EURIBOR: Positive Skew Affirms Lower ECB Rate View; EU-US Trade Deal In Focus

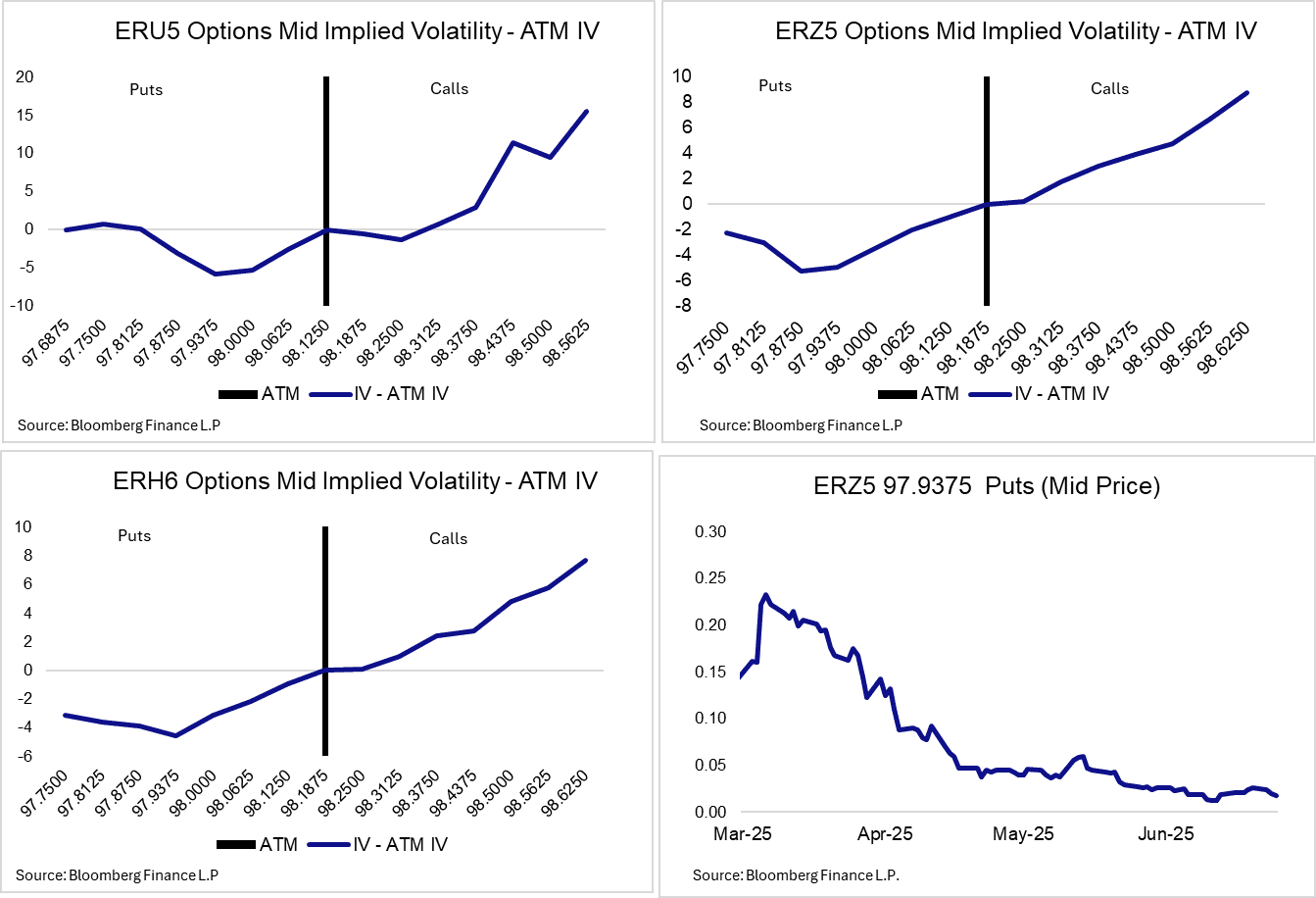

Euribor options markets continue to exhibit positive skew across the next three quarters (U5, Z5, H6), with the risks of more aggressive ECB easing than currently expected spurring demand for dovish call structures, often funded through sales of puts/put spreads. The June Eurozone flash inflation round kicks off on Friday with Spain and France (EZ HICP estimate on July 1st), but the outcome of EU-US trade negotiations are likely to be more consequential for the EUR front-end ahead of the July 8 tariff delay deadline.

- A reminder that if no agreement between the EU and US is reached, almost all EU exports to the US will be subject to 50% tariffs. Although general expectations are that such an extreme outcome will be averted (the ECB’s “severe” trade scenario presented at the June decision assumed 20% US tariffs on EU exports alongside EU retaliation), it still presents a notable downside growth risk, both directly and via the uncertainty channel.

