CHILE: President Boric Said To Appoint Nicolas Grau As Finance Minister

Aug-21 16:51

- La Tercera reports that Economy Minister Nicolas Grau will be appointed by President Boric to replace Finance Minister Marcel, who resigned earlier. At the same time, Alvaro Garcia is expected to be appointed as the new Economy Minister.

- "*NICOLÁS GRAU TO REPLACE MARCEL AS CHILE'S FIN MINISTER: LT" - BBG

- "*NICOLÁS GRAU TO REPLACE MARCEL AS CHILE'S FIN MINISTER: LT" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

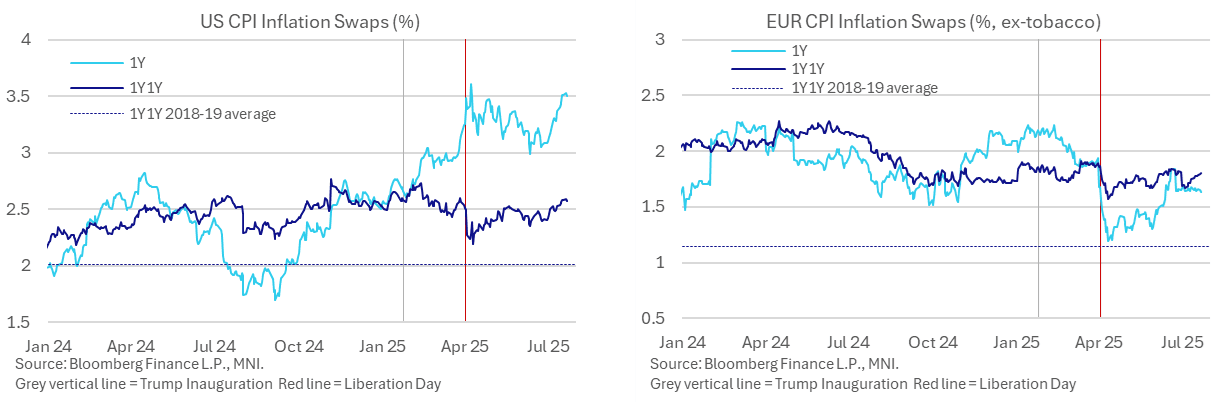

US INFLATION: Short-Term Inflation Expectations Holding Much Of Recent Increase

Jul-22 16:48

- Today’s further decline in yields sees 2Y Treasury yields at the lowest since the surprisingly resilient nonfarm payrolls report on Jul 3, at 3.827% having hit 3.959% last week on Jul 15/16.

- It’s come with only limited reversal in breakevens, with the 2Y breakeven at 2.74% currently in similar levels to Jul 15/16. It peaked at 2.79% on Jul 18.

- Similarly, short-dated inflation swaps remain elevated: the 1Y at 3.50% is 2.7bp lower on the day but still elevated by recent standards, having peaked at 3.61% on Apr 8 prior to the partial backtracking in reciprocal tariffs.

- 1Y1Y inflation swaps also hold much of their recent increase, currently at 2.58% for 1bp of yesterday’s highest close since late March.

- US Tsy Sec Bessent earlier today said "there's nothing that tells me that he [Fed Chair Powell] should step down right now" and President Trump more recently said “I think he’s done a bad job but he’s got to be out pretty soon anyway. In 8 months he’ll be out.”

- Whilst last week’s concerns of Trump firing Powell have abated, there are still signs of longer lasting implications of a more dovish Fed when Powell’s term as Chair ends in May 2026.

CPI inflation swaps including Europe for a comparison:

US STOCKS: Midday Equities Roundup: Chip Makers & Interactive Media Leading

Jul-22 16:34

- Stocks are trading mixed Tuesday, off highs with weaker S&P eminis and Nasdaq indexes lagging the DJIA at midday. Currently, the DJIA trades up 31.91 points (0.07%) at 44354.29, S&P E-Minis down 12.25 points (-0.19%) at 6332.5, Nasdaq down 118.6 points (-0.6%) at 20855.63.

- Information Technology and Communication Services sector stocks led the decline in the first half, semiconductor makers weighing on IT: Lam Research -3.98%, Micron Technology -3.50%, KLA Corp -3.17%, Applied Materials -3.01%, Dell Technologies -2.83% and Broadcom -2.81%

- Interactive media and entertainment shares weighed on the Communications sector: Netflix -2.31%, Meta Platforms -1.03%, TKO Group Holdings -0.78% and Live Nation Entertainment -0.62%.

- On the positive side, Health Care and Homebuilding sectors led gainers by midday: IQVIA Holdings surged 17.82% higher on strong earnings, Charles River Laboratories +7.82%, Quest Diagnostics +6.36%. Also on strong earnings, DR Horton rallied 14.54%, PulteGroup +9.33% and Lennar +7.79%. Other leaders included Northrop Grumman +8.61%, Albemarle +6.97%.

- Earnings expected after today's close: Lockheed Martin Corp, Capital One Financial Corp, Texas Instruments Inc, EQT Corp, CoStar Group Inc, Intuitive Surgical Inc, Enphase Energy Inc, Pegasystems Inc, Range Resources Corp and Baker Hughes Co.

FOREX: Broad USD Weakness Extending, USDJPY Approaches 146.00

Jul-22 16:31

- After consolidating the Monday selloff overnight, the USD index (-0.52%) has resumed its weakening trend on Tuesday, extending the pullback from last week’s highs to ~1.6% in recent trade, further eroding the cautious recovery that had been seen across the first half of July. An extension lower for US yields appears to be assisting the move, helped by Treasury Secretary Bessent providing a more optimistic tone regarding Powell’s short-term future as the Fed Chair.

- Outside of the scandies, gains have been led by the Japanese Yen and Swiss Franc in G10, helping USDJPY extend its post upper house election pullback. USDJPY downside momentum built through initial support of 146.92 (Jul 16 low), printing down to a session low of 146.31. Short-term pivot support to monitor next is 145.85, the 50-day EMA.

- Bessent’s mention of Japan talks going “very well” and that the election may be the impetus to getting a deal done will have also provided tailwinds for the yen. His comments follow Japan’s chief trade negotiator meeting with the US Commerce Secretary on Monday ahead of the looming August 01 deadline.

- Elsewhere, advances for the likes of GBP, AUD, NZD and CAD have all mirrored the adjustment for the DXY. For EURUSD, spot has traded back above 1.1750, narrowing the gap back to cycle highs at 1.1829, the Jul 1 high and the bull trigger.

- The swift reversal and subsequent resumption of weakness keeps a bearish trend intact for USDCAD. Downside momentum appears to have picked up below some daily lows around 1.3650 today and further declines would refocus attention on key support at 1.3540, the Jun 16 low.

- GBP has relatively underperformed, however, cable has still risen back above the 1.35 handle which further negates the prior bearish technical breaks last week. This dynamic keeps EURGBP trading towards its most recent highs and attention firmly on the April 11 high at 0.8738.