EM CEEMEA CREDIT: Petra Diamonds: S&P downgrades, again

Aug-27 09:30

(PDLLN; Caa3neg/CCneg/NR)

- Not a surprise. South Africa’s diamond miner Petra Diamonds saw its ratings lowered from CCC to CC by S&P, aft-mkt close y’day. Outlook remains on negative on technical factors, but we see potential for a sparkle of light at the end of the tunnel.

- The agency action follows the Co.’s proposed terms for in-principle agreement to refi the existing RCF (extension on revised terms) and ‘26s notes (extension with amendments) earlier in the month (as well as specific equity rights issue), citing “current capital structure as unsustainable and therefore consider this exchange as distressed according to our criteria, mainly because absent the proposed exchange, there appears a high probability of conventional default around the 2026 maturities” (Source: S&P Global Ratings).

- The agency cites a further lowering of the proposed refi deal to D for the ’26 notes upon completion but highlights that post exchange there is “a high probability” that the ICR will be higher than the pre refi announcement CCC standing, rationale based on subsequent improved B/S structure and limited refi risks. No surprise here either.

- For what it is worth, our screens indicate PDLLN 26s last close at high 50s cash px area, as per Bloomberg data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: Expectations Not Swayed By Two-Sided Trade Deal Impacts

Jul-28 09:28

- As discussed, there has been little reaction in European front rates to weekend news on the US-EU trade deal with a 15% tariff on EU goods, having already been rumoured last week.

- There is still just 4bp of cuts priced for the Sept ECB, having adjusted from 10bp prior to Thursday’s ECB press conference and subsequent sources pieces pointing to a high bar to a cut next meeting. This had been ~ 12.5bp before headlines earlier in the week on the trade deal nearing.

- Recall Lagarde from the Q&A: "But one thing I will add to that is that the sooner this trade uncertainty is resolved – I think we use the word “resolved swiftly” – so the sooner it is resolved, the less uncertainty we will have to deal with, and that would be welcomed by any economic actors, including ourselves.”

- From a near-term domestic inflation angle, the deal has clearly reduced the prospects of EU retaliation, for which there had been growing support for more penal approaches. Nevertheless, details on the deal more broadly are sparse.

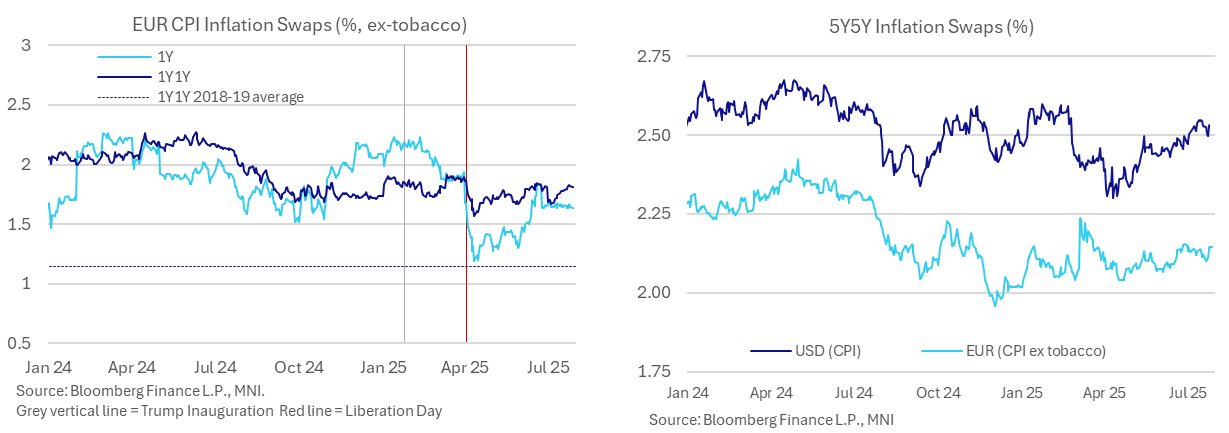

- For now, 1Y inflation swaps are just 0.5bp lower than Friday’s close, at 1.638% a little further off last week’s 1.668% but having broadly kept an unusually narrow range of 1.64-1.69% in July to date.

- 1Y1Y inflation swaps meanwhile at 1.81% are holding their trend climb seen over the month, close to recent highs having average close to 1.9% in the two weeks ahead of early April “Liberation Day” tariff announcements. Whilst still below 2%, as they have been since July 2024, they remain far higher than the tepid 1.1% averaged in 2018/19 pre-pandemic.

- Much further out, 5Y5Y inflation expectations at 2.144% are towards the high end of ranges over the past couple months but with little change over the weekend. This remains comfortably between the ~2.05% seen prior to EU and German fiscal announcements in early March after which they briefly surged to 2.22%.

USD: A strong early performance for the Dollar

Jul-28 09:19

- The Dollar was mostly mixed against G10s going into the European session and just ahead of the EU Cash Govie Open, but as Europe came in, the Dollar saw a Broader base bid, after Desks took in the Overnight Tariff news in their stride.

- The US and the EU agreed a 15% Tariff deal, Europe also agreed to cut its Car Import duty to 2.5% as part of the deal.

- Multiple Desks are still somewhat perplexed at the strength of the Dollar in early trade, and aside from the Trade news, new headlines or drivers have so far been limited.

- Instead some Market participants also speculate that the Fed will stick to its Hawkish stance at Wednesday's Meeting when unchanged Rate is expected from the FOMC, for some of the bid into the Dollar.

- G10 Pairs/Crosses have seen some decent early ranges, the EURUSD sees over a 100 pips range, with the EUR mostly under some small pressure following the fade off the highs in European Equities.

- The Kiwi is the worst early performer within G10 against the Greenback, and the initial support will be seen at 0.5939 in NZDUSD, last Week's low.

- Looking ahead, there are no Tier 1 Data for the session, but the US-EU trade deal details continue to trickle down.

EUR: HSBC Cautious Of EUR Gains On Trade Deal

Jul-28 09:07

HSBC note that the U.S.-EU trade deal has “several consequences. For investors, it reduces uncertainty surrounding future EU-U.S. trade and removes the near-term risk of an escalatory tit-for-tat trade war. For businesses, it provides greater clarity, which should support business planning and investment. Nevertheless, a new 15% tariff still provides a higher barrier for EU firms selling into the U.S. than before April 2. A higher tariff could lead firms to shift production to the U.S. and/or could weigh on the profits of EU exporters and European growth more broadly”.

- They think “EUR/USD will struggle to make further gains near term and believe other fundamental drivers such as interest rate differentials will become more influential drivers again. Since April 2, political uncertainty pushed EUR/USD higher compared to rate differentials. The reduction of political uncertainty could reverse this move”.

- More broadly, HSBC write “although Eurozone fundamentals have stabilised, we do not think the ingredients are in place for a sustained rally. With the ECB’s easing cycle complete, U.S. factors will remain the key focus, notably with the FOMC meeting on Wednesday and the U.S. labour market report on Friday”.