FRANCE: PM Lecornu Survives Censure Motion

As expected, PM Sebastien Lecornu and his second administration have survived a confidence motion in the National Assembly. A total of 271 lawmakers voted for removal, short of the 289 required to remove the gov't.

- As noted earlier, the centre-left Socialist Party (PS) opting not to support censure meant crossing the threshold to remove Lecornu was too high a hurdle (see 'FRANCE: Voting Underway In First Censure Motion Against Second Lecornu Gov't', 10:23BST).

- A second censure motion put forward by the far-right will also be voted on today, but is likely to fail as well.

- While Lecornu remains in place for now, he and his gov't are walking a tightrope. The combined seat total for the far-right Rassemblement National, right-wing UDR, environmentalist Ecologists, left-wing Communists, and far-left La France Insoumise comes to 263, meaning eight deputies from the PS, conservative Les Republicains or centrist LIOT group voted for censure.

- The upcoming budget debates could see more lawmakers from any of these groups peel off to back censure, ensuring political risks will remain elevated in the short-to-medium term.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

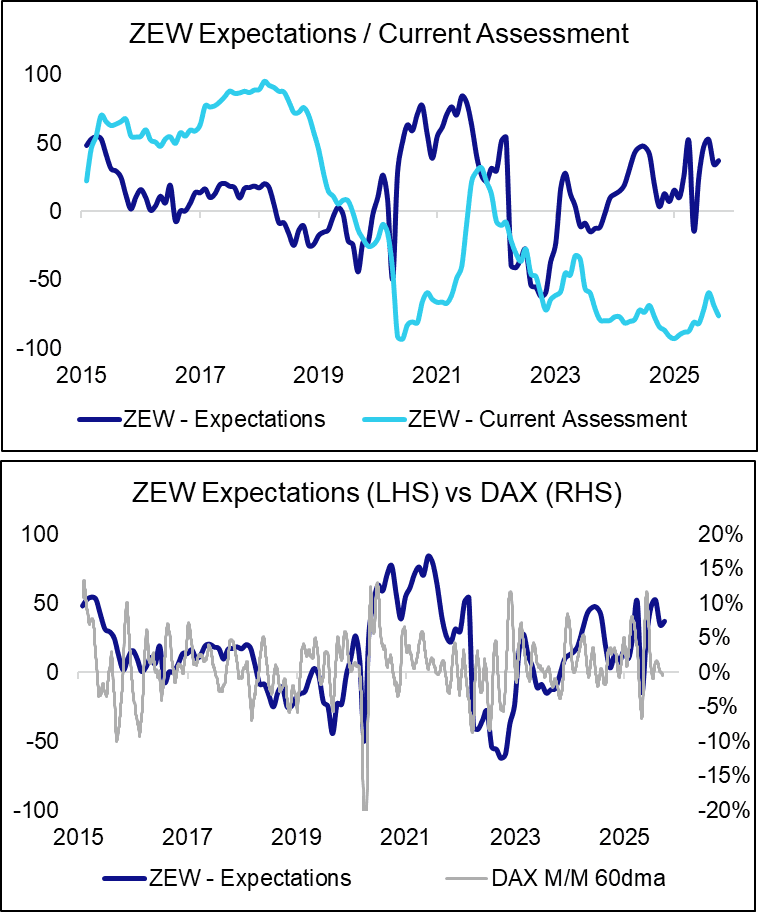

GERMAN DATA: Don't Read Into The Stronger-than-expected ZEW Expectations Index

The September German ZEW survey’s expectations component was much stronger-than-expected at 37.3 (vs 25.0 cons), but was only a little higher than August’s 34.7 reading. We suspect that consensus for the expectations component was weighed down by the late-August pullback in the Stoxx50 index. The ZEW has historically been sensitive to prior M/M stock market moves, though this signal appears to have lost some power in recent months.

- The current conditions component meanwhile was weaker-than-expected at -76.4 in August (vs -73.6 cons, -68.6 prior), down from a cycle high of -59.5 in July.

- The press release notes that “The outlook has improved in particular for export-oriented sectors, which had recently suffered a strong decline. Among the industries that benefit most are the automotive sector, the chemical and pharmaceutical industry and the metal sector. Nevertheless, the three indicators for these industries continue to be in the negative range”

EGBS: Bund Futures Weaken Into 5-year German Auction Before Stabilising

Bund futures weakened into this morning’s E4.5bln 2.20% Oct-30 Bobl auction before stabilising. Futures are currently -9 ticks at 128.64, off earlier session highs of 128.90. Initial support is Friday’s low at 128.51, which shields the Sep 4 low at 128.25.

- The German auction saw slightly softer cover ratios than last month's outing, but the lowest accepted price was nonetheless in excess of the pre-auction mid price. Finland will sell bonds later this morning, while Slovakia has also already come to the market today.

- Bunds found light support from a pullback in equities and crude oil futures earlier, but moves have generally lacked conviction.

- The German curve has bear steepened, with yields +0.5 to +2.5bps higher.

- 10-year EGB spreads to Bunds are biased slightly tighter. The BTP/Bund spread is eyeing a test of the August low of ~76.7bps (currently -0.5bps at 77.5bps).

- The September German ZEW survey’s expectations component was much stronger-than-expected at 37.3 (vs 25.0 cons), but was only a little higher than August’s 34.7 reading. Meanwhile, Eurozone July industrial production was slightly softer than forecast at 0.3% M/M (vs 0.4% cons, an upwardly revised -0.6% prior).

- ECBspeak hasn’t been market moving. Maltese CB Governor Scicluna had a more hawkish tone than Kazaks earlier in the morning.

STIR: Low Odds Of 50bp Sep Fed Cut Priced, Miran Confirmed, UBS Go Long SFRZ6

FOMC-dated OIS continues to price outside odds (~5%) of a 50bp cut at tomorrow’s decision.

- All but 2 analysts expect a 25bp cut, based on the 32 sell-side previews MNI saw.

- The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”.

- The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- The caveat here is that Senate approval of Fed Governor Miran provides a notable wildcard when it comes to the SEP.

- Our full preview can be found here.

- Note that UBS have recommended going long SFRZ6 at an implied rate of 2.96% as their economists expect “the Fed to respond to an adverse demand shock in the labour market with a 20% probability of a 50bp rate cut”. They also suggest that “the drop in U.S. rates after a consensus U.S. CPI print suggests that market positioning leans the other way”.