FRANCE: PM Lecornu On X.com: All Issues During Consultations Open To Debate

Lecornu on X.com following his surprise reappointment as French Prime Minister by President Macron (translated from the French):

"I accept - out of duty - the mission entrusted to me by the President of the Republic to do everything possible to provide France with a budget by the end of the year and to address the daily life issues of our fellow citizens. We must put an end to this political crisis that exasperates the French people and to this instability that is harmful to France’s image and its interests. As I have said, this can only be achieved under certain conditions, drawing the necessary conclusions from the past few weeks:

- All issues raised during the consultations held in recent days will be open to parliamentary debate: deputies and senators will be able to take on their responsibilities, and the debates must be seen through to the end;

- Restoring our public finances remains a priority for our future and our sovereignty: no one will be able to evade this necessity;

- All ambitions are legitimate and useful, but those who join the Government must commit to setting aside presidential ambitions for 2027;

- The new government team must embody renewal and diversity of skills.

I will do everything to succeed in this mission."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

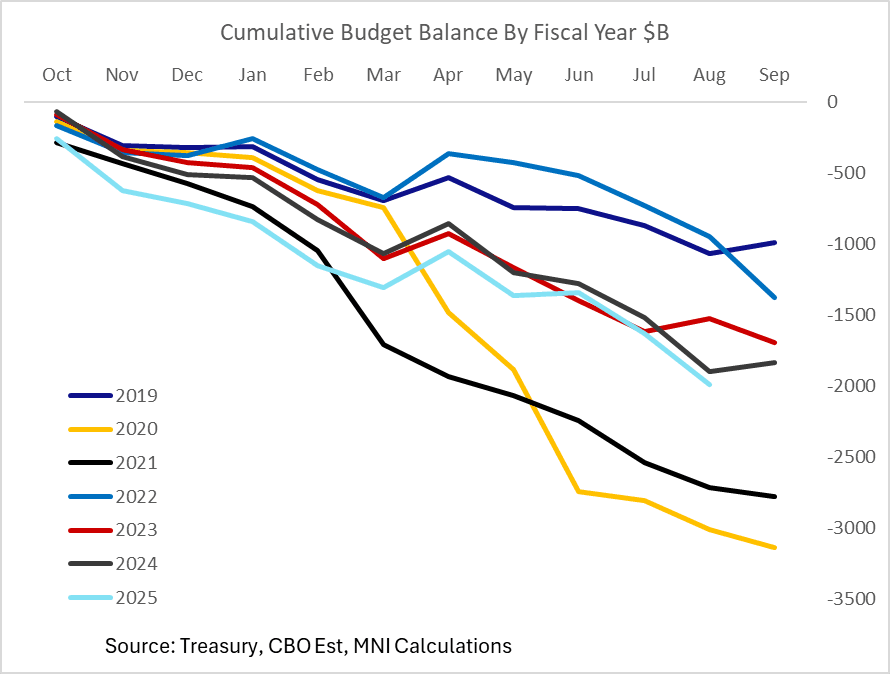

US FISCAL: Tariffs Partially Offsetting Deficit Expansion So Far

With one month remaining in the fiscal year (Oct-Sep), the Congressional Budget Office is estimating a cumulative deficit of $1.989T through August, including a $360B deficit for August itself. That's about $92B above last year's cumulative total to this point. While the Treasury's official August tally will only be released Thursday at 2pm ET, the CBO's estimate is usually very close to the mark.

- When accounting for timing shifts in outlays, however, the deficit is only about $11B bigger than it was at this point.

- Year-to-date, accounting for timing shifts, outlays are up 5% for a total $310B Y/Y in the 11 months through August, of which $223B is mandatory spending and $72B is net interest on the public debt. The estimate is flattered to the downside by a $110B fall in Department of Education outlays, about half of which is related to adjustments to student loans. And FDIC outlays fell $63B, vs 2024 which was hit by bank failures in the wake of the Silicon Valley Bank debacle.

- And in terms of timing-adjusted receipts, they're up $299B Y/Y in the fiscal year-to-date, or 7%. While corporate taxes are a little lower (largely due to timing shifts), individual income taxes are up 8% ($181B) - and "other receipts" soared 45% ($102B).

- It should be no surprise that within that category, customs duties made up $95B (+137% Y/Y) of that total, marking a $165B total for the fiscal year so far, in the wake of the Trump administration's tariff increases.

- The deficit is still tracking above most analyst expectations we've seen of $1.8-1.9T (was $1.83B in FY2024), though September tends to be a mixed month in terms of net outlays and there is of course the new monthly boost of tariffs (not including any negative dynamic effects on growth from said tariffs). We will get more details after the official Treasury statement expected Thursday.

USDCAD TECHS: Bullish Theme

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3925 High Aug 22 and the bull trigger

- RES 1: 1.3868 High Aug 26

- PRICE: 1.3850 @ 16:38 BST Sep 10

- SUP 1: 1.3782/27 50-day EMA / Low Aug 27 and a bear trigger

- SUP 2: 1.3709 61.8% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 3: 1.3658 76.4% retracement of the Jul 23 - Aug 22 bull cycle

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact. The recovery from the Aug 29 low highlights a potential early reversal signal and if correct, marks the end of the corrective pullback between Aug 22 - 29. An extension higher would open the bull trigger at 1.3925, the Aug 22 high. Support lies at 1.3727, the Aug 29 low. Clearance of this level would instead reinstate a short-term bear theme and expose 1.3709 initially, a Fibonacci retracement.

US OUTLOOK/OPINION: Wells Fargo: Sticky Services To Continue

Wells Fargo is on the low end of sell-side expectations for unrounded core CPI, seeing a 0.29% M/M increase in August, but still expect “sticky services inflation alongside the rebound in goods prices” continuing.

- Core goods are set to rise 0.25% M/M: “New vehicle inflation, which has been tame, is poised to strengthen as a rebound in auto sales has helped to reduce inventory and the use of incentives has slowed. Price growth for other import-heavy items, such as apparel, recreational goods and communication hardware, should remain solid as well with another 0.3% increase.”

- Meanwhile core services prices to rise 0.30% M/M: “Travel-related service prices started to rebound in July, and we estimate another solid gain in August (+1.0%), led by lodging away from home. While spending on discretionary services remains generally weak, consumers' appetite for travel shows signs of rebounding with hotel occupancy and TSA screenings up again on a year-ago basis, suggestive of some stabilization in consumer demand.”

- However, medical care services could moderate after July’s jump and primary shelter inflation “should run a touch under its 0.31% year-to-date average through the remainder of 2025”.