EM CEEMEA CREDIT: PKO BANK POLSKI SA: Q2 25 Results: Solid

(PKOBP:A3/-/-)

- As expected, solid Q2 2025 results from PKO, small beat in every metric. Net Interest income +2.9% vs Q1 2025 at PLN6.15bn vs PLN5.98bn estimates. Net interest margin was steady at 4.91%. Fee & Commission +1.9% vs Q125 at PLN1.28bn vs 1.27bn est, driven by currency exchange and credit cards. Net income PLN2.66bn vs PLN2.53bn est

- NPL ratio marginally better at 3.52% vs 3.7% estimates and capital ratios remain solid with TCR at 17.3% and CET1 at 16.29%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

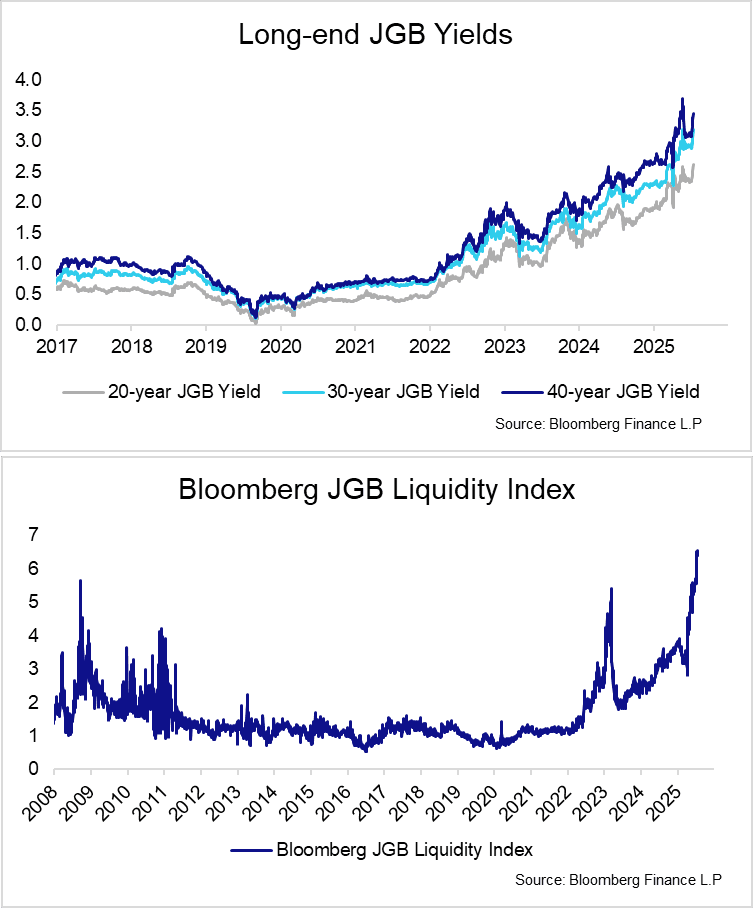

JGBS: Steepening Extends With 30-year Yields Eyeing May 21 High

Bear steepening in the JGB curve has extended this morning, spilling over into long-end EGBs and Gilts. 10s30s is currently just under 5bps steeper at 157.3bps, still below last Tuesday’s 160.3bp high.

- 30-year yields are up 11bps at 3.172%, with initial key resistance the May 21 high at 3.204% (the highest level since the BBG series began in 1999).

- Meanwhile, 10-year yields pierced the May 22 high of 1.582% overnight, but are currently back at 1.580% (+6bps today).

- As already noted, a combination of fiscal/political risks and possible upgrades to the BOJ’s inflation projections at the upcoming July 31 decision have contributed to the latest rise in yields.

- The Upper House election will be held on July 20. The LDP is on course to lose a significant number of seats and the governing coalition could also lose its overall majority. JNN reporting overnight was supportive of this scenario.

- Meanwhile the latest Bloomberg sources reporting was consistent with last week’s MNI Policy Team piece: BOJ officials may increase their median CPI forecast for FY25 from 2.2% partly due to a temporary surge in rice prices, MNI understands. The steepening of the curve suggests this is a contributing factor of today’s JGB selloff, rather than a driver.

- Structural forces pushing long-end JGB yields higher also remain in play, namely concerns around demand for long-end debt and weak liquidity at that portion of the curve.

- This week’s Japanese calendar includes 5-year supply tomorrow, June trade data on Thursday and June national CPI on Friday.

SILVER TECHS: Impulsive Bull Wave Extends

- RES 4: $40.285 - 1.618 proj of the Apr 7 - 25 - May 15 swing

- RES 3: $40.000 - Psychological round number

- RES 2: $39.655 - 1.500 proj of the Apr 7 - 25 - May 15 swing

- RES 1: $39.093 - Intraday high

- PRICE: $38.961 @ 08:18 BST Jul 14

- SUP 1: $36.493 - 20-day EMA

- SUP 2: $35.334 - 50-day EMA

- SUP 3: $33.967 - Low Jun 3

- SUP 4: $32.615 - Low May 22

Trend conditions in Silver are unchanged, a strong impulsive bull cycle remains intact and today’s gains further reinforce current conditions. The metal has cleared key short-term resistance at $37.317, the Jun 18 high. This confirms a resumption of the uptrend and sights are on the $39.655 next, a Fibonacci projection. On the downside, initial support to watch lies at $36.493, the 20-day EMA.

USDCAD TECHS: Resistance Remains Intact

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3752 50-day EMA

- PRICE: 1.3690 @ 08:11 BST Jul 14

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

Short-term gains in USDCAD appear corrective and the trend structure remains bearish. Resistance to watch is the 50-day EMA, at 1.3752. A clear break of the average would signal scope for a stronger recovery and highlight a possible reversal. For bears, sights are on key support at 1.3540, the Jun 16 low. Clearance of this level would resume the downtrend and open 1.3503, a Fibonacci projection.