OUTLOOK: Price Signal Summary - Fresh S&P E-Minis Cycle High

Sep-10 10:29

- In the equity space, a bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract has traded to a fresh cycle high today, breaching the Sep 5 high of 6541.75. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on the 6600.00 handle next. Initial support to watch is 64262.58, the 20-day EMA.

- A corrective bear cycle in EUROSTOXX 50 futures remains in play. Recent weakness resulted in a breach of 5369.17, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development. A stronger reversal would open 5445.00, the Aug 26 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

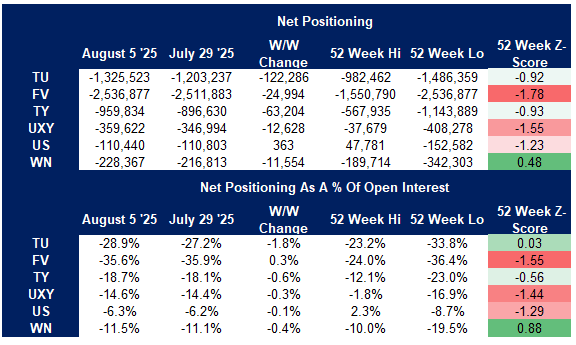

US TSY FUTURES: Swings In Long End Positioning Dominate Latest CFTC CoT

Aug-11 10:21

While headline adjustments in the latest CFTC CoT report pointed to extensions of existing positioning biases across asset managers, leveraged funds and non-commercial accounts, closer inspection revealed some nuances in the week ending August 5.

- Asset managers added ~$8.5mn DV01 equivalent of net longs across the curve, although ~$7.6mn of that came in WN futures alone. Elsewhere, net long setting in TU & TY futures was marginally more prominent than net long cover in FV, UXY & US futures. The cohort remains net long across the curve.

- Similarly, leveraged funds added ~$7.6mn DV01 equivalent of net shorts across the curve, with $8.2mln of fresh net shorts added in WN futures alone. Elsewhere, net short cover in FV & US futures proved slightly more sizeable than net short setting in TU, TY & UXY futures. The cohort remains net short across the curve.

- Wider non-commercial accounts added to existing net shorts in all contracts outside of US futures, where net positioning was essentially neutral. The cohort remains net short across the curve. See table below for greater details on net positioning swings for non-commercials.

Source: MNI - Market News/Bloomberg Finance L.P.

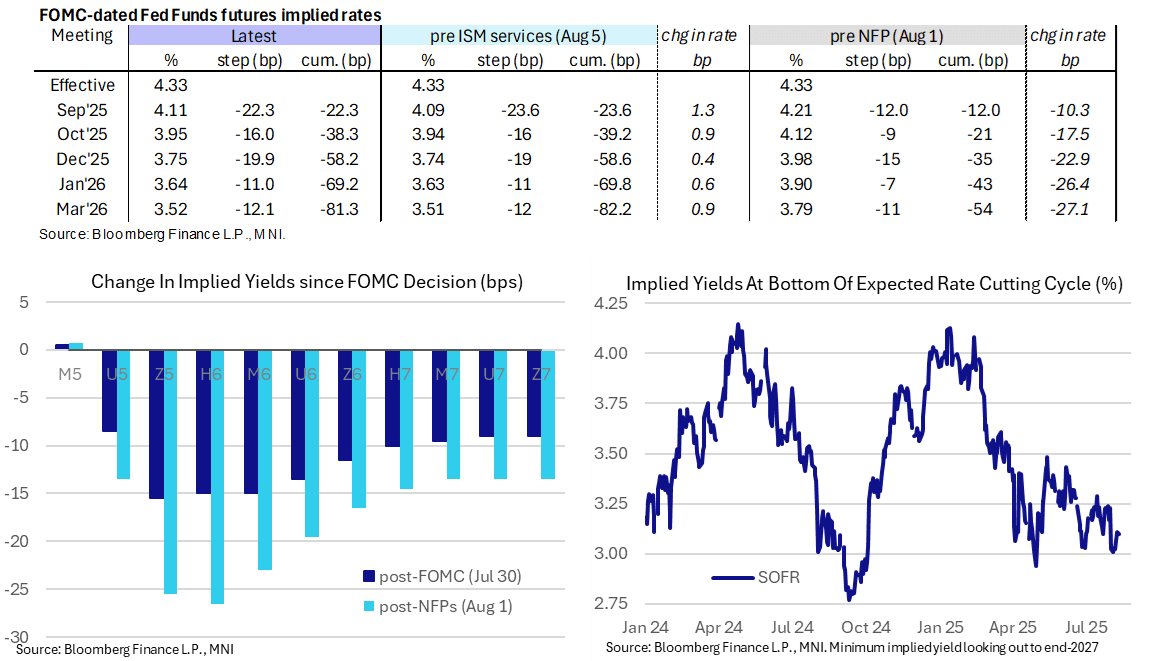

STIR: Fed Rate Path Treading Water With Tomorrow’s CPI Eyed

Aug-11 10:20

- Fed Funds implied rates for near-term meetings hold Friday’s drift higher ahead of a particularly thin docket with focus firmly on tomorrow’s CPI report.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 38.5bp Oct, 58bp Dec, 69bp Jan and 81.5bp Mar.

