PRECIOUS METALS: Dollar Weakness Helps Gold Extend ATHs

Sep-13 13:47

Renewed dollar weakness has seen gold extend its all-time highs, currently 0.8% higher today at $2,579/oz. Immediate focus is on resistance at $2584.0/oz, the 1.764 proj of the Jul 25 - Aug 2 - Aug 5 price swing. This level shields round number resistance at $2,600/oz.

- Silver has seen a larger 2.5% rise today, now at its highest since July 17. The Jul 11 high at $31.754 provides the next resistance, before the bull trigger at $32.518 (May 20 high)

- That leaves the Gold/Silver ratio on track for a third straight decline at 84.2. The Aug 27 low at 83.5732 provides initial support.

- Elsewhere, platinum has broken above $1k to reach its highest since July 18, while palladium is at its highest since April.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: CPI Details: Supercore As Expected, Mixed Drivers

Aug-14 13:41

- Away from housing, supercore inflation was very much as expected at 0.21% M/M after two particularly weak prints averaging -0.05% M/M. These of course haven’t fed into supercore PCE (currently seen averaging 0.18% M/M in May-June) and the implications for PCE in July are mixed at first glance – we’ll update with analyst core PCE estimates in due course.

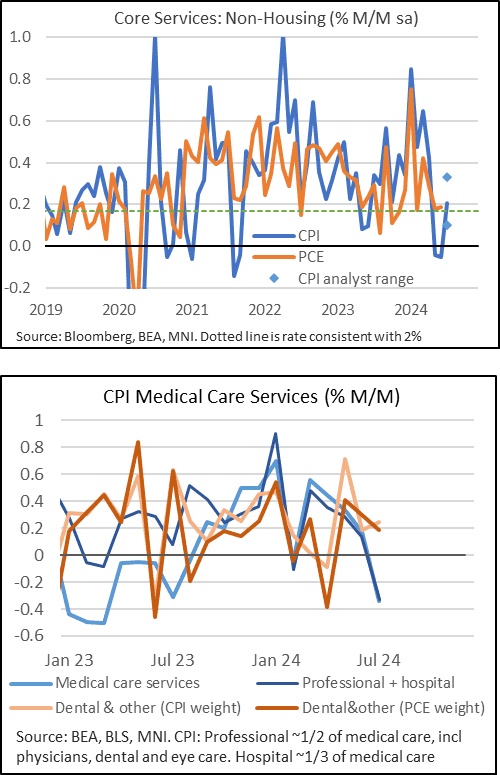

- One notable area for instance is medical care services (8% of core CPI). It saw a sharp decline of -0.34% M/M after 0.17% M/M, driven by hospital services (-1%) but with the limited medical service components that feed into core PCE little changed by our reckoning at ~0.2% M/M.

- There are two other offsetting moves within the details though: vehicle insurance surprised higher with 1.2% after 0.9% (a heavy 4% of core or 11% of supercore that isn’t included in PCE) but food away from home moderated sharply from 0.4% to 0.2% M/M for its second lowest monthly reading since early 2021 (not in core CPI but 7% of core PCE).

US DATA: CPI Details: Goods Provides The Main Downside Surprise

Aug-14 13:41

- CPI goods provided the main downside surprise, contrary to stronger goods inflation in yesterday’s PPI release although that can be seen as signs of further erosion of pricing power.

- At -0.3% M/M, it registered the thirteenth month of deflation out of the last fourteen.

- Used cars were the main downside surprise with a 2.3% decline.

- There was also some continued weakness in core goods ex used cars, but at -0.09% M/M after 0.04% in June it’s not wildly different to the 2024ytd average of exactly 0.00%. Apparel (-0.45%) played a sizeable role here, continuing to reverse the early-year strength.

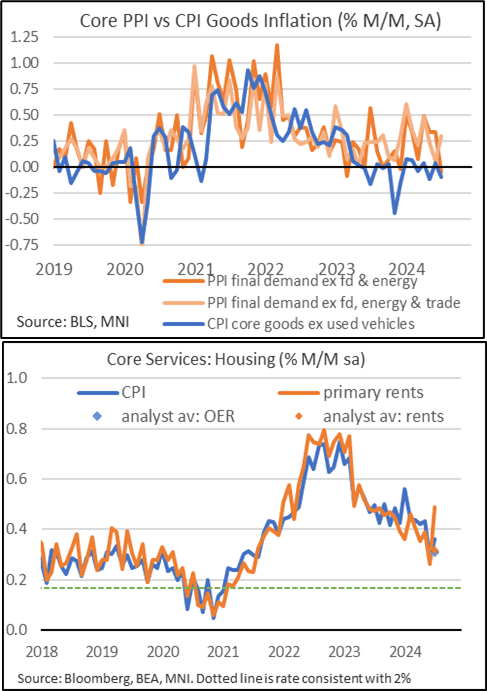

- Services meanwhile saw signs of strength, with the most notable being the 0.49% M/M increase in primary rents (technically the strongest monthly increase since May 2023). Unless it turns out there are sampling issues, this strongly goes against June’s surprise moderation to 0.26% and indicates the anticipated next phase of moderation won’t be as smooth as first thought.

- That said, the more heavily weighted OER component saw a less notable acceleration from 0.28% to 0.36% (analyst average 0.31, range 0.27-0.38), remaining under the 0.4-0.5% monthly prints seen since mid-2023.

- To emphasize the continued rent progress that the FOMC needs to see, OER and primary rents saw a weighted average of 0.27% M/M pre-pandemic. We have only had one month meet that rate over recent years (June) and it has since re-accelerated to 0.39% M/M.

US DATA: Surprise Rents Strength A Stumbling Block For 50bp Cut Arguments

Aug-14 13:40

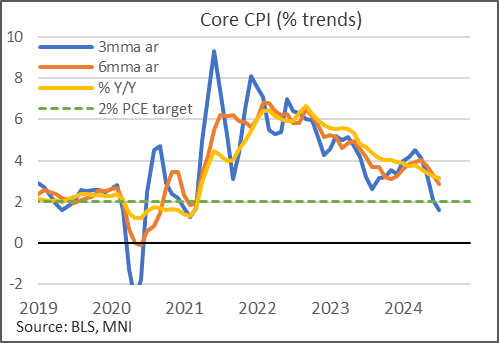

- Core CPI inflation was a touch softer than expected in July at 0.165% M/M (cons 0.2 with a slight tilt lower) but the details were arguably stronger.

- All told, this is a CPI report that offered further broad disinflationary pressures, with core CPI slowing a tenth to 3.17% Y/Y for a new low since Apr 2021 and the six-month rate rate dipping 0.5pps to 2.85% annualized for its first month below the Y/Y in six months.

- However, the re-acceleration in rents, barring any quirks behind their measures, shouldn’t give the Fed greater confidence that inflation is moving sustainably toward 2%. We don’t see this report warranting a 50bp cut in September but the ultimate test is going to be next month’s payrolls report, with further dovish unemployment rate surprises or at least another 4.3% print and additional CPI softness needed to justify a 50bp move.