every dollar before deciding to spend it," and low-income consumers showed greater financial strain. Overall, there were reports of increased credit card usage, fewer retail visits, and stronger demand for necessities. Auto dealers reported softer new vehicle demand tied to affordability and fuel costs, alongside substitution toward used and hybrid vehicles."

- Manufacturing appeared to be a strong point though uncertainty appeared to weigh on the forward-looking outlook: "By contrast, manufacturing activity increased at a modest to strong pace for nine of the Districts and only one noted a slight decline from the previous period. Banking conditions were stable across most Districts; however, residential mortgages, consumer, and agricultural loan delinquencies were noted as rising in several of the Districts. Agriculture conditions were unchanged or declined for most of the Districts, with cost pressures intensifying from fuel and fertilizer spikes. Energy activity increased in two of the markets, but Districts reported that the outlook remains highly uncertain leading producers to hold off on materially expanding activity. More broadly, business outlooks for the next six months were reported to have little change in anticipated growth, as elevated uncertainty and signs of weakening consumer spending weighed on sentiment."

US TSYS: Post-Fed Beige Book React

Jun-03 18:15

- Treasuries remain weaker - off midday lows - little if any reaction to the latest Fed Beige Book survey of economic conditions. Markets continue to digest the data that showed most districts saw increased inflation than in the prior period.

- TYU6 trades -7.5 at 109-15 vs. 109-11.5 low. initial technical support well below at 108-28.5 (Low May 22). The recovery since May 19 appears corrective and the medium-term trend condition remains bearish. Note that the recovery has allowed a recent oversold trend condition to unwind.

- The next resistance to watch is 110-09, the 50-day EMA. The bear trigger lies at 108-08+, the May 19 low. A breach of this level would confirm a resumption of the downtrend.

- Cross asset update: Bbg US$ index extends session high (BBDXY +3.93 at 1205.63), crude elevated (WTI +2.18 at 95.94), stocks weaker but off lows (SPX emini -43.5 at 7580.5).

- Focus remains on increased Middle East tensions and tenuous/opaque negotiations.

- Look ahead: Thursday Data Calendar: Weekly Claims, Challenger Jobs, Fed Speak

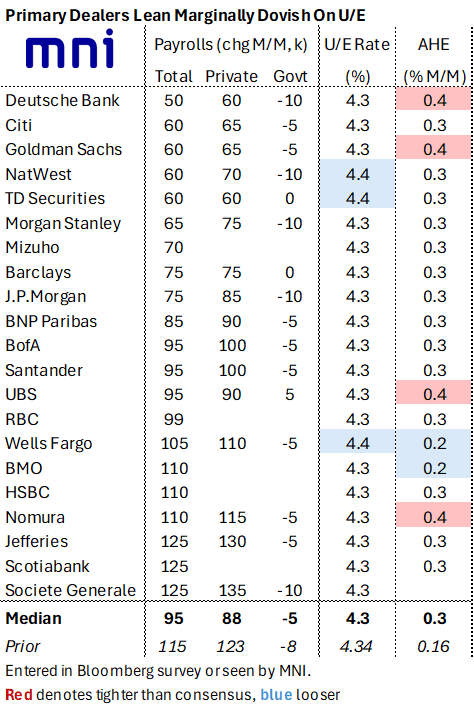

US LABOR MARKET: A Tighter Range To Primary Dealer Analyst Estimates For NFPs

Jun-03 18:05

- MNI’s survey of primary dealers shows a median expectation of 95k for nonfarm payrolls growth in May, a little stronger than the 85k currently seen for nonfarm payrolls.

- There’s a narrower range to estimates this month, from 50k-125k vs -15k to 135k in April.

- Highlighting the extent of the past two upside surprises, only Jefferies had a higher estimate than the realized 115k in April whilst the 178k initially reported for March (since revised to 185k) was higher than every primary dealer analyst.

- Back to May estimates, primary dealers may be more optimistic than broader consensus for nonfarm payrolls growth but they’re in line on private payrolls at 88k vs 87k for broader consensus.

- The unemployment rate is widely expected to round to 4.3% again, with a surprisingly small dovish skew to a 4.4% print considering it was 4.34% in April.

- There’s also relatively little divergence around the median expectation of a 0.3% M/M increase in AHE.

- See supporting comments behind these analyst estimates in the full MNI US Payrolls Preview, here.