- While officials have signalled that talks are “progressing”, there is not a yet clear pathway to a deal. Recent reporting has suggested EU officials are preparing retaliatory measures even in the case of a 10% baseline US tariff.

- Today’s flow has included a buyer of the 98.375/98.50/98.625 Z5 call fly in 5k, with a 98.125/98.25/98.375 U5 call fly bought in 10k yesterday. In H6, last week saw 98.06/98,1875/98.4375/98.5625 call condors favoured, sold against puts/put spreads.

- While markets still lean dovish on balance, compressed put vol has seemingly provided attractive entry points for those with a more hawkish ECB outlook. Increased German/EU fiscal spending may be one factor supporting this view, alongside possible medium-term inflationary risks from increased trade barriers (especially in the case of EU retaliation). Last Thursday saw a large buyer of 97.9375 Z5 puts for 2.25 in 55k. These puts were trading at ~25 ticks in early March following the initial German fiscal announcement. Outright put buyers have also been seen in Z5 in recent sessions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: French Flash May HICP Expected Unchanged At 0.9% Y/Y

The Eurozone May flash inflation round kicks off with France tomorrow at 0745BST/0845CET. The data is being released so early this month because of Thursday’s Ascension Day holiday. Current consensus looks for annual HICP inflation to remain steady at 0.9% Y/Y, with a monthly rate of 0.1% M/M.

- The May flash PMI contained soft inflation details: “Subdued demand conditions were a factor that weighed on companies’ pricing decisions during May. Not only did prices charged fall, but they did so to the greatest extent since January 2021. Discounting was broad-based by sector, underlying survey data revealed. According to panellists, prices charged were reduced as a result of lower interest rates, strong competitive pressures and promotional offers. Notably, output price reductions occurred despite a slight intensification of input price inflation”.

- Goldman Sachs expect French headline HICP at 0.8% Y/Y, with core to ease to 1.7% Y/Y from 1.9% prior. They expect “both core goods and services moving slightly lower on a year-over-year basis”. Specifically, they “expect an 11%mom nsa decline in the airfares component and a 2.6%mom nsa increase in package holidays, partly offset by recreational and accommodation services components”.

- Goldman look for “energy inflation to fall further to -7.9%yoy from -7.4%yoy in April, partly driven by a reported 6.4% gas price decline. We expect processed food inflation to go to 1.0%yoy (from 0.9%yoy in April) and unprocessed food inflation to decline to 2.5%”.

- Meanwhile, SEB write that “the April reading was partly lifted due to Easter effects on recreation and transport. A larger reversal effect is therefore expected in the May numbers”.

STIR: Goldman: A Closer Call For June BoC, But Value In The CAD Front-End

Goldman Sachs note that “the upside surprise in Canada’s April inflation print saw market cut pricing sharply reset, with the market pricing in only about 5bp for the June meeting”.

- Their economists expect “the BoC to look through the one-off price level increase due to tariffs - which they think played a role in the upside surprise - and continue to expect a cut at the June meeting (plus one more in July to a 2.25% terminal rate), though they acknowledge the risks of a hold have gone up”.

- Given market pricing implies only about 60% of a full cut by the July meeting, Goldman Sachs think “there is value to receiving the very front-end of the CAD curve with the softer activity picture continuing to point towards cuts” and recommend receiving July BoC meeting OIS.

OIL: Little Changed As Negative MT Fundamentals Counter Latest Crude Positives

Crude oil futures are little changed on the day, with the crude-supportive developments in the EU-U.S. trade talks, in addition to geopolitical risks in the form of the potential for a further intensification in the Israel-Hamas conflict and the latest Russian missile launches on Ukraine, neutralised by some ongoing fundamental headwinds.

- That leaves WTI & Brent futures little changed, with medium-term bearish technical themes intact despite the recent bounce.

- Bulls need to break the 50-day EMA’s in the contracts ($62.75 & $66.24, respectively), to turn the tide more in their favour.

- Meanwhile, the respective April 9 lows present key support and the technical bear triggers.

- Our commodity team notes that fundamental pressure remains evident amid general economic headwinds, coupled with expectations for a more meaningful OPEC+ production increase from July.

- BBG have warned that OPEC+’s seemingly hardline approach to punishing its overproducing members risks plunging crude into a full-blow price war.

- Elsewhere, some downward pressure seemingly came from U.S. President Trump noting that he was “optimistic” following the last round of talks with Iran on limiting their nuclear programme in exchange for sanctions relief.

- Also, note that the Trump administration is preparing to use a narrowly tailored license for Chevron to allow it to perform minimal maintenance of essential operations in Venezuela.