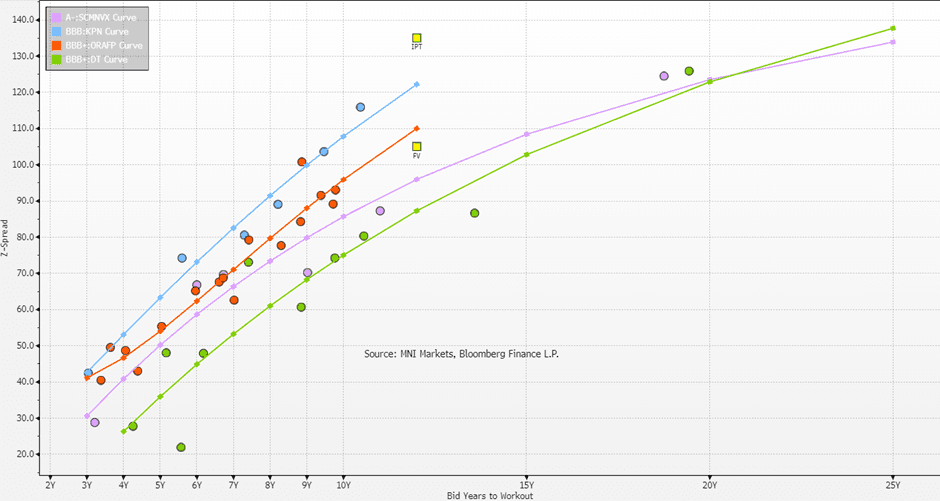

EU COMMUNICATIONS: Orange: FV (B’mark 12y)

Aug-28 08:14

ORAFP (Exp. Ratings: Baa1/BBB+/BBB+)

- IPT given at MS+135a. We see FV around MS+105.

- Lots of bonds sitting away from par on the shown curve.

- ORAFP 49s not shown here; they invert the extreme long end of the curve.

- Our FVs account for this though too many to show on the chart.

- Recent results were not a mover: https://mni.marketnews.com/47dVI1n

- Neither were comments on French consolidation: https://mni.marketnews.com/4mz6ZxP

- MasOrange reconsolidation is an ongoing story though we expect leeway at the agencies.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Large Call Spread

Jul-29 08:06

SFIM6 97.40/97.50cs, bought for 0.75 in 10k.

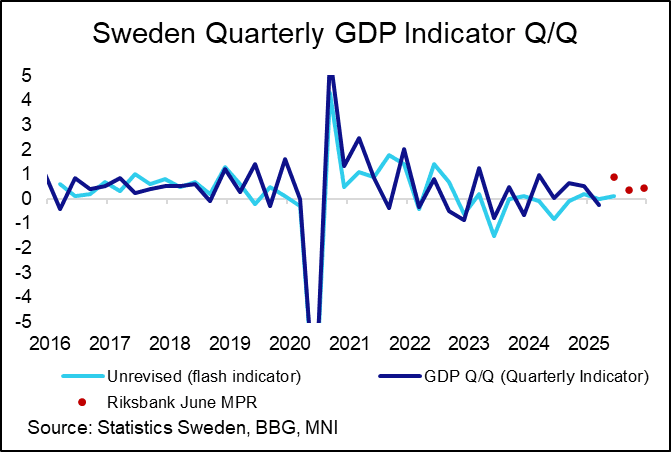

SWEDEN: Q2 Flash GDP Weaker Than Expected

Jul-29 08:00

The Swedish flash Q2 GDP indicator was weaker-than-expected at 0.1% Q/Q (vs 0.3% cons, -0.24% prior). As always, a generous pinch of salt should be taken with this indicator, it can be heavily revised and is often a poor predictor of actual GDP outcomes (Q2 due at the end of next month). The market reaction has been relatively limited for now.

- The 0.1% reading was significantly below the Riksbank’s June MPR projection of 0.9%. We suspect that the extremely weak May retail sales report, which also pulled down the May monthly GDP estimate, has had a large role to play here.

- June retail sales are due tomorrow, which will also reveal whether May’s -4.8% M/M is revised.

- June monthly GDP was 0.5% M/M (vs a downwardly revised -0.8% prior from -0.2% initial). However, no details are released today.

- Despite its caveats, the message from the GDP indicator is consistent with an economy that is still a little subdued despite 200bp of Riksbank cuts. It leans in favour of market expectations for one more cut this year. The July flash CPI report (due next Friday) may be important in determining whether an August cut is still on the cards.

- While trade policy uncertainty has reduced since the US-EU struck an agreement at the weekend, the terms of the deal would still exert a toll on Sweden’s export-sensitive economy.

MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

Jul-29 08:00

- MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

- MNI: ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.4%