- The SOFR implied terminal yield of 3.10% (SFRH7) is 1bp lower after Friday’s 3.11% marked the highest since the July NFP report. It has recently ticked to just under five cuts priced from current levels.

- There is no notable data or Fedspeak scheduled today. Barkin (non-voter) and Schmid (’25 voter, hawk) are next of the scheduled FOMC speakers, both coming after CPI tomorrow.

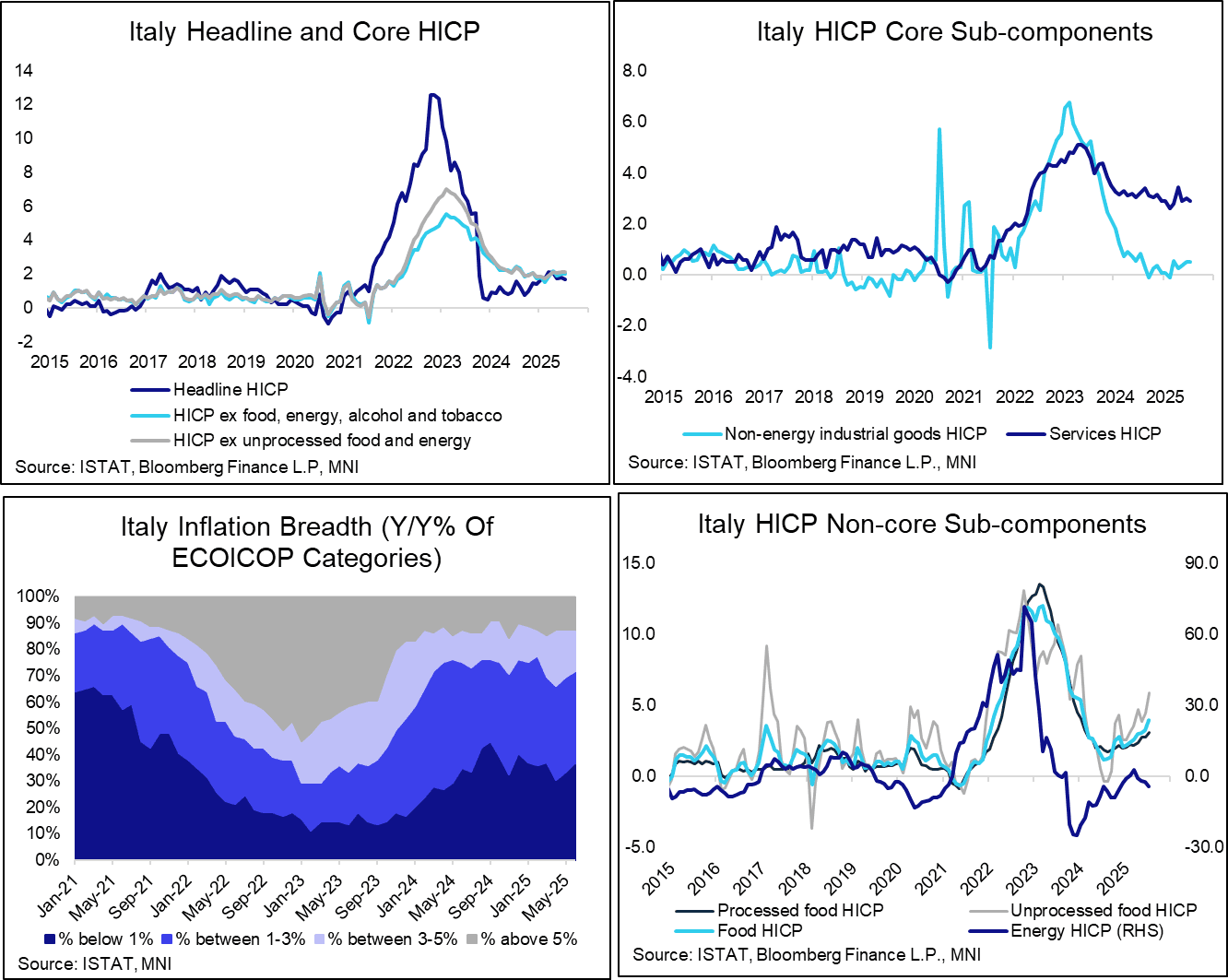

EUROPEAN INFLATION: Italy July Headline and Core HICP Confirm Flash Estimates

Aug-11 10:15

Italian final July HICP inflation confirmed flash estimates at 1.7% Y/Y (vs 1.8% prior). HICP excluding food, energy, alcohol and tobacco was also confirmed at 2.0% Y/Y (vs 2.0% prior).

- Relative to the flash release, services was revised up a tenth to 3.0% Y/Y (vs 3.0% prior), while non-energy industrial goods was revised down a tenth to 0.4% Y/Y (vs 0.5% prior).

- Within services, a pullback in services related to recreation (3.1% Y/Y vs 3.6% prior) was offset by an acceleration in transport services (largely airfares) and miscellaneous services (largely financial services).

- Energy inflation was revised up a notable five tenths to -3.5% Y/Y (vs -2.1% prior), while processed foods were revised down three tenths to 2.8% Y/Y (vs 2.8% prior).

- Unprocessed foods was unrevised at 5.9% Y/Y (vs 4.5% prior).

- The proportion of subcomponents with annual inflation rates between 1-3% Y/Y ticked up to 38%, the highest since February.